Investor Alert

Surge in Defense Funding Puts European Stocks in the Spotlight

Date Posted: September 20, 2024

Read time: 40 min

For years, the U.S. has been the dominant player in military spending, with American companies like Lockheed Martin and RTX (formerly Raytheon) commanding the global arms market. But now, Europe—specifically its arms manufacturers—may be the next big opportunity for savvy investors.

A recent, long-awaited report by Mario Draghi, former Prime Minister of Italy and former head of the European Central Bank (ECB), paints a clear picture: Europe needs to boost its defense spending.

Draghi’s report outlines a plan to increase national defense budgets, prioritize defense research and development (R&D) and reduce Europe’s dependence on U.S.-made military equipment.

These recommendations echo Polish Prime Minister Donald Tusk’s comment back in March that the continent had entered a “prewar” era and needed additional investment in its defense sector.

I imagine this talk must be music to the ears of European arms manufacturers, and for investors like you, it could signal a potentially interesting chance to start participating.

Europe’s Defense Sector Must Invest More in R&D

Draghi’s report should be a wake-up call to Europe’s leaders. The region may be the second-largest military spender in the world, but that doesn’t tell the full story. For decades, European nations have underfunded their defense sectors, relying heavily on the U.S. for both technology and equipment.

In the 12 months through June 2023, 78% of the €75 billion ($83 billion) spent by European countries on defense went outside the continent, with 63% landing in the hands of U.S. manufacturers, according to Draghi’s findings. This over-reliance on foreign arms, primarily American, has left Europe exposed.

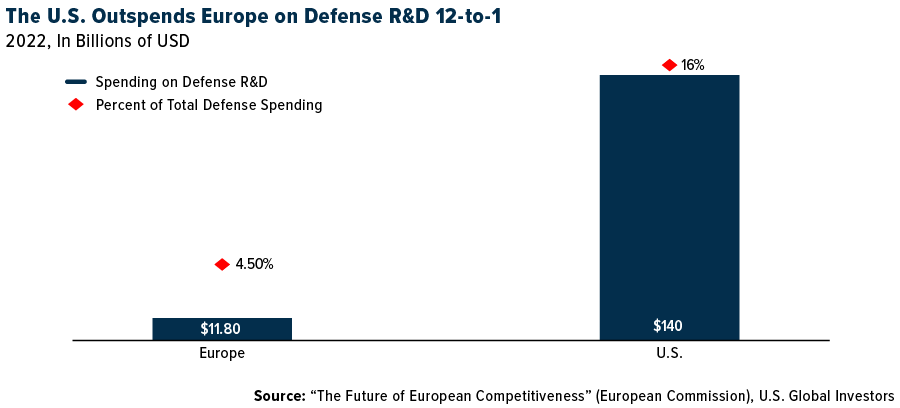

Draghi’s assessment highlights this vulnerability and argues for a significant shift in strategy. He points out that Europe’s defense R&D spending was a mere €10.7 billion ($11.8 billion) in 2022—about 4.5% of total defense spending—compared to the U.S., which spent a whopping $140 billion, or 16% of total defense spending. This isn’t sustainable if Europe hopes to become more self-reliant in defense, especially as tensions with Russia continue to escalate.

Indeed, the Russia-Ukraine conflict has forced European governments to rearm rapidly, and Draghi’s report underscores the urgency of the situation. Europe can no longer afford to sit on the sidelines of its own defense. Leaders are beginning to understand that their reliance on the U.S. must end if they are to build a robust defense strategy capable of handling threats from adversaries like Russia, which announced this week that it’s increasing the size of its army by 180,000 troops to 1.5 million active personnel.

Capitalizing on Europe’s Rearmament

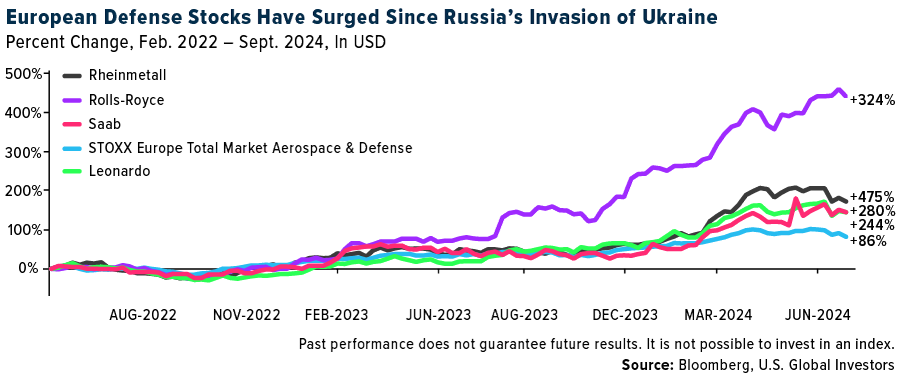

But here’s the kicker: While the demand for military equipment is skyrocketing, European arms manufacturers have been underutilized. Draghi’s call to action could be the catalyst that finally unleashes their potential. Germany, for example, has already ramped up its arms exports by 30% in the first half of 2024, and companies like Rheinmetall are reporting record-breaking orders. Rheinmetall’s CEO, Armin Papperger, recently said, “We have never seen such growth.”

The Düsseldorf-based company is benefiting from increased defense spending across the European Union (EU) and the North Atlantic Treaty Organization (NATO), along with significant orders from Ukraine. Rheinmetall’s strategic foresight—investing early in defense te1chnology, starting in 2014 when Russia first invaded Crimea—has paid off handsomely.

With an expected annual sales growth of €2 billion ($2.2 billion) in the coming years, Rheinmetall is, I believe, a solid play for those looking to capitalize on Europe’s rearmament. (Germany announced this week it would temporarily suspend weapons exports to Israel while it deals with “legal challenges,” Reuters reports.)

Then there’s Thales, one of France’s largest defense contractors. The company has seen record orders in 2024 due to increasing military budgets, with its earnings before interest and taxes (EBIT) margin hitting a new all-time high of 11.5% in the first half of the year.

Thales recently secured three contracts worth over €500 million ($556 million) each, making it one of the best-positioned defense stocks in Europe today. We believe its mix of advanced defense tech and a diverse portfolio makes it a potentially attractive option for investors looking for both growth and stability.

Surge in Defense Funding Bucks Broader VC Downturn

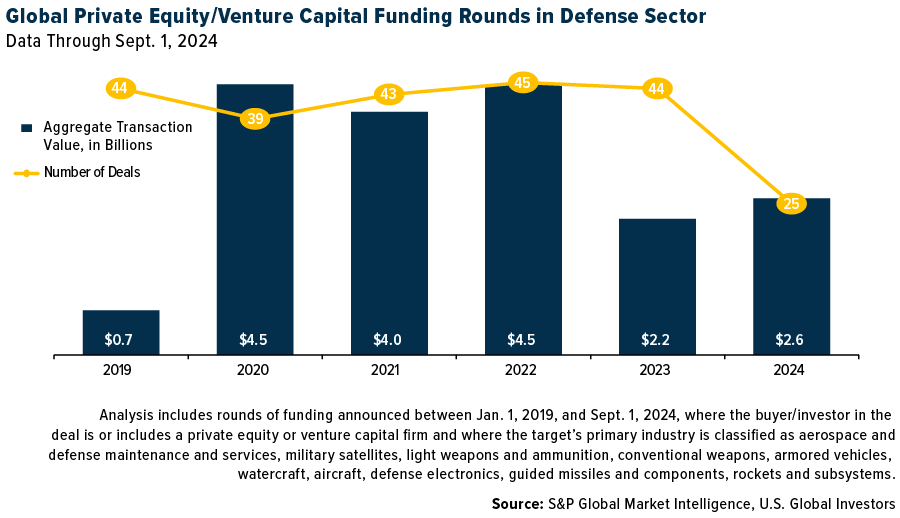

What’s even more compelling is the influx of private equity and venture capital into the defense sector.

As of September 1, 2024, nearly $2.6 billion has been poured into 25 funding rounds, surpassing the full-year total for 2023, according to S&P Global.

This surge in investment contrasts with the broader decline in venture capital funding across most sectors this year. Defense is clearly becoming a priority for investors, and this trend is only expected to grow as Europe gears up for increased military expenditures.

U.S. Election a Wildcard

One wildcard in this equation is the upcoming U.S. presidential election. Analysts at Alpine Macro suggest that a Donald Trump victory could lead to reduced global geopolitical risks. If reelected, the former president might push Ukraine to negotiate a peace deal with Russia, which could de-escalate the conflict and stabilize Europe’s defense outlook.

A Kamala Harris presidency, on the other hand, could exacerbate tensions, as her perceived inexperience might embolden adversaries like Russia and China to test her administration’s resolve, Alpine Macro says.

Despite spending more on its military than the next nine countries combined, the U.S. is, like Europe, contemplating raising defense spending to meet new geopolitical challenges. Speaking before Congress this week, Jane Harman, Chair of the National Defense Strategy (NDS), recommended that the U.S. return “to the levels of spending on national defense, proportionally, as we did in the Cold War.”

That would be a tall order. The U.S. currently spends 3.7% of its GDP on national defense, down significantly from the 15% to 16% it was spending at the height of the Cold War in the early 1950s.

Regardless, European nations will continue to rearm, as they can no longer depend solely on the U.S. for their defense.

The Draghi report should serve as a clarion call for investors. European nations are waking up to the reality that they need to ramp up their own defense capabilities, and arms manufacturers like Rheinmetall, Thales and others are primed to benefit. With the war in Ukraine showing no signs of slowing and geopolitical risks remaining high, there’s hardly been a better time to consider adding European defense stocks to your portfolio.

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 1.62%. The S&P 500 Stock Index rose 1.36%, while the Nasdaq Composite climbed 1.49%. The Russell 2000 small capitalization index gained 2.08% this week.

- The Hang Seng Composite gained 9.77% this week; while Taiwan was up 1.84% and the KOSPI rose 0.70%.

- The 10-year Treasury bond yield rose 8 basis points to 3.742%.

Airlines and Shipping

Strengths

- The best performing airline stock for the week was Wizz, up 11.5%. The Department of Transportation (DOT) approved the Alaska Air and Hawaiian Airlines merger this week. According to the DOT, Alaska and Hawaiian are required to protect the value of rewards, maintain existing service on key Hawaiian routes to the continental U.S. and inter-island, guarantee fee-free family seating, and ensure competitive access at the Honolulu hub airport. The protections will remain in place for six years.

- According to Morgan Stanley, air cargo spot rates have hit a new high in the first week of September, as the industry braces for transpacific-heavy demand in the fourth quarter. Average global spot rates went up 6%, according to WorldACD, 30% higher than a year earlier.

- RBC views Air Canada’s four-year collective agreement with its pilot union as neutral. While terms of the new agreement will remain confidential pending a ratification vote and board approval, reports from media outlets point to a 42% pay raise over four years (26% raise retroactive to September 2023, plus 4% raises thereafter).

Weaknesses

- The worst performing airline stock for the week was Embraer, down 5.0%. According to ISI, airline web traffic declined 7% year-over-year for the week, versus down 3% in the trailing four-week period. This implies future demand for airline tickets may be soft.

- According to ISI, shipping rate seasonality is beginning to look like one of those exception years as current spot rates are about $8,000 per day below July levels (with no sign of seasonal uplift yet). Chinese LNG demand has been flat year-over-year for the past few months, and European gas storage seems adequate.

- Ryanair CEO Michael O’Leary said that a prolonged Boeing workers’ strike may cut the number of aircraft it receives by next summer to 20 from an anticipated 25. O’Leary said his low-cost Irish airline, one of Boeing’s largest customers, was supposed to receive 30 737 MAX aircraft before summer 2025 but Boeing’s operational issues had already brought that number down to 25.

Opportunities

- RBC is optimistic on expected production and delivery plans into 2025 (its target is 810 deliveries) and sees the industry holding at a 1x book-to-bill into 2025. While the group views the outlook as generally positive for the business jet outlook, they called out a significant mix shift to fractional ownership, which can be a positive for higher utilization levels (but can also limit individual sales). Declining interest rates are not expected to be a tailwind.

- According to UBS, the major users of the de minimis rules are concerned about the potential implementation of the executive order in November that may lead to front loading of e-commerce volumes. This would likely have a positive impact on air freight rates and would increase demand for Express block space in October and early November.

- Boeing announced several measures to preserve cash while protecting funding for safety, quality and customer support. These measures include a hiring freeze, postponement of salary increases, and potential temporary furloughs within its workforce. Boeing will also eliminate all first and business-class air travel and suspend spending on external consultants and non-essential temporary workers.

Threats

- Frontier lowered November capacity by 910 basis points (bps), reports Bank of America, with domestic and Latin American flying each seeing cuts at 940/730bps, respectively. This could imply slower future growth.

- The Biden administration has announced plans to crack down on de minimis exemptions which allows the import of products without duties if they have a value below $800. This extends to more than 40% of U.S. imports and more than 70% of textile and apparel imports. The Biden administration also called on Congress to pass legislation to comprehensively reform the exemption, and Bank of America notes the EU is also investigating similar measures.

- According to JPMorgan, several questions still surround Qantas. First, the size of the capex bill as fleet renewal gathers pace is a core consideration, as is whether current conditions are “as good as it gets” and represent peak cycle earnings. This is in addition to other peripheral issues which are abating and remove an overhang on the stock as sentiment improves. Regarding Qantas’ capex profile, they accept it is high.

Luxury Goods and International Markets

Strengths

- The U.S. reported strong economic indicators this week. Retail sales in August increased by 0.1% month-over-month, defying expectations of a 0.2% decline. Housing starts for August reached 1.356 million, surpassing the consensus estimate of 1.325 million. Additionally, the New York Fed Empire Manufacturing Survey for September reported a figure of 11.5, significantly better than the forecast of -5.0 and August’s reading of -4.7.

- BNP Paribas Exane upgraded Hermès from neutral to outperform, citing the brand’s strong performance this year within the luxury sector. The brokerage believes Hermès will continue to outpace its competitors. Year-to-date, Hermès shares have risen by 1%, while the S&P Global Luxury Index has declined by 7%.

- RealReal, an online marketplace, was the best performing S&P Global Luxury stock, gaining 20.45% for the week. The company was given an “outperform” rating at Northland.

Weaknesses

- Goldman Sachs and Citigroup downgraded China’s growth forecast to 4.7% for 2024. The country continues to release disappointing economic data with industrial output slowing to a five-month low in August.

- European car sales fell by 18.3%, reaching a three-year low, with electric vehicle sales dropping by 43.9%. This decline has led the European Automobile Manufacturers Association (ACEA) to urgently call for the EU to postpone the new emissions targets set for 2025.

- Ermenegildo Zegna was the worst-performing S&P Global Luxury stock, losing 14.9% in the past five days. The company’s shares declined after reporting financial results this week.

Opportunities

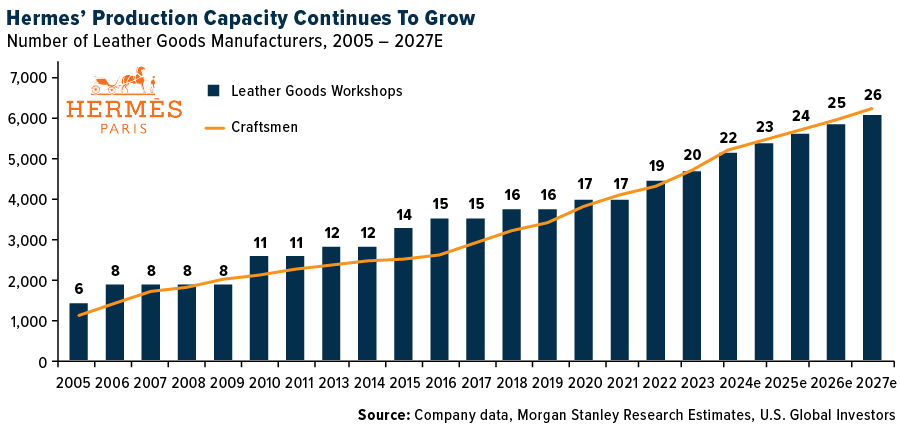

- Hermès recently announced the opening of its 23rd leather goods workshop in France. In 2005, the company operated five manufacturers, but it has steadily increased production capacity since then. Morgan Stanley estimates that Hermès will open three more workshops over the next three years.

- Central banks worldwide are continuing to cut interest rates. Last week, the European Central Bank reduced its deposit rate by 25 basis points, bringing it down from 3.75% to 3.5%. This week, the Federal Reserve lowered rates by 50 basis points. This ongoing global easing cycle is expected to support economic growth and boost consumer spending.

- Burberry’s new CEO, Joshua Schulman, formerly of Michael Kors, aims to revitalize the struggling brand. Burberry’s shares have plummeted over 50% year-to-date, and earlier this month, the company was removed from the FTSE 100 Index, ending its 15-year presence in the blue-chip index after its market capitalization fell below the minimum requirement for inclusion.

Threats

- Zuzanne Pusz, the head of European Luxury Research at UBS, is expecting weakness in the luxury sector to last longer than previously expected. She is predicting slower sales growth, and further margin pressure, recommending remaining defensive and having exposure to well positioned companies like Hermes, Brunell Cucinelli and Richemont.

- Mercedes-Benz Group sold the remaining stake in Denza to BYD in a wake of disappointing sales in China. Denza was established by BYD and Mercedes in 2010 with a mission to create a leading premium brand of EV and hybrid cars. Each company initially held a 50% stake, but Mercedes lowered its interest to 10% in 2021. BYD, a prominent Chinese electric vehicle manufacturer, has been effectively pushing foreign EV competitors out of the market. The company cut the growth outlook mainly due to slower demand in China, sending shares lower on Friday.

- Bloomberg reported that the real reason luxury stores are seeing fewer customers in China is the rise of China’s daigou trade, which means “buying on behalf of.” This business focuses on importing lower-priced goods from abroad and reselling them in China at higher prices. The daigou trade has been growing due to arbitrage opportunities, as luxury goods are generally cheaper in Europe and the U.S. According to Bernstein’s analysis, shoppers in Beijing pay, on average, 24% more for luxury items than they would in Paris, while the U.S.is the second most expensive market, with a 16% markup.

Energy and Natural Resources

Strengths

- The best performing commodity for the week was sugar, up 17.16%, as fires and drought evaporate and wilt crops in Brazil, threatening a potential shortfall in supply from the world’s biggest producer of sugar. According to JPMorgan, liquefied natural gas (LNG) spot prices have continued to strengthen, leading into the Northern Hemisphere winter. Average prices in August were the highest since November 2023 and more than 60% above the trough in February 2024. With no incremental capacity online so far this year, existing plants are operating above usual utilization levels.

- Oil jumped as Libyan exports continued to slump and expectations rose that the Federal Reserve will be more aggressive in cutting rates this week. West Texas Intermediate (WTI) advanced more than 2% to settle above $70 a barrel while Brent futures settled just shy of $73 a barrel. Libyan exports have declined markedly as United Nations-led talks failed to break an impasse over control of the central bank, which has spilled over into its oil industry, according to Bloomberg.

- According to RBC, uranium equities were up on commentary from Russian President Vladimir Putin discussing possible restrictions on exports of uranium and other critical materials in response to Western sanctions; for context, in 2023, Russia supplied 10-15% of the U.S.’s and 20-25% of Europe’s enriched uranium requirements.

Weaknesses

- The worst performing commodity for the week was wheat, dropping 4.25%, on lack of buyers on good weather conditions in U.S. potentially boosting crop yields, as reported by Bloomberg. According to RBC, fertilizer equities were down two weeks in a row, along with broader materials sector weakness and lack of movement in fertilizer markets. Fertilizer prices across the board have continued to trade within a very narrow range since Q2, while crop prices softened and pressured affordability.

- According to Bank of America, the manganese ore price fell to $3.65, down 20 cents on the week. “Port stock prices continue to go down. I do not think there is any buyer around to pay $4/mt for semi-carbonated ores,” a trader said. “There is no taker for this offer,” sources from China and India said.

- According to Goldman, four factors have weighed on refining profitability recently: (a) global oil demand weakness, particularly in Asia and China, (b) seasonality, with gasoline rolling from summer to winter grade, (c) elevated refining utilization after a heavy turnaround period earlier this year, and (d) tight inland crude differentials, with Brent-WTI tightening up to $3/barrel versus the two-year average close to $5/barrel.

Opportunities

- Bank of America attended the 2024 edition of the annual World Nuclear Association (WNA) Symposium. Key takeaways include: (1) a robust outlook for nuclear growth; (2) still growing skepticism about the supply of nuclear fuel; and (3) uncertainty about near-term uranium (U3O8) prices (but generally constructive). Reinforcing that trend, On Friday, Constellation Energy Corp. announced they are restarting the remaining nuclear reactor at Three Mile Island after it was mothballed in 2019 for $1.6 billion and sell the electricity directly to Microsoft Corp. Constellation’s latest balance sheet only shows $311 million in cash, so this marks a huge step in AI companies securing an energy source with zero carbon emissions.

- Kathleen Quirk, CEO of copper miner Freeport-McMoRan, said that if the red metal “went from $4 per pound today, roughly, to $6 per pound a month from now, there’s very little that the industry can do in any short period of time to respond to that.” She added that “It used to be you could develop a new mine within three or four years, and that has extended to 10 years or more. And so that’s why Freeport has focused on the brownfield opportunities.”

- Canada and Mexico are drawing tens of billions of dollars of investment to kick-start their LNG export industries as a permitting freeze slows the expansion of the sector in the U.S., the world’s biggest supplier. Roughly $63 billion of capital investment is poised to pour into the sector in the two countries, according to consultancy Rystad Energy, including projects under construction and those awaiting final investment decisions.

Threats

- According to UBS, demand remains the key downside risk to oil prices, with a slowing Chinese economy in focus. Global demand growth should be lower by 0.1 million barrels per day (Mb/d) to 1 Mb/d in 2024. Their Chinese demand growth forecast is down by 0.1 Mb/d to 0.3 Mb/d, consistent with a downward revision to UBS’s Chinese GDP forecast of 4.6%.

- According to Goldman, the risk to oil is the risk that relatively comfortable inventory levels allow the market to already price in the expected 2025 surplus, which would hinder the recovery in valuation. If the present undervaluation were to sustain at the 25th percentile of history, this would leave Brent in the fourth quarter at $72/barrel or $5 below their base case.

- Oil and gas production in the North Sea could halve by 2030, far faster than currently expected, under tax proposals that would cause “irreversible damage” to the sector, according to a report from energy consultants Wood Mackenzie. North Sea oil and gas companies have already dramatically scaled back their activity while they wait for a decision on taxes in next month’s Budget. “The ongoing uncertainty makes planning extraordinarily hard and financing all but impossible,” said the report. Companies will have to pay 78% tax from November, after an increase in the “energy profits levy.”

Bitcoin and Digital Assets

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performer for the week was Sui, rising 44.04%.

- Bitcoin rose this week, the biggest move in over a month, as expectations increased that a reduction in borrowing rates by the Fed would boost demand for speculative assets. Bitcoin gained as much as 6.4% on Tuesday, Bloomberg reports, the biggest intraday increase since August 8.

- Hedge fund manager Anthony Scaramucci predicts record highs for Bitcoin, Bloomberg reports, fueled by a combination of interest-rate cuts and U.S. crypto regulatory clarity in the wake of November’s presidential election.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performer for the week was Helium, down 12.87%.

- The German Attorney General’s Office and the country’s Federal Criminal Police Office have shut down 47 crypto exchanges allegedly tied to criminal activities including money laundering. The exchanges purposefully failed to comply with KYC requirements, according to an article published by Bloomberg.

- DeFi platform Delta Prime has been hit with a $6 million exploit after an admin lost control of a private key. The hacker initially drained about $4.5 million, Bloomberg explains, but was able to continue attacking the protocol to steal funds.

Opportunities

- Crypto venture capital firm Dragonfly Capital is seeking to raise $500 million for its fourth fund, which will invest in early-stage projects. The firm has raised $250 million so far and aims to close the fundraising in the first quarter of next year.

- SIX group is exploring the creation of a venue in Europe for trading cryptocurrencies, Bloomberg reports. The venue would be available only for institutional investors and can help facilitate trading whether it’s spot crypto or derivatives.

- Crypto exchange Bitget bought $30 million of Toncoin, the token linked to messaging app Telegram. The purchase came shortly before Telegram CEO Pavel Durov was arrested in France setting off a tumble in Toncoin.

Threats

- The hackers behind a cyberattack against the drug distributor Cencora Inc. received a total of $75 million in the largest known cyber extortion payment ever made. The payment made for the Cencora hack occurred in three installments in Bitcoin, writes Bloomberg.

- The official YouTuber channel of the supreme court of India that was used for streaming proceedings was compromised by hackers. The channel hosted videos relating to a cryptocurrency product and the entire page was deleted, according to Bloomberg.

- Two California men were indicted with conspiracy to steal and launder over $230 million in cryptocurrency. According to the DOJ, the scammers gained access to victim cryptocurrency accounts and then transferred victim funds into their possession which they laundered through various mixers and exchanges.

Defense and Cybersecurity

Strengths

- BAE Systems Australia secured a $270 million contract to boost production of critical components for the Evolved SeaSparrow Missile (ESSM) Block 2. This will expand its workforce while supporting Australia’s sovereign defense capabilities (and also contribute to the missile’s deployment on naval warships).

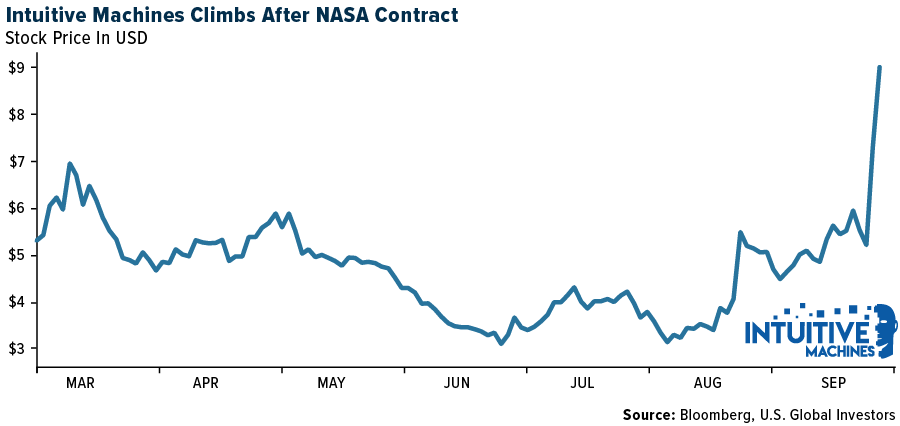

- Intuitive Machines won a NASA contract worth up to $4.82 billion to provide communication and navigation services for lunar missions, including support for the Artemis campaign to establish a long-term presence on the moon.

- The best performing stock in the XAR ETF this week was V2X Inc., rising 7.67% after news that insiders purchased shares in early September.

Weaknesses

- European defense stocks saw their biggest drop in five months, led by Rheinmetall’s 6.7% fall, as Ukraine’s allies considered a potential cease-fire, with sector baskets from Goldman Sachs and UBS also seeing significant declines.

- Israel is planning another military operation in Lebanon, which could potentially escalate into a third Lebanon war. They are already transporting heavy military equipment to the border, amassing forces, and have launched a massive airstrike on targets in southern Lebanon.

- The worst performing stock in the XAR ETF this week was Virgin Galactic, falling 10.16%, due to bearish flows and large amounts of puts trading.

Opportunities

- Ukraine claimed it destroyed a large stockpile of Russian missiles, including Iskander and Tochka-U, using long-range drones in an attack on a depot located about 500 kilometers from the Ukrainian border in Toropets, Russia.

- Sweden has agreed to lead NATO’s defense base in Finland as part of the alliance’s effort to bolster its defenses against Russia, marking a deepened security collaboration between the two nations within NATO.

- Raytheon and Northrop Grumman successfully tested a new long-range solid rocket motor designed for hypersonic applications. This marks a significant milestone in their collaboration and highlights the growing importance of long-range missile technology amid global defense concerns, particularly in the context of the Ukraine conflict.

Threats

- Icom Inc. stopped producing the walkie-talkies involved in Lebanon’s recent explosions a decade ago, warning that most IC-V82 radios on the market are counterfeit. Investigations continue into how these devices were modified with explosives, killing at least 26 people.

- U.S. authorities accused Iranian hackers of sending stolen information from Donald Trump’s campaign to Joe Biden’s team and journalists. This comes as part of a spear phishing effort, though there is no evidence Biden’s team responded.

- Huntington Ingalls is facing pressure to improve labor productivity amid strong Navy ship demand, leading JPMorgan to downgrade its stock rating to neutral while raising the target price to $285.

Gold Market

This week gold futures closed the week at $2,645.40, up $34.70 per ounce, or 1.33%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher/lower by 1.05%. The S&P/TSX Venture Index came in up 0.77%. The U.S. Trade-Weighted Dollar fell 0.33%.

Strengths

- The best performing precious metal for the week was gold, up 1.33%. According to Canaccord, New Gold released an update on its ongoing exploration program at its New Afton mine, located in British Columbia. The results demonstrate the potential to incrementally add to existing resources and grow the mine’s life. Canaccord highlights that no resource exists yet for the K-Zone, which the company has now expanded to an area 50 meters wide and 300 meters strike length. The zone remains open in all directions and drilling is ongoing.

- According to BMO, Lucara reported the recovery of another 1,000+ carat diamond from its Karowe mine. The 1,094 carat rough diamond shares similarities with last year’s 692-carat diamond, which yielded polished diamonds that were sold for $13 million by HB Antwerp.

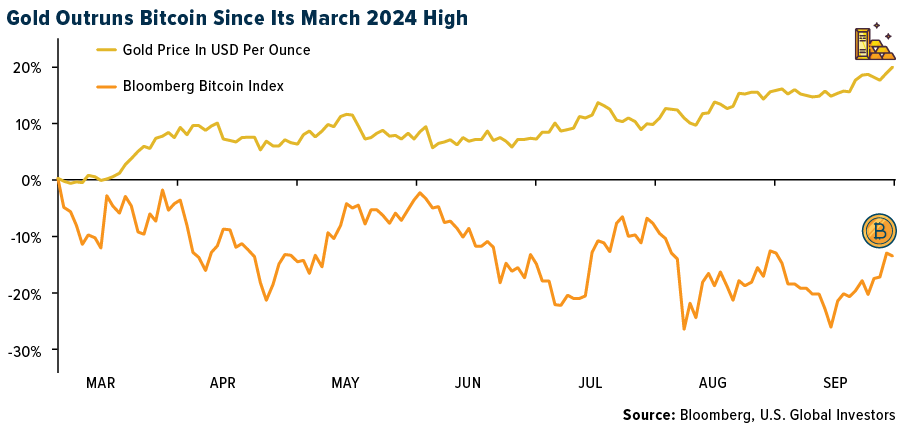

- Gold reached a new high of $2,622 an ounce on Friday as the Federal Reserve cut rates by an aggressive 50 basis points on Thursday, which triggered profit taking initially. Since the Bloomberg Bitcoin Index hit a record high on March 13, 2024, surrounding the various Bitcoin ETFs launchings, its performance relative to gold bullion has been underwhelming with a loss of 14% relative to gold’s gain of 20%.

Weaknesses

- The worst performing precious metal for the week was platinum, down 2.69%. Westgold Resources guided to group gold production of 400,000-420,000 ounces, which was 4% below RBC’s 426,000-ounce forecast. Production will be back-ended as the South Junction, Big Bell Deeps and Great Fingall projects are expected to commence production ramp-up in the second half of 2025.

- According to JP Morgan, Chinese demand for physical gold has remained subdued since May with net imports falling sharply in the last few months (-51% year-over-year in July) and onshore prices largely trading at a discount for most of the last couple of months.

- According to Morgan Stanley, the volume and value of rough diamond imports fell again in August, by 29% month-over-month and 54% year-over-year, and 26% MoM and 49% YoY, respectively. Both metrics remain below their five-year average range (ex-COVID), suggesting that the midstream producers are still in a de-stocking mode.

Opportunities

- According to Bank of America, gold has been creeping higher and they keep a call that the yellow metal should hit $3,000 per ounce once a sustained cutting cycle gets under way. Precious rallies have been driven by Chinese investors and central bank in recent months, while Western investors have not been major participants, so having the latter back is critical, as evidenced by the growing accumulation of new money flows going into the SPDR Gold Shares ETF.

- According to Scotia, in the junior mining space, there could be more sector mergers and acquisitions (M&A), project divestments/acquisitions, joint ventures (JVs) and minority investments. The average price-to-net-asset-value (P/NAV) valuation for their gold development universe is currently at 0.46 times earnings, which compares to 0.35 times earnings last year, a positive price change of 31% YoY, though still trading at a discount to their mid-tier producers at 0.65x P/NAV.

- In the past two weeks, the Precious Metals and the Denver Gold Forum have taken place at a time when we have had record gold prices. Attendance by industry members and was solid, but what was lacking was generalist investors on the scene. This highlights that despite the significant rise in gold bullion prices in recent years, there is a lot of money that hasn’t been paying much attention to the sector yet, and that is still the opportunity.

Threats

- Bank of America feels gold is getting into overbought territory, though it can stay there for a while. Meanwhile, ETFs have seen inflows, but assets under management remain comparatively low.

- According to Morgan Stanley, two U.S. senators have introduced a bill proposing to ban the import of critical minerals (including palladium, platinum, rhodium, ruthenium, nickel, copper and zinc) from Russia. As a result, unlike many other Western counterparties, the import data reflects that the U.S. has continued import sizable quantities of palladium sponge of Russian origin.

- Heraeus notes that “central banks are remaining committed to gold purchases, with net additions to reserves rising to 37 tons globally in June, despite the PBoC reporting zero purchases or sales for another month. Sales of gold fell to 4 tons in July and purchases also rose to the highest level since February. The Central Bank of Poland was the largest buyer in July, adding 14 tons during the month. High gold prices are not typically a headwind for central banks, which tend to buy gold as part of asset diversification programs and are therefore generally price-agnostic.”

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission (“SEC”). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product. Certain materials in this commentary may contain dated information. The information provided was current at the time of publication. Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content. All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (06/30/2024):

Alaska Air

Ryanair Holdings

Boeing

Qantas Airways

Hermès

BMW

Mercedes-Benz Group

New Gold Inc.

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The S&P Global Luxury Index is comprised of 80 of the largest publicly traded companies engaged in the production or distribution of luxury goods or the provision of luxury services that meet specific investibility requirements.

The New York Fed Empire Manufacturing Survey is a monthly survey conducted by the Federal Reserve Bank of New York to assess manufacturing conditions in New York State.

The S&P Global Luxury Index is a stock market index that tracks the performance of companies involved in the luxury goods sector. This includes businesses that produce high-end products such as fashion, cosmetics, jewelry, and luxury automobiles.