Investor Alert

PayPal, Kanye and CBDCs

Date Posted: October 14, 2022

Read time: 46 min

Readers of a certain age will remember Carnac the Magnificent, Johnny Carson’s recurring alter ego.

Readers of a certain age will remember Carnac the Magnificent, Johnny Carson’s recurring alter ego. As Carnac, the late-night host would list off three seemingly unrelated words, all of which answered a question that was sealed in an envelope that he held to his forehead.

Today we’re going to play the same game, with the answers being PayPal, Kanye (or Ye, as he’s now known) and central bank digital currencies (CBDCs). And the question: What are the consequences of financial hyper-centralization?

Some of you will make the connections immediately. For everyone else, let me explain.

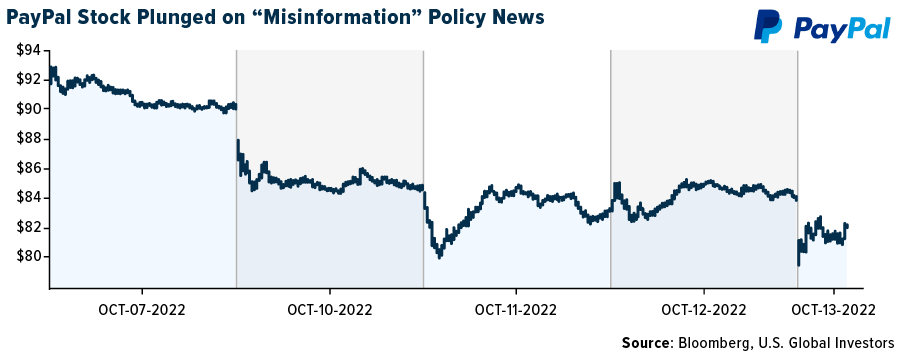

PayPal, the financial technology (fintech) firm cofounded over 20 years ago by Peter Thiel, Elon Musk and others, was roundly criticized this week after an update to its terms of service showed that the company would fine users $2,500 for, among other things, spreading “misinformation.” A PayPal spokesperson was quick to walk back the update, even claiming that the language “was never intended to be inserted in our policy,” but the damage was done. #DeletePayPal started trending on Twitter, and the company’s stock tanked nearly 12% this week.

As for Ye, he and his apparel brand Yeezy were reportedly dropped this week by JPMorgan Chase. In a letter widely shared on social media, JPMorgan says Ye has until November 21 to move his business finances elsewhere.

No reason was given for the bank to cut ties with the billionaire rapper, but it’s easy to surmise that Ye was targeted for his political beliefs and outspokenness. I don’t agree with everything he says, nor should you. He’s a controversial figure, and his comments are often erratic and designed to get a rise out of his critics. I’m not sure, though, that this alone should imperil his access to banking services.

The two cases of PayPal and Ye represent what I believe are legitimate and mounting concerns surrounding centralized finance. Admittedly, Ye is an extreme example. He’s a multiplatinum recording artist with tens of millions of social media followers. But there’s a real fear among everyday people that they too can be fined or have their accounts frozen or canceled at any time for expressing nonconformist views.

CBDCs Are Inevitable

That brings me to CBDCs. I was in Europe this week where I attended the Bitcoin Amsterdam conference, and I was honored to participate on a lively panel that was aptly titled “The Specter of CBDCs.”

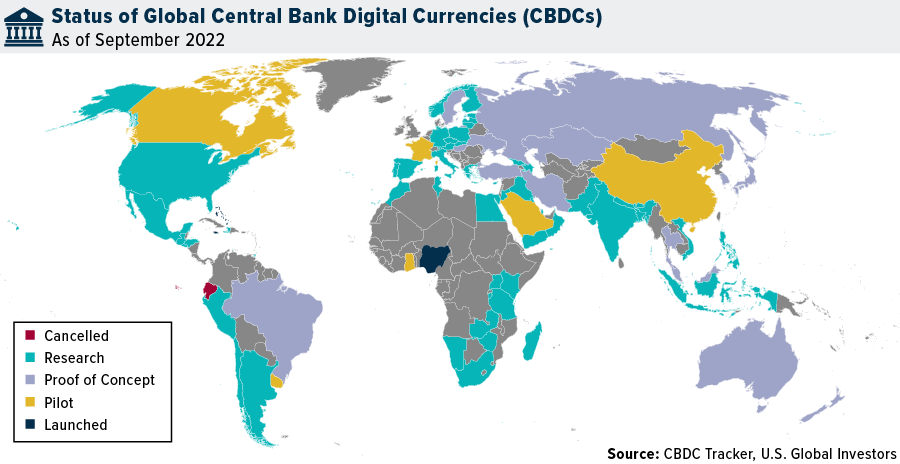

As I told the audience, I believe CBDCs are inevitable, ready or not. There are too many perceived benefits. These currencies offer broad public access and instant settlements, streamline cross-border payments, preserve the dominance of a nation’s currency and reduce the operational costs of maintaining physical cash. Here in the U.S., millions upon millions of dollars’ worth of bills and coins are lost or accidentally thrown away every year.

An estimated 90% of the world’s central banks currently have CBDC plans somewhere in the pipeline.

As I write this, only two countries have officially launched their own digital currencies—the Bahamas with its Sand Dollar, and Nigeria with its eNaira—but expect many more to follow in the coming years. China, the world’s second largest economy, has been piloting its own CBDC for a couple of years now, and India, the seventh largest, released a report this week laying out the “planned features of the digital Rupee.” A pilot program of the currency is expected to begin “soon.” And speaking at an annual International Monetary Fund (IMF) meeting, Treasury Secretary Janet Yellen said that the U.S. should be “in a position where we could issue” a CBDC.

CBDCs Improve Bitcoin’s Use Case

Due to the centralized nature of CBDCs, there are a number of concerns that give many people pause. Unlike Bitcoin, which is decentralized and anonymous, CBDCs raise questions about privacy, government interference and manipulation.

In the White House’s own review of digital currencies, issued last month, policymakers write that a potential U.S. coin system should “promote compliance with” anti-money laundering (AML) and counter-terrorist financing (CFT) laws. Such a system should also “prevent the use of CBDC in ways that violate civil or human rights,” and it should be sustainable; that is, it should “minimize energy use, resources use, greenhouse gas emissions, other pollution and environmental impacts on local communities.”

Nothing about this sounds inherently nefarious, but then, some of us may have said the same thing about PayPal’s “misinformation” policy (whether intended or not) and JPMorgan’s decision to end its relationship with a polarizing celebrity.

I believe this only improves Bitcoin’s use case, especially if we’re headed for a digital future.

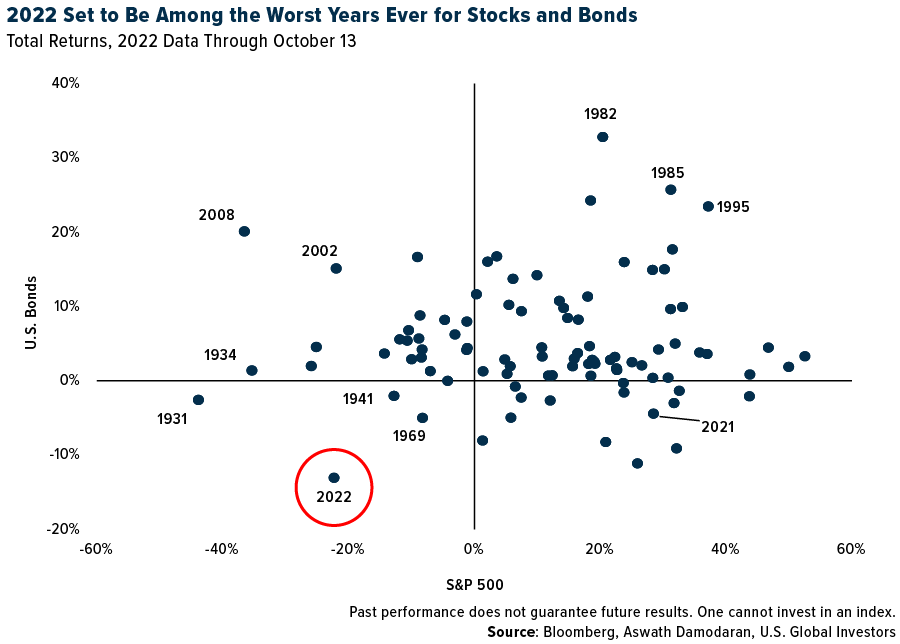

Worst 60/40 Portfolio Returns in 100 years

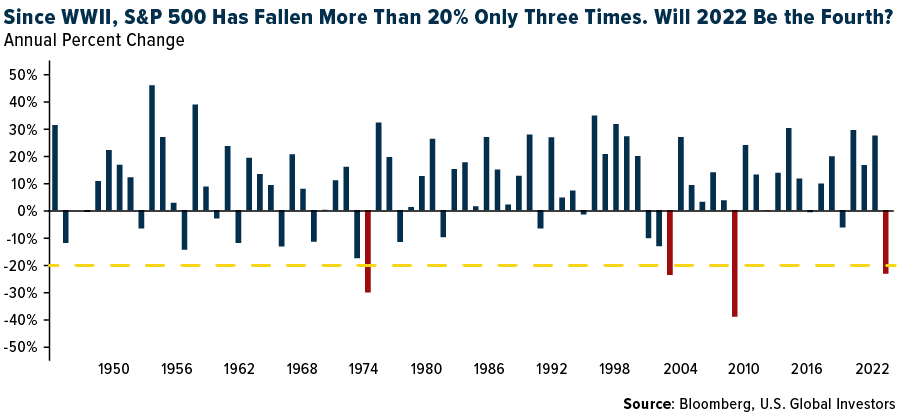

With only a little over 50 trading days left in 2022, it looks more and more likely that this will be among the very worst years in history for investing. Since World War II, there have been only three instances, in 1974, 2002 and 2008, when the S&P 500 ended the year down more than 20%. If 2022 ended today, it would mark only the fourth time.

Here’s another way to visualize it. The scatter plot below shows each year’s total returns for the S&P 500 (horizontal axis) and U.S. bonds (vertical axis). As you can see, 2022 falls in the most undesirable quadrant along with the years 1931, 1941 and 1969. Not only have stocks been knocked down, but so have bond prices as the Fed hikes rates at an historically fast pace.

What this means is that the traditional “60/40” portfolio—composed of 60% stocks and 40% bonds—now faces its worst year in 100 years, according to Bank of America.

My takeaway is that diversification matters more now than perhaps in any other time in recent memory. Real assets like gold and silver look very attractive right now. Real estate is an option. Bitcoin continues to trade at a discount. Diversification doesn’t ensure a positive return, but it could potentially spell the difference between losing a little and losing a lot.

You can watch my panel at Bitcoin Amsterdam by clicking here!

Index Summary

- The major market indices finished mixed this week. The Dow Jones Industrial Average gained 1.15%. The S&P 500 Stock Index fell 1.55%, while the Nasdaq Composite fell 3.11%. The Russell 2000 small capitalization index lost 1.16% this week.

- The Hang Seng Composite lost 5.94% this week; while Taiwan was down 4.19% and the KOSPI fell 0.91%.

- The 10-year Treasury bond yield rose 13 basis points to 4.016%.

Airlines & Shipping

Strengths

- The best performing airline stock for the week was Qantas, up 8.4%. Airline stocks are so cheap from a valuation standpoint, writes Yahoo! Finance, they ought to take off at a rapid pace – they just need the right series of catalysts, which might be taking shape. “With continued network restoration and lower assumed fuel [costs] next year, the case for traffic growth in 2023 (versus 2022) is obvious. Over time, capacity normalization should drive unit cost (and unit revenue) normalization,” Evercore ISI analyst Duane Pfennigwerth stated in a note to clients.

- American Airlines’ and United Airlines’ fourth quarter booked revenue – through the end of September – continues to exceed that of 2019 by a wide margin, continuing the trend established earlier this year. Chase daily card swipes for future travel have also strengthened and stabilized post-Labor Day.

- American Airlines updated its third quarter 2022 guidance. Management is now guiding revenue, unit revenue, and margins above the prior range. Capacity is expected to be at the lower end of the prior range with non-fuel unit costs at the higher end.

Weaknesses

- The worst performing airline stock for the week was Air China, down 16.3%. Boeing reported third quarter 2022 commercial deliveries of 112 aircraft, up from 85 in the same quarter last year, but down sequentially from 121 in the second quarter of 2022. The delivery numbers were mixed, reflecting a resumption of deliveries with the 787, however, 737 MAX deliveries were down 14% sequentially from the second quarter.

- For container shipping, spot freight rates have fallen 16 weeks in a row with the latest rates closing below $2,000, levels perceived by the industry as the “trough”. Against this backdrop, the three Asia-based container liners, COSCO Shipping, OOIL and Evergreen Marine, have seen drastic selloffs in recent months, reflecting concerns over whether this would be a bottomless downcycle, like the episode witnessed in the past decade.

- According to an 8-K released last week, damage from Hurricane Ian has potentially impacted the construction timeline of Allegiant’s Sunseeker Resort in Charlotte County, Florida. The resort was previously selling rooms for May 2023 but has since pushed back this selling date to September 2023. While the extent of the damage is largely unknown, as access to the resort has been limited since the storm, it appears the resort was protected by the seawall along the Charlotte Harbor and structures built above the mean high tide, according to management.

Opportunities

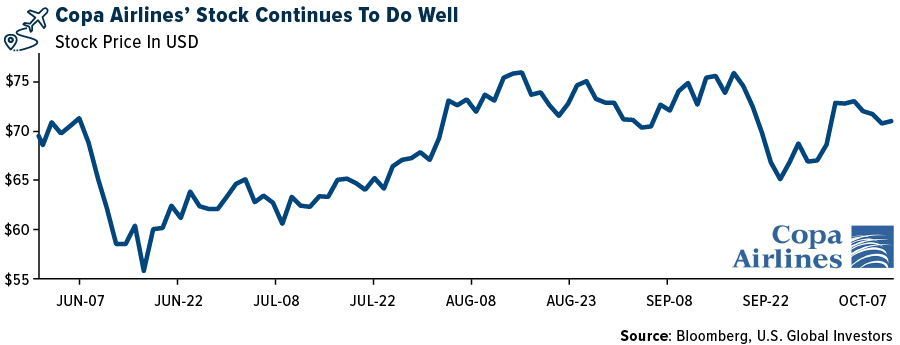

- According to Raymond James, while economic uncertainty persists, the group continues to believe Copa Airlines’ improved unit cost (versus pre-crisis) reaffirms a structural cost advantage, which along with its robust balance sheet and advantaged hub, serves as a formidable defensive moat. In addition, Copa is one of the first airlines to start returning cash to its shareholders, currently through buybacks (with $200 million in repurchases authorized this year), and the group expects a more meaningful dividend in 2023.

- Unadjusted global air freight demand in August was 2.9% below the same period in 2019, while seasonally adjusted volumes increased 1.0% month-over-month. Despite the sequential improvement, new export order manufacturing PMIs, which is a leading demand indicator, remain muted across most economies. August air freight capacity was down 8.0%, noticeably lower than June’s 6.0% decline relative to pre-COVID levels, as passenger airlines come off of the summer peak and as some freighter airlines park aircraft. With this, seasonally adjusted load factors improved to 49.1% in August from 48.9% in July.

- Joby announced a mutually exclusive partnership with Delta Air Lines across the U.S. and the U.K. for at least five years following commercial launch. This would integrate Joby’s airport offering into the Delta booking flow for a seamless customer experience. The exclusivity is applicable to the premium, differentiated service, offered alongside Joby’s standard airport service. In connection, Delta will make a $60 million investment in Joby, providing it with a 2% stake and option to appoint a board member.

Threats

- According to JPMorgan, for European airlines and airports, the bank sees: 1) continued air traffic recovery into the second half of the year on solid near-term demand commentary; 2) for 2023, JPMorgan airport traffic expectations look achievable, although it assesses there could be risks to passenger demand as high air fares meet lower household spending; 3) premium could outperform non-premium traffic, Europe could outperform U.K. and short-haul could be more resilient than long-haul leisure; and 4) airport retail could be squeezed.

- Many shippers may suspend service around China’s National Day holiday and sharply increase the number of idle vessels, with Sea Intelligence forecasting a 22%–28% reduction in tonnage on North American routes versus National Day-related pullbacks of 9%–11% in 2014–2018, and 15%–19% in 2019.

- After seeing a step up in large corporate volumes post Labor Day to -17.5% versus 2019, corporate trends have softened over the past three weeks. For the most recent week, large corporate consolidated net sales stepped back -29.3% versus 2019. Large corporate volumes decelerated to -26.4% versus 2019, while pricing was -3.8% versus 2019.

Emerging Markets

Strengths

- The best performing country in emerging Europe for the week was Turkey, gaining 1.7%. The best performing country in Asia this week was China, gaining 1.6%.

- The Hungarian forint was the best performing currency in emerging Europe this week, gaining 1.4%. The Indian rupee was the best performing currency in Asia this week, gaining 0.7%.

- This week China released September CPI data at 2.8% versus 2.9% expected. However, the CPI did increase from a prior reading of 2.5% in August, mostly due to higher pork prices.

Weaknesses

- The worst performing country in emerging Europe for the week was Romania, losing 2.2%. The worst performing country in Asia this week was Hong Kong, losing 5.9%.

- The Czech koruna was the worst performing currency in emerging Europe this week, losing 0.6%. The Thailand baht was the worst performing currency in Asia this week, losing 1.8%.

- Technology stocks listed in Hong Kong sold off this week on worries over new regulations coming out of the U.S. on chip exports, made with American technology, to China. Companies like Alibaba may not directly be involved in the semiconductor market, but many rely on U.S. chip technology to run and support their e-commerce, gaming, and internet search platforms.

Opportunities

- Hong Kong is considering easing property taxes and visa restrictions as authorities seek to reverse course of highly educated people leaving the region, which has threatened the city’s status as an international financial hub. The visa changes would make it easier for companies to hire non-local workers, while in terms of property taxes, it may relax rules on a 15% stamp duty that non-residents must currently pay.

- Xi Jinping is likely to be re-elected as head of the Communist Party in China, during the 20th Congress of the Chinese Communist Party (CCP), set to begin on October 16. The current president will most likely continue his current agenda of promoting national unity, economic stability, working toward supporting commonwealth, and making further plans for his country to overtake the United States as the biggest economy in the world.

- This week the President of Turkey met with the President of Russia in Kazakhstan. Turkish sources say that the government hopes to organize a summit in Istanbul on November 25 to propose a cease-fire and establish a committee to explore ways to return Ukraine and Russia’s borders to what they were in 2014. News about a cease-fire will be well welcomed by markets.

Threats

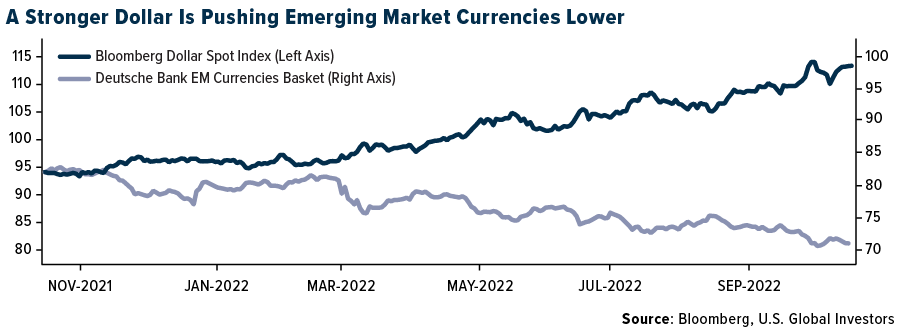

- On Thursday, the United States reported higher-than- expected inflation. CPI increased 0.40% in the month of September, while a 0.20% increase was expected. Year-over-year, CPI was released at 8.2%, above the expected reading of 8.1%. Following the news, the U.S. dollar spiked, pushing emerging market currencies lower. This trend may continue, as the Federal Reserve is expected to hike rates to bring inflation to a more desired level.

- The war in Ukraine intensified after last weekend’s explosion damaged parts of the bridge connecting Russia with Crimea. Supporters of Putin, believe that the Kerch Bridge is a symbol of Russia’s success in its illegal annexation on Crimea. Putin called the attack on the infrastructure a terrorist incident and shortly after launched missile attacks on cities throughout Ukraine. Ukraine did not claim its responsibility for the damage of the bridge, but Ukraine President Zelensky said “This is just the beginning.”

- According to the International Monetary Fund (IMF) global growth will slow from 6.0% in 2021 to 3.2% in 2022, and 2.7% in 2023. This is the weakest growth profile since 2001 except for the global financial crisis and the Covid pandemic. Global inflation is forecast to rise from 4.7% in 2021 to 8.8% in 2022 but could decline to 6.5% in 2023 and to 4.1% by 2024.

Energy & Natural Resources

Strengths

- The best performing commodity for the week was lumber, rising 9.78%. Lumber has largely been in rally mode since the start of the month but may have run its course with more jumbo rate hikes in the cards. After rallying three times since June, the commodity fell back to make new lows after each successive rally. In other news, nuclear power is getting a strong reboot in Europe due to the economy being too reliant on Russian power. French President Emmanual Macron wants 45 of France’s 56 nuclear power plants to be operational by January. Currently, only 30 are operating.

- The Biden administration is considering a complete ban on Russian aluminum — long shielded from sanctions due to its importance in everything from automobiles and skyscrapers to iPhones — in response to Russia’s military escalation in Ukraine. As reported by Bloomberg, the White House is eyeing three options: an outright ban, increasing tariffs to levels so punitive they would impose an effective ban, or sanctioning the company that produces the nation’s metal, United Co. Rusal International PJSC, according to people familiar with the decision-making.

- This week, a German expert commission proposed a package worth EUR96 billion to the government. The measure is primarily aimed at households and companies to ease the impact of high gas prices. Companies with consumption of more than 1.5MWh per year are eligible for the gas break, which includes BASF, Covestro, Siemens Energy, Thyssenkrupp, and other 24,000-25,000 firms.

Weaknesses

- The worst performing commodity for the week was coffee, falling 9.81%. Favorable crop conditions in Brazil are painting the picture of an improved supply from one of the top exporters of arabica coffee beans. U.S. gas in storage increased by 129 billion cubic feet (Bcf) last week, above the consensus of 116 Bcf, reaching 3,106 Bcf. U.S. natural gas futures are marking their eighth weekly decline and longest such streak since February 2001. The higher-than-expected build was driven by record production and a material decline in power burn, which fell below the three-year average. In addition, Germany announced they had reached 95% gas storage for the winter, taking some pressure off of international prices.

- European coal prices continue to move lower, now at $290 per ton from $400 per ton back in August. While the 50% lower TTF natural gas price since late August is likely to be a key driver of the European coal price correction, elevated coal inventories are creating an overhang as well.

- U.S. households face 25-year highs in heating bills to stay warm this winter, according to the Energy Information Administration. Consumers in the south that rely on natural gas, which has been falling in price, should expect to see an average power bill of $1,359, but homes in the north that rely on oil for heat, could see an average bill of $2,354. Diesel prices are soaring again too. In California, prices topped $190 per barrel, and New York harbor is slightly cheaper at $170 per barrel. According to Bloomberg, U.S. inventories of diesel are dangerously low ahead of the winter heating season.

Opportunities

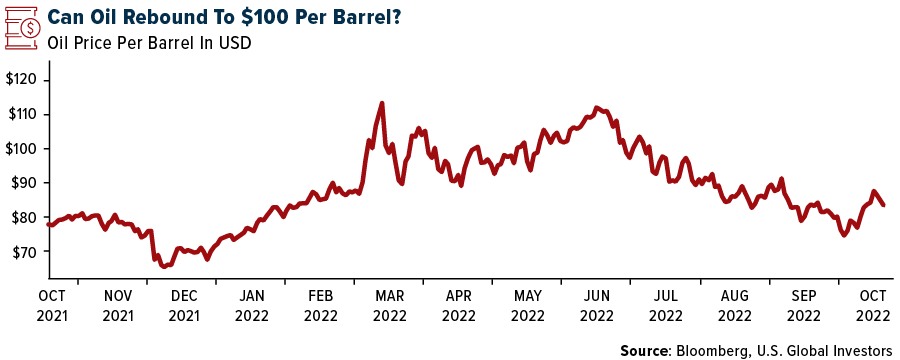

- JPMorgan’s Global Commodities team highlights five forecasted conditions needed for a fourth quarter 2022 oil price of $100/bbl to play out. These include: 1) demand needs to bounce 900mbd year-over-year in the fourth quarter; 2) sanctions on Russia need to constrain supply by 600mbd; 3) Saudi Arabia production needs to normalize from 11mmbd in September to a sustainable 10.6-10.7mmbd pace; 4) U.S. SPR releases need to end in October or sooner; and 5) the U.S. dollar needs to stabilize.

- BNEF released its latest Global Hydrogen Strategy Tracker. The tracker shows 35 countries now have a strategy around hydrogen development (up from 26 last year), with 17 currently preparing one. Of the 35 country-level strategies, 18 have a target for electrolyser capacity, which combined, point to 88GW by 2030, with 70% of this in the European Union.

- According to CIBC, despite looming recessionary concerns, the set up for energy remains attractive for investors. The capital discipline in the sector has provided a boon to free cash flow in this cycle and has increased shareholder returns that may stay. While the price targets remain grounded in modest forward cash flow multiples, CIBC does see room for multiple expansions for Canadian operators given the increased importance of energy security.

Threats

- Energy markets could remain constrained by output growth. Energy Aspects research suggests that shale oil in the U.S. is at risk of peaking in just two years. Currently, drillers are seeing rampant inflation matched by limited labor availability and some are considering cutting back on production next year unless prices go back up. Energy Aspects noted that none of the producers surveyed planned to boost production materially. OPEC+’s 2 million barrels per day cut, and limited growth in the U.S. oil production markets, could remain tight. However, a recession could be around the corner to slow down all markets.

- With retail gasoline prices now ticking back up in the past two weeks after declining for 14 straight weeks off a peak of $5 per gallon, a reemerging risk for refiners is now around a potential for a product export ban. This is particularly true given the tone of Secretary Granholm’s recent letter to the industry.

- Electric vehicle (EV) manufacturers, as well as small- and large-scale battery storage companies, have faced rising prices, shortages, and delays. China dominates in materials refinement and battery production, where it: 1) refines over 60% of the world’s lithium; 2) controls 77% of global battery cell capacity; and 3) manufactures 60% of the world’s battery components, resulting in U.S. companies regionalizing their supply chains. However, most of the produced lithium goes to EV companies, leaving uncertainty over how much domestic output will remain for stationary storage.

Luxury Goods

Strengths

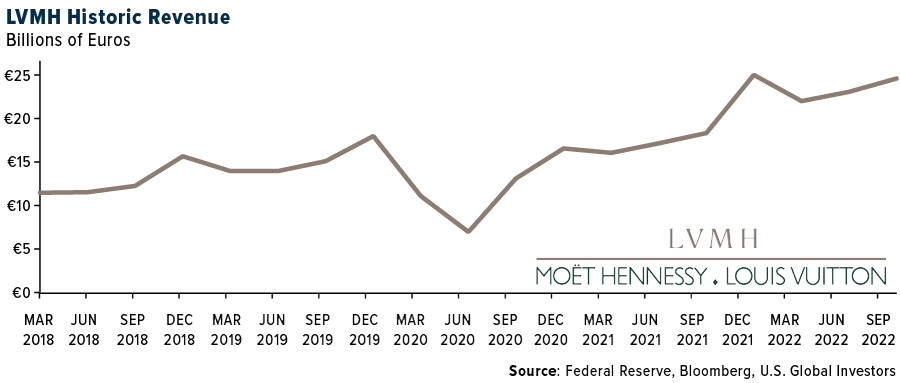

- According to Bloomberg, Louis Vuitton reported strong third quarter results this week, with sales jumping 22%. The company’s revenue was $54.8 billion in the first nine months of 2022, 28% higher than in 2021. Strong sales were supported by American shoppers, in particular taking advantage of the weaker euro, buying expensive goods in Europe, and simultaneously utilizing the record strong dollar.

- Sephora (a popular beauty retailer owned by LVMH) is back in the U.K. market with a new strategy focused on e-commerce, reports Vogue Business. To re-enter the market, the article explains, Sephora purchased British online retailer Feelunique for an undisclosed sum in 2021. This gives Sephora a leg up in the local market, as the website has 1.3 million active users.

- Brilliant Earth, a company selling jewelry that features diamonds and other gemstones, was the best performing S&P Global Luxury stock for the week, gaining 16.67%. The company recently filed for a $200 million mixed securities shelf offering, pushing the stock price higher.

Weaknesses

- As reported by CNBC, Peloton (a popular fitness equipment maker) is cutting another 500 jobs after multiple layoff rounds this year. The cuts amount to around 12% of the company’s total workforce, the article explains. CEO Barry McCarthy says the cuts should help position the struggling company to return to growth.

- According to Bloomberg, September’s U.S. CPI reading increased. It was reported at 0.4% versus a consensus of 0.2%, and a previous month reading of 0.1%. The reading represents a slight decrease in the purchasing power of Americans – the U.S. remains one of the leading luxury goods markets worldwide. In addition, this may give the Federal Reserve the green light to continue hiking rates in the U.S.

- Sands China, an integrated resort developer and operator in Macau, was the worst performing S&P Global Luxury stock for the week, losing 24.99%. As a result of the Chinese government’s support and commentary this week about the benefits of its zero-Covid policy, the stock fell 3% to HK$16.24, and this year has had a total return of around -11%.

Opportunities

- Big luxury brands like Gucci, Balenciaga, Hermès, Tiffany & Co., Fendi, Etro, and Dolce & Gabbana, are actively participating in the Metaverse as a different channel to reach new customers through “digital fashion.” For example, Gucci has created a Gucci Town, Balenciaga has a game to explore its newest digital collection, Tiffany & Co. has a “TiffCoin”, and Dolce & Gabbana even adapted its actual designs to fit into the Metaverse, (where the company also has its own Fashion Week, reports CoinTelegraph).

- Based on an article from Business of Fashion (BoF), one of the main goals of luxury and fashion companies now is to attract young consumers, especially Gen-Z (aged between 12 to 25, and digital natives). This generation represents 25% of the world’s population, and its purchasing power in the US is around $360 billion. According to a survey from BoF, 89% of this generation said that their favorite entertainment activity to spend money on is indeed fashion. This presents a massive opportunity for luxury brands to strategize and market appropriately to this sector.

- This week, Valentino launched its first dedicated career website, reports FashionUnited, highlighting life at the company and jobs available across its business units, from creative and design to retail and product development. The site has an international outlook, highlighting the different territories that Valentino operates in (and is available in Italian, English, Chinese, Japanese and Korean). As the article explains, it shares with prospective talent – and customers – a “window into Valentino’s world.”

Threats

- According to Bloomberg, the second-hand luxury watch market will reach $35 billion by 2030. This represents an increase of 75%, as reported by Deloitte and based on its consumer and watch brand executives survey. Young consumers will help reinforce this trend, as they view such pieces as investments. This comes as a wakeup call to luxury watchmakers, as sales in physical stores have seen a decline. This is one reason why well-known brands like Richemont purchased Watchfinder & Co. as its secondary market sales channel.

- China’s year-over-year retail sales will be released next week. Bloomberg economists predict sales to increase modestly by 3.2% in September versus 5.4% in August. This would represent a decrease of 40.7% in general consumption, pointing to weak consumer spending.

- China continues to defend its zero-Covid policy. This week, a National Health Commission panel expert said that the policy helps to reduce infections and save lives. On top of that, Beijing has new Covid rules. Due to new Covid cases, the city is asking new visitors to take two nucleic acid tests within three days of arrival and says these visitors cannot go to crowded places within seven days. Such measures could impact the global economy, at least in the medium-term, as it could spiral into more massive lockdowns in the world’s leading luxury goods market.

Blockchain & Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performer for the week was Huobi Token, rising 81%.

- Coinbase Global entered into a partnership with Alphabet Inc.’s Google over cloud services, its latest corporate pact after prior accords with BlackRock and Meta platforms. Google cloud will enable some customers, starting with those in the web3 industry, to pay using cryptocurrencies through Coinbase. Google will also use Coinbase Prime for institutional crypto services, writes Bloomberg.

- Tron founder Justin Sun said he owns “tens of millions” of Huobi Tokens and that he intends to try and boost the latter now that he’s an adviser to its linked crypto exchange. “I would see myself as one of the biggest holders,” of Huobi Tokens in the world, Sun said in a Bloomberg television interview with Emily Chang.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performer for the week was Klaytn, down 19.50%.

- The latest C-suite departure in the crypto sector comes from NFT marketplace OpenSea, where Brian Roberts has exited the role of chief financial officer after less than a year on the job. Roberts, who joined the NFT platform in December after seven years at ride-sharing firm Lyft, said in a LinkedIn post he’ll now be an adviser to OpenSea, according to an article published by Bloomberg.

- An attacker spirited away about $100 million from decentralized finance provider Mango by manipulating the price of its token in an exploit that wiped out depositors on the crypto platform. The heist began with two accounts funded with the stablecoin USD coin. The account took large positions in Mango perpetual futures, causing the price of the Mango token to spike. The price jump stoked an unrealized profit from the futures. The attacker used that to borrow and withdraw roughly a net $100 million from the protocol in a range of tokens leaving depositors with nothing, according to Mango.

Opportunities

- The head of New York’s financial regulator is looking to use the state’s role as a financial services hub to help set the regulatory agenda nationwide, with a particular focus on bringing order to the cryptocurrency industry. Superintendent Adrienne Harris said she intends to accomplish her goals partly by offering clearer guidance to banks and other financial institutions and by bolstering the resources her agency needs to do its job, writes Bloomberg.

- Uniswap Labs has secured more funding even as the crypto market struggles and investors start to lose confidence in decentralized finance. The exchange said it secured $165 million through a Series B funding round, reports Bloomberg, valuing the company at $1.66 billion. Uniswap said this is one of the largest funding rounds for a crypto firm since the market downturn this year.

- Binance has launched a $500 million fund to provide loans to Bitcoin miners struggling to cope with difficult crypto-market conditions. Binance pool, the company’s mining service, will provide loans for both private and publicly listed miners, writes Bloomberg.

Threats

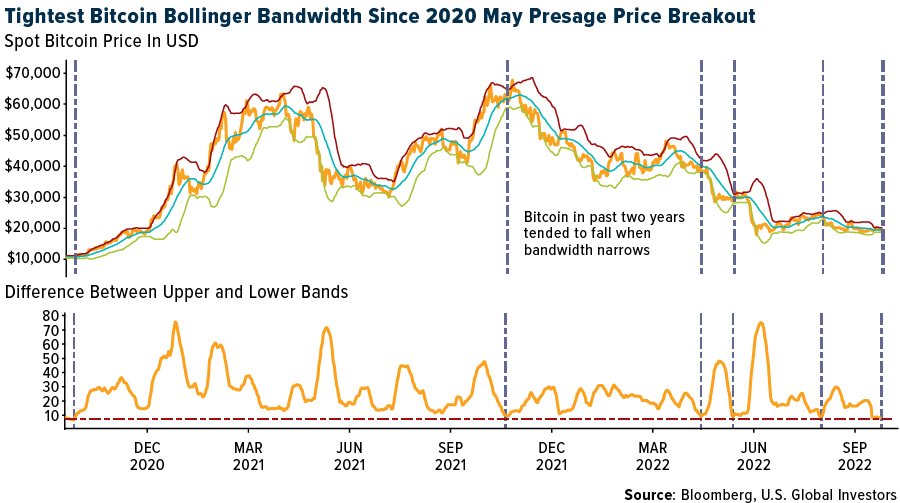

- The Bollinger Bandwidth for Bitcoin has shrunk to the narrowest since 2020. The bandwidth is the gap between the upper and lower band in a Bollinger study, a popular way of gauging volatility. The Bandwidth has been similarly narrow five other times over the past two years, according to data compiled by Bloomberg. On four of those occasions Bitcoin subsequently shed almost 16% over 20 days.

- The U.S. SEC is probing Yuga Labs, the creator of the Bored Ape Yacht Club NFT collection, over whether sales of its digital assets violate federal law, according to a report from Bloomberg. The issue is whether some of Yuga’s NFTs are closer to stocks, and thus should follow the same disclosure rules. The key legal question at the center of the probe, according to Bloomberg, is whether NFTs are securities, writes CoinDesk.

- The U.S. Treasury Department faces a second lawsuit over its August decision to sanction Tornado Cash, a crypto-mixing service that obscures sources of coin transactions. The lawsuit filed Wednesday claims the Treasury’s sanctions overstepped its authority and punished U.S. cryptocurrency investors, writes Bloomberg.

Gold Market

This week gold futures closed at $1,648.90, down $60.40 per ounce, or 3.53%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 6.85%. The S&P/TSX Venture Index came in off 4.43%. The U.S. Trade-Weighted Dollar rose 0.41%.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Oct-12 | PPI Final Demand YoY | 8.4% | 8.5% | 8.7% |

| Oct-13 | Germany CPI YoY | 10.0% | 10.0% | 10.0% |

| Oct-13 | CPI YoY | 8.1% | 8.2% | 8.3% |

| Oct-13 | Initial Jobless Claims | 225k | 228k | 219k |

| Oct-17 | China Retail Sales YoY | 3.5% | — | 5.4% |

| Oct-18 | Germany ZEW Survey Expectations | -66.7 | — | -61.9 |

| Oct-18 | Germany ZEW Survey Current Situation | -69.0 | — | -60.5 |

| Oct-19 | Eurozone CPI Core YoY | 4.8% | — | 4.8% |

| Oct-19 | Housing Starts | 1,475k | — | 1,575k |

| Oct-20 | Initial Jobless Claims | 235k | — | 228k |

Strengths

- The best performing precious metal for the week was platinum, but still off 1.84%. Traders flipped to net bullish on platinum’s long position this week. Fortuna Silver reported third-quarter production of 1.84 million ounces of silver and 66,000 ounces of gold, above consensus of 1.63 million ounces and 63,000 ounces, respectively. The beat in silver production was primarily driven by higher throughput and grades at San Jose. Silver production from Caylloma of 292,000 ounces also came in above consensus of 262,000 ounces, driven by higher grades and throughput.

- K92 Mining mill throughput of 117,938 tons (1,282 tons per day) significantly exceeded consensus of 95,000 tons, as the process plant continued its strong performance and growing throughput capacity ahead of the Stage 2A expansion flotation upgrades, on track for late fourth quarter 2022 or early first quarter 2023. Throughput was 35% higher than in the third quarter of 2021 and set a new quarterly record at Kainantu.

- Centamin PLC reported it is in the final stages of commissioning its 36MW solar power plant at the Sukari Gold Mine in Egypt. Initial work shows the plant is delivering above expectations and could offset $20 million in annual cost for diesel prices. Separately, the mine’s application for grid power has been received by the government. Should all approvals take place, full integration could start in 2024.

Weaknesses

- The worst performing precious metal for the week was silver, down 10.24%, with hedge fund managers cutting their net-long position to the lowest in five weeks. Barrick Gold reiterated it would achieve the low end of its gold production guidance, (a 19% production improvement is required quarter-over-quarter for this) and could be at or slightly below the low end of production guidance, (and costs well above the top end of prior guidance). The company reported production of 990,000 ounces (down 10% versus consensus). Gold costs were also higher, with TCC guided to be up 3%-5% quarter-over-quarter and AISC guided to be up 3%-5% quarter-over-quarter. Gold production declined 5% quarter-over-quarter, disappointing versus prior guidance.

- Superior Gold said Wednesday that it has cut production guidance for full-year 2022 after it suspended mining and development activity at the main pit of its Plutonic gold mine in Western Australia. The company attributed the stoppage to the site’s underperformance linked to labor shortages and contractor issues. The miner, which dropped over 30% on Wednesday, now expects to produce 62,000 to 65,000 ounces of gold in 2022 compared to the previous target of 69,000 to 75,000 ounces. The open pit amounted to roughly 10% to15% of production this year as it made better sense to re-deploy resources toward additional underground development.

- Osisko Gold Royalties earned 23,850 attributable gold equivalent ounces (“GEO”) in the quarter, excluding Renard, below the Visible Alpha consensus 26,700 GEO. Preliminary revenues were C$53.7M and costs C$4.4M for record quarterly cash margin of C$49.3M, below the consensus C$49.9 million.

Opportunities

- Torex Gold Resources reported strong third-quarter gold production of 122,200 ounces, a 10% increase over the same quarter last year. The solid result was the result of high mill throughput and record metallurgical recoveries. Thanks to the result, the company is guiding toward the high end of full-year 2022 guidance of 430,000-470,000 ounces gold, which considers lower expected fourth quarter production for planned maintenance activities.

- New Gold announced the receipt of the key permit amendment enabling mining of the C-Zone at New Afton after market close on Friday, October 7. The official receipt is a catalyst for the stock, and partially de-risks development of the new zone through 2022-2023.

- There’s a global migration underway in the gold market, as western investors dump bullion while Asian buyers take advantage of a tumbling price to snap up cheap jewelry and gold bars. Rising rates that make gold less attractive as an investment mean that large volumes of the metal are being drawn out of vaults in financial centers like New York and heading east to meet demand in Shanghai’s gold market and Istanbul’s Grand Bazaar.

Threats

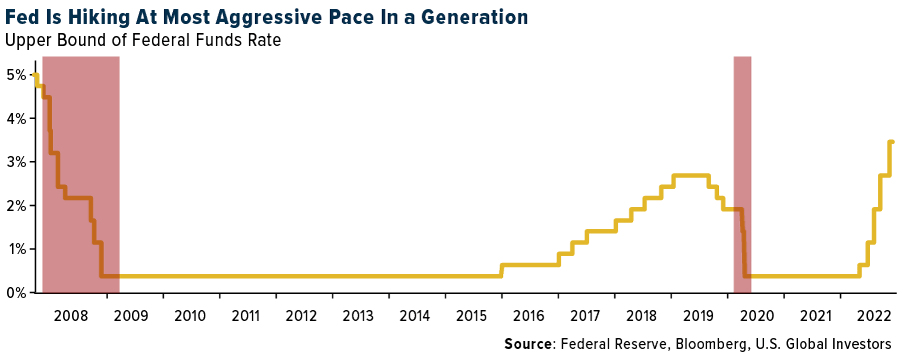

- Despite the ISM Manufacturing survey notably slowing and the JOLTS survey showing a sharp drop of more than 1 million job openings, U.S. inflation remains both elevated and concerningly broad based. Given this, it is premature to anticipate a more dovish Federal Reserve. Moreover, even as the pace of hiking will ultimately slow, a true policy pivot should only follow clear evidence that inflation has been sustainably brought back to target and that process is likely to remain a headwind for precious metals into 2023. However, many investors believe the Fed will ultimately make a policy mistake, hiking rates at the fastest pace in a generation.

- Gold extended a decline after plunging below $1,700 an ounce last week, as strong U.S. jobs data intensified concerns that the Federal Reserve will remain aggressive with rate hikes. The metal came under pressure from the stronger dollar on Monday amid weak risk sentiment in equity markets. Relentless Fed policy tightening has weighed on the asset throughout 2022, leading prices to slide 19% from gold’s year-high in March.

- Bloomberg highlighted that the largest buyers of U.S. Treasuries have all stepped back in their eagerness to buy U.S. debt. The article notes that Japanese pension and life insurers to foreign governments and U.S. commercial banks have all balked. Particularly in the face of the upped Fed offloading of $60 billion of Treasuries from its balance sheet every month. Treasuries have already recorded their steepest losses since the 1970s, but analysts worry who the next buyer will be. Zoltan Pozsar of Credit Suisse Group AG noted that since the year 2000, there has always been a big central bank on the margin buying Treasuries. Now, the private sector is basically being tasked to fulfill what the public sector has walked away from as a massive supply of Treasuries get pushed back into the system, (without a glitch?).

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission (“SEC”). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product. Certain materials in this commentary may contain dated information. The information provided was current at the time of publication. Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content. All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (09/30/22):

Fortuna Silver Mines

K92 Mining

Barrick Gold Corp.

Superior Gold Inc.

Osisko Gold Royalties

New Gold

Torex Gold Resources

Boeing

American Airlines

United Airlines

COSCO Shipping Holdings

Evergreen Marine Corp.

Delta Air Lines

LVMH Moet Hennessy

Hermes International

Alibaba Group

Siemens AG

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The S&P Global Luxury Index is comprised of 80 of the largest publicly traded companies engaged in the production or distribution of luxury goods or the provision of luxury services that meet specific investibility requirements.

Free cash flow (FCF) represents the cash a company generates after accounting for cash outflows to support operations and maintain its capital assets.

The Job Openings and Labor Turnover Survey (JOLTS) tells us how many job openings there are each month, how many workers were hired, how many quit their job, how many were laid off, and how many experienced other separations (which includes worker deaths).