Frank Talk

Ultra-Short Government Bonds Are Rallying on Bank Contagion Fears

Date Posted: March 16, 2023

Read time: 6 min

Yields on short-dated U.S. Treasury bonds fell to their lowest levels in months on increased safe-haven demand.

Bank contagion has officially spread to international markets, raising fears that last week’s dramatic failures of U.S. lenders Silicon Valley Bank (SVB) and Signature Bank may be just the start of another global crisis. Shares of Credit Suisse Group, one of Europe’s top 20 largest banks by assets, plunged more than 32% in intraday trading, hitting a new all-time low following reports that the Swiss bank continues to see depositor outflows.

Yields on short-dated U.S. Treasury bonds fell to their lowest levels in months on increased safe-haven demand. (Bond yields and prices move in opposite directions.) The six-month yield traded as low as 4.5% on Wednesday, while the one-year yield came close to breaking below 4.0% for the first time since October 2022.

I believe the bond rally may continue the longer fears of a full-blown banking crisis persist. Investors interested in capital preservation right now can do much worse than short-term Treasuries, which are less volatile than longer-dated bonds.

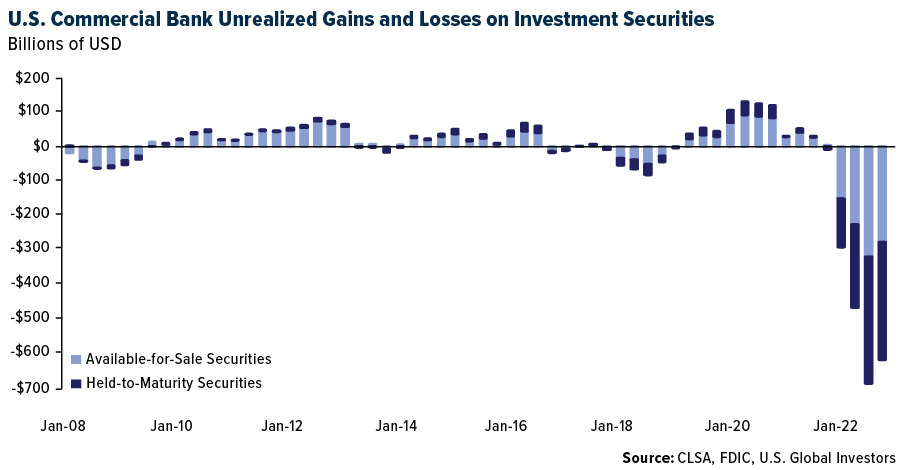

Long-Term Debt Contributing to Massive Unrealized Bank Losses

In fact, long-term Treasuries are a big part of the reason why banks are under pressure at the moment.

Why? I’ll let equity research strategist Lyn Alden explain because I don’t believe I would be able to do a better job than she does:

Banks were given a ton of new deposits during 2020 and 2021 thanks to fiscal stimulus to people, and banks used those deposits to buy a lot of [Treasury] securities, which were low-yielding at the time. After a year of rapid interest rate increases, the prices of those fixed-income securities are now lower than they were when banks bought them.

Remember, yields and prices go in opposite directions. What this means is that U.S. banks now have massive amounts of unrealized losses on their books—an estimated $620 billion, all told. To clarify, these are assets that have decreased in value due to rising interest rates but haven’t been sold yet.

As Alden points out, banks should be fine if they hold these securities to maturity and get their principal back. But not every bank is able to do that.

The problem is that if there’s a run on a bank and depositors seek to withdraw more cash than the institution has on hand, it may be forced to sell its highly discounted bonds, thereby locking in those losses.

This is precisely what happened to SVB. To fund redemptions, the bank reportedly had to sell its $21 billion bond portfolio… for a loss of $1.8 billion.

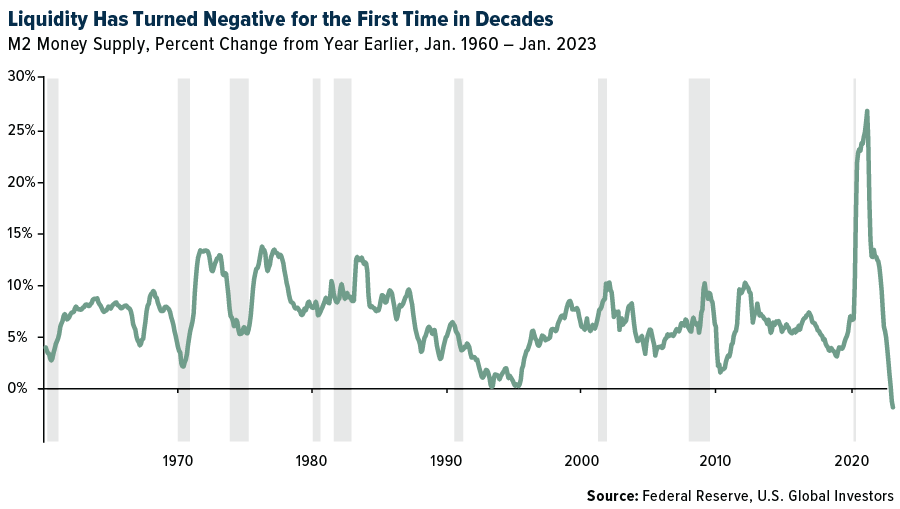

Where Has All the Liquidity Gone?

Making matters worse is that liquidity is drying up, and fast. M2 money supply is how the Federal Reserve defines cash as well as everything that’s deposited in checking and savings accounts. Again, in the first couple of years of the pandemic, the supply of M2 money skyrocketed. This helps explain why inflation is where it’s at today, and to combat higher prices, the Fed has had to significantly tighten monetary policy.

You can see the results below. For the first time in decades, M2 money supply has actually gone negative.

Pricing In a Fed Pivot

Taking into consideration the risk of systemic bank failures, among other risks, the Fed may be more likely to pause or even reverse quantitative tightening.

This possibility is reflected in the market’s current pricing, as seen in the CME Group’s FedWatch Tool, which uses fed funds futures pricing data. As of Wednesday, the implied probability of interest rates being between 3.75% and 4.00% by January 2024 was 29%, compared to the current rate of around 4.58%. However, this is just a probability and may not be accurate.

However, if you believe that the Fed is more likely to lower rather than raise rates this year, then buying short-term bonds may be a good option. When rates are expected to fall, investors often turn to short-turn debt as a way to lock in current yields before they decline.

This is the opposite strategy of banks like SVB.

Our U.S. Government Securities Ultra-Short Bond Fund (UGSDX) is designed to be used as an investment that takes advantage of the security of U.S. government bonds and obligations, while simultaneously pursuing a higher level of current income than money market funds offer.

Under normal market conditions, UGSDX invests at least 80% of its net assets in U.S. Treasury debt securities and obligations with an average effective maturity of two years or less.

Please consider carefully a fund’s investment objectives, risks, charges and expenses. For this and other important information, obtain a fund prospectus by visiting www.usfunds.com or by calling 1-800-US-FUNDS (1-800-873-8637). Read it carefully before investing.

Foreside Fund Services, LLC, Distributor. U.S. Global Investors is the investment adviser.

Investing involves risk including the possible loss of principal. Bond funds are subject to interest-rate risk; their value declines as interest rates rise. Past performance is no guarantee of future results.

An available-for-sale (AFS) security is a debt or equity security purchased with the intent of selling before it reaches maturity or holding it for a long period should it not have a maturity date. A held-to-maturity (HTM) security is purchased to be owned until maturity. M2 is the U.S. Federal Reserve’s estimate of the total money supply including all of the cash people have on hand plus all of the money deposited in checking accounts, savings accounts, and other short-term saving vehicles such as certificates of deposit (CDs).

All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor. The S&P U.S. Treasury Bill 6-9 Month Index is designed to measure the performance of U.S. Treasury bills maturing in 6 to 9 months.