Investor Alert

Oil Investments Are Expected to Make this Texas University the Nation’s Wealthiest School

Date Posted: August 26, 2022

Read time: 44 min

The University of Texas at Austin (UT), just a couple of hours up the road from our headquarters in San Antonio, may soon unseat Harvard as the wealthiest school in the U.S. How has it managed to do this? In a word: Oil.

At a time when large sovereign wealth funds are divesting from fossil fuels and ESG (environmental, social and corporate goverance) investing has gone mainstream, the UT System has been the longtime owner and manager of 2.1 million acres of mineral-rich land, scattered across West Texas, that it leases out to as many as 250 producers, including ConocoPhillips.

Thanks to higher oil prices, the mineral rights to the land generate roughly $6 million every day, according to Bloomberg.

The UT System’s decision to continue participating in oil is in keeping with Texas’s close ties to the fossil fuels industry. The state produces more oil and gas (and wind power) than any other, a fact that policymakers are eager to protect. This week, Texas moved to restrict state pension funds from investing in BlackRock, UBS Group, Credit Suisse and a number of other financial institutions that have been found to be “hostile” toward the energy sector.

But it’s more than just tradition. UT’s oil investments have been incredibly profitable and, by most accounts, will continue to be so as long as the energy crisis deepens and inflationary pressures keep prices elevated. The S&P 500 Energy Index is by far the top performing sector for the year, up nearly 50%, compared to the broader market, which is off by 12%.

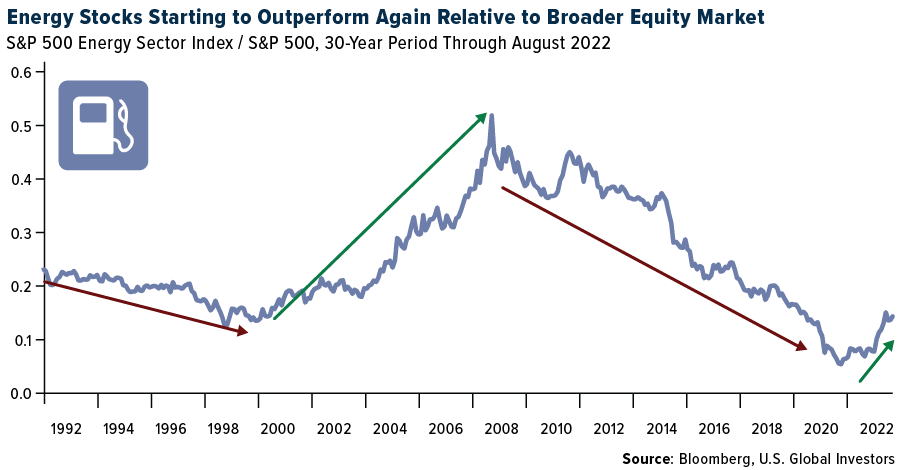

A New Cycle of Outperformance?

Looking ahead, energy stocks appear to be setting up for a new cycle of outperformance relative to the market. Take a look at the chart below, which shows the long-term ratio between the energy index and S&P 500. Technically, this may be the most attractive time to invest in energy since at least the beginning of the century.

Warren Buffett seems to agree. Last week, Berkshire Hathaway received regulatory approval to buy up to half of Houston-based Occidental Petroleum (OXY).

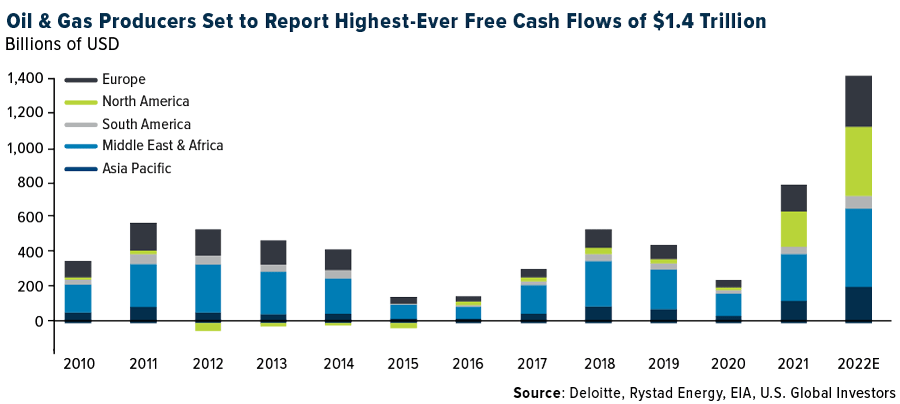

The disruptions of the past two years are believed to have triggered a readjustment in the energy market. In a just-released report, Deloitte projects that oil and gas producers could report the highest-ever free cash flow (FCF), as much as $1.4 trillion, in 2022. The industry could also become debt-free by 2024.

Although oil prices in 2022 have been equivalent to those in 2013 and 2014, cash flows are currently three times higher thanks to capital expenditure discipline after years of underinvestment, Deloitte analysts say. U.S. shale producers, which generated negative cash flows in nine out of the last 10 years, are expected to report record FCF of $600 billion.

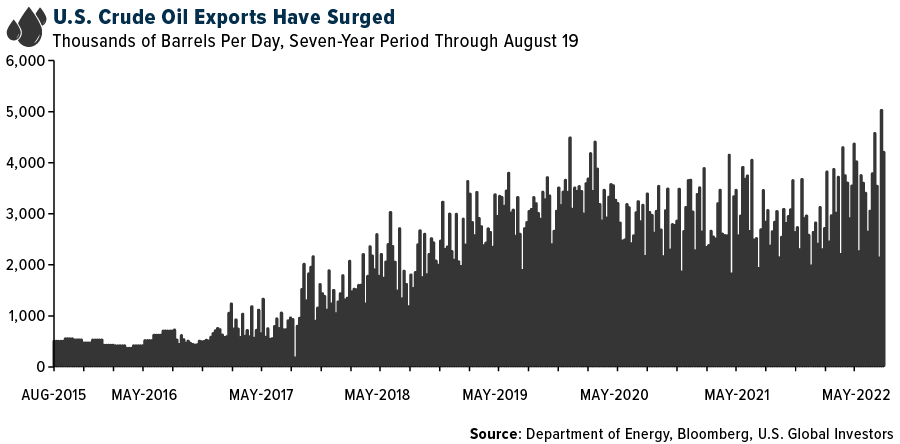

This comes as the U.S. is set to export a record amount of crude oil this year and next as the country captures market share away from Russia. Since Congress lifted the 40-year-old oil export ban in 2015, weekly exports have steadily risen above 4 million barrels a day, but earlier this month, exports exceeded 5 million barrels for the first time. According to Bloomberg, U.S. suppliers will likely be able to hold on to the increased market share since producers in other regions, including those in the North Sea and West Africa, have not been growing output as rapidly as American companies have.

California Bans Gas-Powered Vehicles by 2035. Will the Infrastructure Be Ready by Then?

The backdrop to all of this, of course, is the expansion of ESG-minded investing and global financing of alternative fuels and renewable energy sources. This week, California became the first state to approve a ban on the sale of new gas-powered vehicles by 2035 in favor of electric vehicles (EVs). This is a huge opportunity, as investment in the state’s notoriously spotty power grid will need to increase significantly.

New, more reliable EV charging stations will also need to be installed. Earlier this month, J.D. Power announced that Americans’ satisfaction in charging infrastructure is declining due to a growing number of “inadequate” and “non-functioning stations.”

“This lack of progress points to the need for improvement as EVs gain wider consumer acceptance because the shortage of public charging availability is the number one reason vehicle shoppers reject EVs,” the report reads.

Airlines and Shipping Companies Seeking Alternative Fuels

The airlines and container shipping industries are also seeking ways to achieve net-zero carbon emissions by 2050. One method being used by airlines is sustainable aviation fuel (SAF), which reportedly reduces CO2 emissions by as much as 80%. The liquid fuel is normally produced from a number of sources, including waste oil and fats, municipal waste and non-food crops.

SAF is currently much more expensive to make than traditional jet fuel, but several companies and groups are leading efforts to scale up the technology. Boeing is establishing a facility in Japan to begin researching and developing SAF, while World Energy, a Boston-based low-carbon solutions provider, is planning to convert a refinery in Houston to an SAF plant. Earlier this month, Alaska Airlines announced it had finalized an agreement to buy 185 million gallons of SAF from biofuel company Gevo over five years starting in 2026. Alaska also has announced a collaboration between Microsoft and start-up firm Twelve to advance production of E-Jet, an even more sustainable fuel that’s made from carbon dioxide.

As for shipping, wind propulsion is being touted as the “most impactful emissions reduction technology.” Today, 21 large ocean-going vessels already have wind-assist systems installed, according to the International Windship Association (IWSA), and by the end of 2023, this number could jump to nearly 50. Some of the biggest names in maritime shipping are involved in investing millions of dollars into wind propulsion technology, including Cargill, Maersk and Mitsui. The IWSA calls the 2020s the “Decade of Wind Propulsion.”

Curious to know the most important invention of the 20th century? Find out by clicking here!

Airlines and Shipping

Strengths

- The best performing airline stock for the week was Qantas, up 10.2%. According to UBS, Latin American August yields came in at 51% year-over-year (from 50% last week), September yields up 50% and October yields up 41% year-over-year. When compared to 2019, August yields increased by 3%, while September yields grew 10% and October was up 11%.

Weaknesses

- The worst performing airline stock for the week was WIZZ Air, down 9.4%. Traffic in the U.S. and China is slowing. In China, the weekly volume index fell 59% versus the 2019 level in the week, versus down 52% in the previous week. In the U.S., TSA checkpoint data has been tracking down by 10% versus 2019 levels.

- The large “excess demand” for container transportation at sea, which has lifted earnings among box carriers to record heights since November 2020, has more or less disappeared this year, according to calculations by Sea-Intelligence. With January 2020 as the starting point – when the Covid-19 pandemic still had not struck nations and the world economy with lockdowns – it is evident that global demand for container transport has consistently been 10% above the available capacity among container carriers. However, throughout the last six months, this imbalance in supply and demand has basically been leveled out. The most recent figures from June this year show that “excess demand” is now down to only 2% compared to the pre-pandemic level.

- Air New Zealand posted its third straight annual loss, but indicated the worst is over and it expects earnings to improve now that borders have reopened. The Auckland-based airline announced a loss before significant items and tax of NZ$725 million for the year ended June 30, compared with a NZ$444 million loss a year earlier. Operating revenue of NZ$2.7 billion, while up 9%, was significantly impacted by pandemic travel restrictions, and dividends remain suspended.

Opportunities

- According to Raymond James, despite the average fuel price being 9% higher in 2019 versus 2009, fuel expense as a percentage of overall revenue has declined from an average of 27% to 22% for U.S. airlines, and from 32% to 27% for non-U.S. airlines. Admittedly, this is likely in part due to fuel hedge losses in 2009; however, pricing de-commoditization and a more fuel-efficient fleet are large drivers.

- In an upbeat visit with UPS senior management, Goldman Sachs came away with a positive view on the prospects for future productivity gains, as well as ongoing mixed enhancement and a still good price environment. Net-net, the bank sees the secular UPS story as intact. While economic risk certainly creates near-term earnings per share (EPS) concerns across the transport space, Goldman did come away from the meeting with a view that UPS has levers that it can pull to mitigate reasonable volume/cost pressures regarding margin.

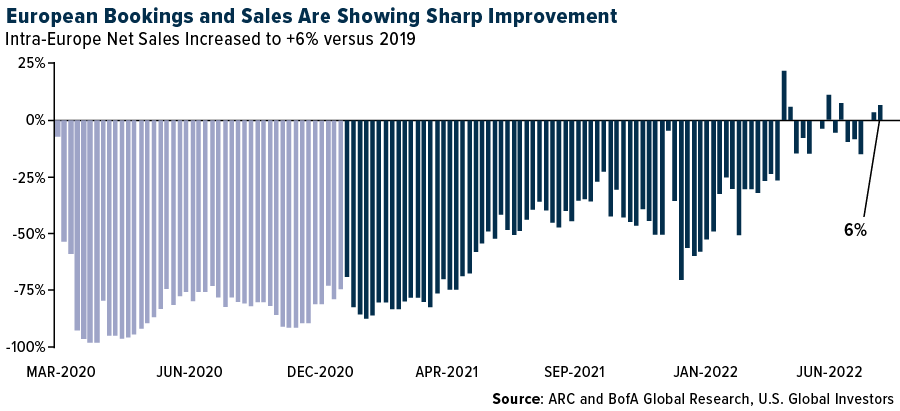

- European airline bookings as a proportion of 2019 levels showed a strong increase in the week, with higher intra-Europe and international net sales driven by a decline in the 2019 base. Total net sales were down by 2% on a week-on-week basis, with lower bookings over summer in-line with historical seasonal trends. Intra-Europe net sales increased by four points to 6% versus 2019, although fell by 2% week-on-week. International net sales were up by 13 points to -3% versus 2019, but also showed a 2% week-on-week decline. This led to an 11-point increase in system-wide net sales.

Threats

- According to Cowen, operational issues are likely to continue for at least another 12 to 18 months as airlines hire replacement workers and hold capacity to levels that enable recovery when operations go awry. The airlines overcorrected during the pandemic and are having the same issues as other industries — hiring to get back to full staffing levels.

- According to JPMorgan, the primary driver of shipping profitability in recent quarters has been tight freight markets and high freight rates. Rates seem to be in a firm downward trend. The fall in rates appears to be driven by a lack of demand, and not by an easing of congestion levels. Congestion appears to be getting worse overall, with this linked in many ways to labor disputes, both in North America and in Europe. Booking levels (and over-bookings) have slowed more sharply, producing a geared effect on freight rates.

- The decline in oil should have been a bright spot for airlines as fuel-related operating expenses should move lower, resulting in declining yields and providing some relief to budget-stretched consumers. However, the recent movement in oil has been offset by an increase in crack-spreads, further delaying the benefits that were expected from the commodity decline.

Emerging Markets

Strengths

- The best performing country in emerging Europe for the week was Turkey, gaining 4.7%. The best performing country in Asia this week was Hong Kong, gaining 1.7%.

- The Romanian leu was the best relative performing currency in emerging Europe this week, losing 0.2%. The Malaysian ringgit was the best performing currency in Asia this week, gaining 0.1%.

- Chinese e-commerce stocks recorded stronger gains this week supported by the latest stimulus projects announced by the government. JD.com was the best performing stock among members of the iShares China ETF

Weaknesses

- The worst performing country in Asia this week was the Philippines, losing 1.6%.

- The Pakistani rupee won was the worst performing currency in Asia this week, losing 2.6%.

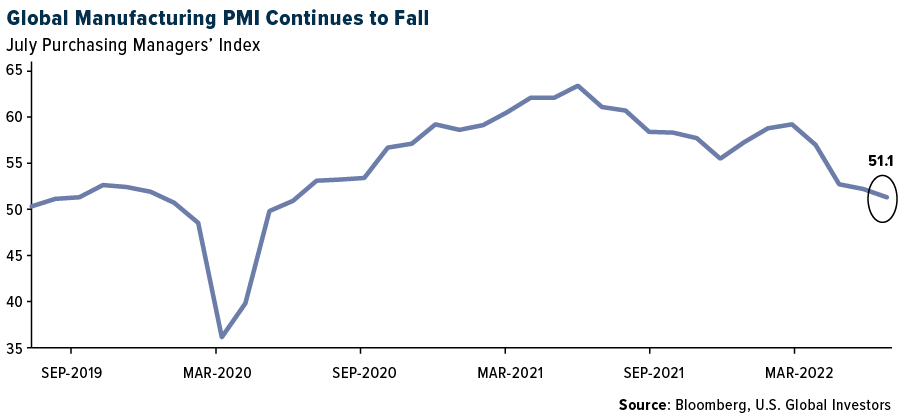

- Eurozone Manufacturing PMI was reported at 49.7, below the 50 mark that separates growth from contraction, but above the expected 49.0. Service PMI declined to 50.2 from 51.2 in July, slightly below the expected reading of 50.5. The Composite PMI, which combines manufacturing and service activities, was released at 49.2.

Opportunities

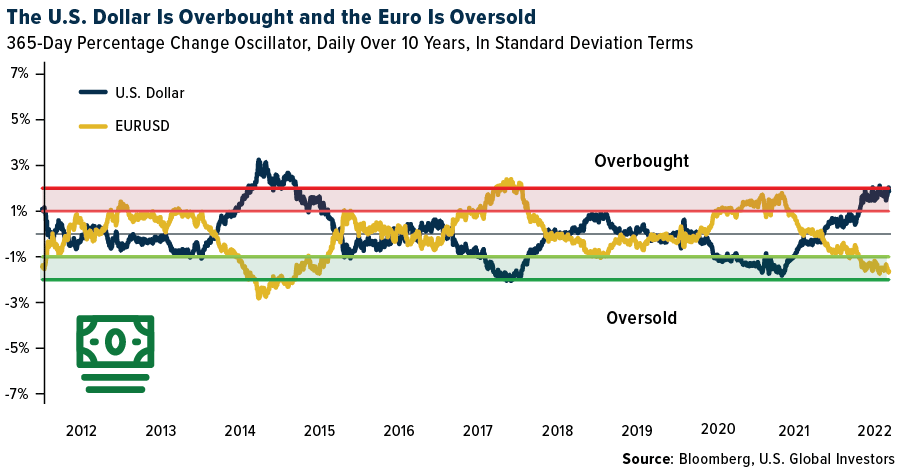

- According to our 10-year oscillators, based on a 365-day percentage change, the U.S. dollar is in overbought territory while the euro is oversold. Some economists may argue that the worsening economic situation in Europe due to slower growth, high inflation, and a shortage of energy, may further push the Eurozone currency lower, but our technical analysis of is pointing to an upcoming reversal.

- Bloomberg economists expect China’s Manufacturing PMI to increase to 49.4, remaining below the 50 mark, but improving from the prior month’s reading of 49.0. The Caixin PMI should remain above 50. Most Bloomberg economists expect the Caixin Manufacturing PMI to be released at 50.2.

- China has reported another round of policy support. State Council announced 19 new measures to help stabilize the economy. More than 300 billion yuan was added to financial instruments for specific projects; 500 billion yuan was added to local governments’ special bonds quotas to be issued by October, and 200 billion yuan were set aside to support electricity producers, FactSet reported.

Threats

- Last weekend, on the west side of Moscow, a car exploded killing the daughter of Alexander Dugin. He is an ultra-nationalist Russian ideologue with ties to Russian President Vladimir Putin. Some call him “Putin’s Brain” and claim that he is the one behind planning the attack on Ukraine.

- Natural gas prices in Europe keep rising. Russia announced that the Nord Stream 1 pipeline which transports gas from Russia to Europe, will shut down its operations for three days starting August 31 due to maintenance. Some companies in Europe struggle to keep their operations with record high gas prices. This week, Azoty, a Polish chemical company producing fertilizer, announced production cuts due to record high energy costs. There is also a possibility that the NS1 pipeline may not reopen after its scheduled maintenance is complete.

- Drought and a heat wave across China are causing an electricity shortage as record low water levels interrupt electricity generation at many hydropower plants. This week, Shanghai implemented power usage curbs for two days from Monday.

Energy and Natural Resources

Strengths

- The best performing commodity for the week was uranium, up 13.22%, as proxied by the Sprott Physical Uranium Trust, on news that Japan is eyeing a dramatic shift back to nuclear power after more than a decade since the Fukushima meltdown. Prime Minister Fumio Kishida noted that nuclear power and renewables are essential to a green economy. In other news, Germany’s natural gas storage facilities surpassed a fill level of more than 75% this month, reports CNBC, two weeks ahead of schedule, as Europe’s largest economy scrambles to prepare for the coming winter. The latest data compiled by industry group Gas Infrastructure Europe shows Germany’s gas storage facilities at slightly over 77% full. Chancellor Olaf Scholz’s government initially planned for gas storage levels to reach 75% by September 1, the article explains. The next federally mandated targets are 85% by October 1 and 95% by November 1.

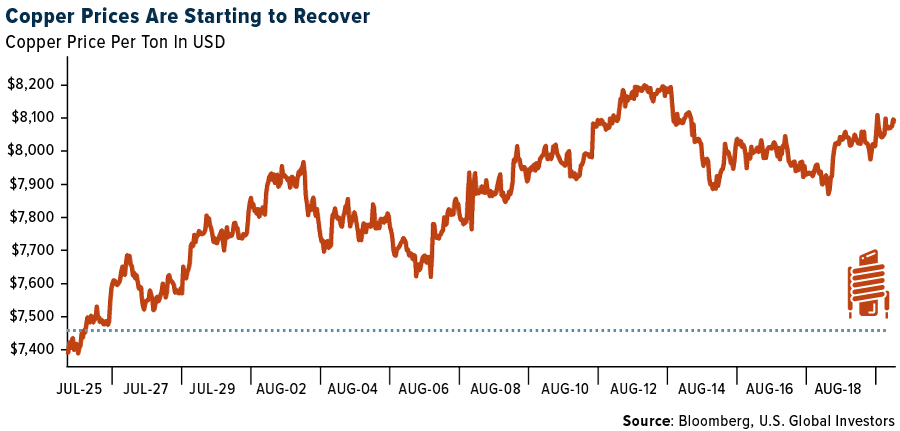

- The world’s largest copper market is tightening as a summer power crunch in parts of China disrupts production at a time of already-low inventories. Both the premium on imported cargoes over the LME spot rate, and the spread between local spot and futures prices, expanded last week to the widest levels since the final quarter of 2021, according to researcher Shanghai Metals Market.

- Coal prices remain elevated, met coal being up 11% this week and higher by 23% this month. Thermal coal is up 3% this week and up 2% this month, as this is a seasonally strong demand period for the commodity (monsoons ending in India and maintenance periods running over in China). Industry expectations are building that China may relax its import ban on Australian coal after no import volumes from Atlantic HV coal in the past few months, indicating some buyers think they’ll be able to buy Australian coal soon. Heatwaves in China, coupled with decreasing inventory levels, placed upward pressure on prices last week.

Weaknesses

- The worst performing commodity for the week was lead, down 3.22%, on recent easing of power rationing which is expected to increase supply. Despite a steady flow of supply closure headlines in zinc and aluminum, the prices of both metals are down on the week. Zinc prices initially jumped more than 6% intraday on Tuesday up to $3,800 per ton but nearly erased all these gains before the market closed for the day and have now sunk back toward $3,500 per ton. To some degree, this can potentially be explained by buy-the-rumor, sell-the-fact profit taking after zinc prices were likely already pricing in the risk of this supply headline – zinc was up nearly 30% off its July low at the end of last week versus 14% in copper and 8% in aluminum.

- The Indian government has increased taxes of fuel exports to INR 2/liter from zero on jet fuel and by INR 2/liter to INR 7 on diesel. The government also slashed a windfall tax on locally produced crude oil, Reuters reported, citing government notifications. Tax on domestically produced crude oil was cut to INR 13k per ton from INR 17.8k per ton.

- U.S. permitting activity decreased substantially in July with 1,145 approved permits compared to 1,415 permits in June. On a month-over-month basis (July versus June), the total approved permit count for horizontal wells decreased 270 permits to 1,145 permits. Private operators received 558 approved permits compared to 587 approved permits for public operators in July, which compares to private operators with 529 permits and public operators with 661 permits in June.

Opportunities

- Deloitte LLP noted this week that U.S. shale producers are on course to make nearly $200 billion this year, perhaps enough to make the industry debt-free by 2024. The report also highlights that this cycle is being met with much more capital discipline. Global spending is about 60% less than spending in 2014. This bodes well for paying down debt, raising dividends, and stock buybacks in the future.

- Ford announced the cutting of 3,000 jobs in a move to shift $50 billion in spending toward developing its electric vehicle (EV) production capacity. Last year Ford produced 64,000 EVs but plans to tool up to having an annual capacity of 2 million EVs by the end of 2026. With tax incentives authorized to produce EVs from domestic sources, and certain trade partners by the recent climate legislation, investors should find domestic natural resource investments favored over imports. Panasonic, which already jointly operates a battery factory with Tesla in Nevada, announced it is planning on building an additional $4 billion battery plant in the U.S., perhaps Oklahoma.

- Natural gas futures in the U.S. jumped to a new 14-year high as European prices surged on Russia’s move to shut a major pipeline, stoking speculation that demand for American exports of the heating and power-plant fuel will soar. U.S. gas climbed as much as 6.9% to $9.982 per million British thermal units on the New York Mercantile Exchange. In Europe, benchmark gas futures rose as much as 20%, driving electricity prices to fresh records. It is likely that natural gas demand will remain strong despite the pull back in crude oil prices.

Threats

- Nickel was in the spotlight this week as Indonesian president Joko Widodo proposed a tax on exports of the metal. Indonesia currently produces 30% of the world’s nickel, but much of it is in the form of Nickel Pig Iron and ferronickel, which are exported abroad for smelting and refining. It is hoped that export taxes on NPI and ferronickel could help move Indonesia up this value chain. Nickel, which is primarily used in stainless steel production, is rapidly expanding its end use, as each new electric vehicle requires about 50kg of the metal. Despite this announcement, nickel dropped 5.9% on the week as inventories of NPI at ports in China remain high amid weakening demand from Chinese steel mills.

- According to JPMorgan, steel prices in the U.S. have continued to fall from their peak with HRC prices now around $771 per ton versus $1,780 per ton at the end of September. The bank thinks prices will continue to move slightly lower over the next several months.

- Carbon prices have sharply increased, rising to an all-time high because of increased cooling demand in Europe. S&P reported that lower auction volumes in August and September are contributing to this rise. The sharp increase in prices is likely to accelerate the idling of marginal steel mills (or at least those will little-to-no hedges in place) as margins continue to be under pressure.

Luxury Goods

Strengths

- U.S. consumer sentiment improved further in August and households’ near-term inflation expectations fell to an eight-month low, supported by declining gasoline prices. The final reading of the University of Michigan Sentiment Index rose to 58.2 from a preliminary reading of 55.1, and above the expected 55.5.

- Inflation expectations fell to an eight-month low of 4.8% from 5.2% in July, while the survey’s five-year inflation outlook was unchanged at 2.9%, holding within the range that has prevailed for the past year.

- Farfetch, an online marketplace, was the best performing S&P Global Luxury stock this week, gaining 47.43%. Shares surged after the Cartier owner said it would sell a 47.5% stake in YNAP to online marketplace Farfetch Ltd. and a further 3.2% to investor Mohamed Alabbar, a developer of the massive Dubai Mall.

Weaknesses

- Preliminary S&P Global Manufacturing PMI for August declined to 51.3 from 52.2 in July. The Service PMI noted an even sharper drop to 44.1 from 47.3 the month prior. The final August PMIs will be announced next week, September 1.

- New home sales in the United States sharply declined to 511,000 from 590,000, and below the expected reading of 575,000. Weaker housing data points to a deteriorating situation in the property sector. Mortgage rates are moving higher, and inflation is at a level last seen in 1982.

- Nordstrom was the worst performing S&P Global Luxury stock this week, losing 25.39%. Shares sold off after company slashed its projections for revenue growth, saying it would have to sharply reduce prices to sell overfilled inventories.

Opportunities

- China cut one- and five-year prime loan rates this week and announced additional measures to help stabilize its economy. Equites surged on Thursday after the announcement was made. The biggest gainers were noted among internet/technology stocks and retailers, as the latest measures should support spending. China is one of the largest global consumers of luxury goods services and products.

- More luxury firms continue adopting cryptocurrency as a form of payment. Soneva, a resort chain, will now accept Bitcoin and Ethereum as means of payment at its high-end resorts of Fushi, Jani and Aqua in the Maldives, as well Kiri in Thailand. Cryptocurrency payments are becoming popular among travelers across the world. Italian sports car maker Lamborghini has already pre-sold the entire production run to early 2024, suggesting that global economic uncertainties are not impacting luxury goods.

- Lamborghini in early August reported the best first half in history, with record sales and profits. Ferrari also posted record results in the second quarter and raised its annual forecast, Bloomberg reports.

Threats

- Russian diamond producer Alrosa accounts for about a third of global diamond supply. For a while, Alrosa was not selling diamonds as new sanctions were imposed on Russia for its invasion of Ukraine. However, now the company is back to selling more than $250 million of diamonds a month, only about $50 – $100 million a month below pre-war levels, Bloomberg reports. India is the largest buyer of Russian diamonds. Any problems with payments due to sanctions may once again push diamond prices higher.

- Bank of America downgraded Lennar, KB Homes, and Toll Brothers due to weaker home demand. Toll Brothers hit its lowest level since June this week after announcing a significant miss in quarterly orders, suggesting that the high end of the market is under pressure amid a broader housing slowdown.

- Bloomberg economists are expecting weaker jobs data coming out next week in the United States. The group expects initial jobless claims to increase to 250,000 from 243,000 the prior week. JOLTS job openings are expected to decline to 10,400,000 in July from 10,698,000 in June.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performer for the week was EOS, rising 23.01%.

- The main clearinghouse for the U.S. stock market has switched on a settlement system built on blockchain, calling it a “milestone achievement” for adopting digital technologies in markets. Depository Trust & Clearing Corp. said on Monday that its “Project Ion” platform is now processing around 100,000 bilateral equity transactions a day in parallel with its existing settlement system, writes Bloomberg.

- Dallas Cowboys quarterback Dak Prescott has signed a multiyear endorsement deal with cryptocurrency firm Blockchain.com as the crypto industry boosts its presence in sports to lure more users. CEO Peter Smith said pro football is going to be crucial for the crypto industry as platforms battle for users, Bloomberg explains.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week was FLOW, down 15.10%.

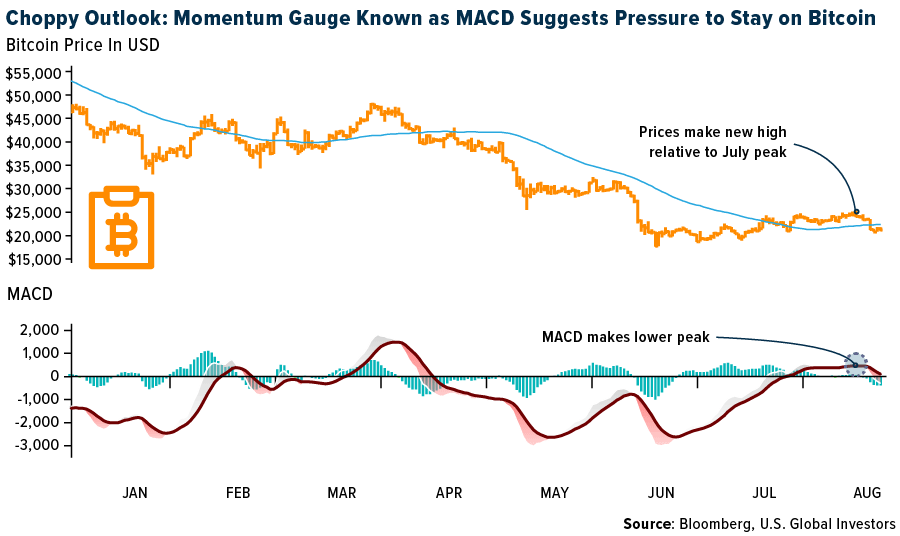

- Bitcoin nursed a four-day drop of about 10%, held back by a bout of risk aversion in global markets on jitters over tightening Federal Reserve monetary policy. Bitcoin fell 2.7% on Monday as the global equity market rebound starts to crack in part because of the Fed’s commitment to raise rates and drain liquidity, writes Bloomberg.

- Cryptocurrencies mirrored global markets and declines after Jerome Powell warned against prematurely loosening policy with Bitcoin settling into the lower end of the narrow range that it has traded in the past two weeks. As reported by Bloomberg, Bitcoin slumped as much as 4.9%, putting it on pace for a second consecutive weekly loss.

Opportunities

- Hacks and bankruptcies continue to roil the digital-asset industry. But these setbacks have become a boon for makers of hardware wallets who have seen their sales spike as customers rush to protect their crypto assets, writes Bloomberg. French startup Ledger saw its day-over-day sales balloon 400% in the 24 hours after a $5.2 million hack involving digital wallets based on the Solana blockchain earlier this month.

- Former SEC Chairman Jay Clayton has joined venture firm Electric Capital as an advisor, part of a growing wave of ex-regulators flocking to the crypto space as the industry faces increasing scrutiny. Kevin Warsh, a former member of the Federal Reserve Board of Governors was also named as an advisor, writes Bloomberg.

- Cryptocurrency miners are accelerating their push to expand in Texas far beyond what authorities had initially expected, reports Bloomberg, threatening to send the state’s electricity use skyrocketing. Enough miners have applied to connect to Texas’ power grid to use up to 33 gigawatts of electricity. The surging interest underscores how appealing Texas remains to crypto miners, even as the value of Bitcoin has plunged more than 50% in the past year, the article continues.

Threats

- A former money manager for Celsius Network deceived the company about his investing abilities and lost or robbed tens of millions of dollars in assets, the bankrupt crypto lender alleged in a lawsuit Tuesday. Celsius alleges Keyfi Inc founder Jason Stone lied about his investing prowess and was incompetent in managing Celsius assets, writes Bloomberg. The crypto lender also accused Stone of outright theft.

- Tornado Cash, a cryptocurrency mixer that was recently slapped with U.S. sanctions, was the preferred tool for laundering illicit proceeds from NFT scams prior to the ban, according to blockchain analytics firm Elliptic Enterprises. Services offered by platforms like Tornado Cash can be used to mask transactions by mixing tokens from different sources before transferring them to the ultimate recipients, according to Bloomberg.

- Afghanistan’s central bank imposed a nationwide ban on cryptocurrencies this month and the Taliban regime has arrested several dealers who defied orders to stop trading digital tokes, according to a senior police official. The crackdown comes after some Afghans turned to cryptocurrencies to preserve their wealth and keep it out of the Taliban’s reach, writes Bloomberg.

Gold Market

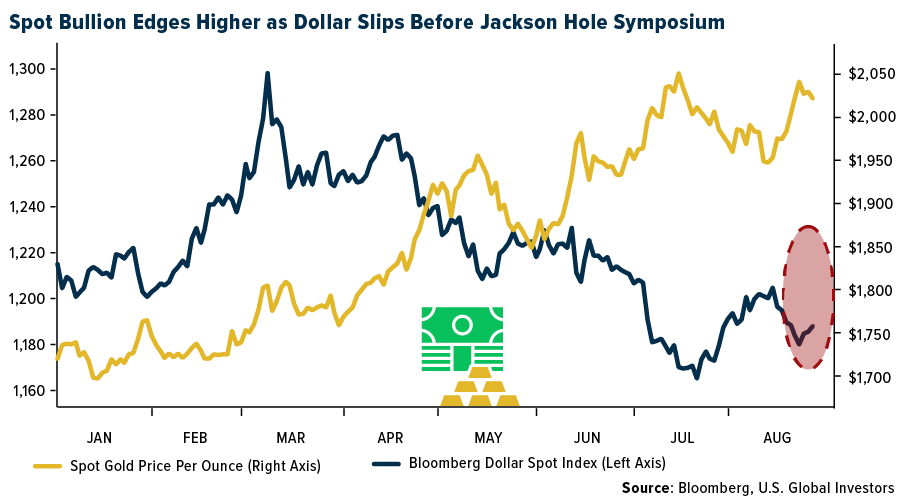

This week gold futures closed at $1,749.90, down $13.00 per ounce, or 0.74%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 1.46%. The S&P/TSX Venture Index came in off 0.61%. The U.S. Trade-Weighted Dollar rose 0.59%.

| Date | Event | Survey | Actual– | Prior |

|---|---|---|---|---|

| Aug-23 | New Home Sales | 575K | 511k | 585K |

| Aug-24 | Durable Goods Orders | 0.8% | 0.0% | 2.3% |

| Aug-25 | Hong Kong Exports YoY | -4.8 | -8.9% | -6.4% |

| Aug-25 | Initial Jobless Claims | 252k | 243k | 245k |

| Aug-25 | GDP Annualized QoQ | -0.7% | -0.6% | -0.9% |

| Aug-30 | Germany CPI YoY | 7.8% | — | 7.5% |

| Aug-30 | Conf. Board Consumer Confidence | 97.5 | — | 95.7 |

| Aug-31 | Eurozone CPI Core YoY | 4.0% | — | 4.0% |

| Aug-31 | ADP Employment Change | 319K | — | 128k |

| Aug-31 | Caixin China PMI Mfg | 50.1 | — | 50.4 |

| Sep-1 | Initial Jobless Claims | 250k | — | 243k |

| Sep-1 | ISM Manufacturing | 52.1 | — | 52.8 |

| Sep-2 | Change in Nonfarm Payrolls | 300k | — | 528k |

| Sep-2 | Durable Goods Orders | — | — | 0.0% |

Strengths

- The best performing precious metal for the week was gold, but still down 0.74%. Gold steadied after a six-day run of losses as financial markets remained on edge ahead of a pivotal annual gathering of central bankers at Jackson Hole. Bullion rose as much as 0.4% as manufacturing surveys showed France unexpectedly joining Germany in recording a decline in factory activity. A recession in the 19-member Eurozone is now more likely than not as energy costs spike following Russia’s invasion of Ukraine, according to analysts surveyed by Bloomberg. Friday’s more hawkish tone from the Fed’s Jackson Hole meeting took the edge off of a relatively good week in gold.

- Exchange-traded funds (ETFs) added 69,512 troy ounces of gold to their holdings in the last trading session, bringing this year’s net purchases to 2.59 million ounces, according to Bloomberg. The purchases were equivalent to $121.4 million at the previous spot price. Total gold held by ETFs rose 2.6% this year to 100.4 million ounces.

- According to Canaccord Genuity, with a large valuation gap between the larger and smaller royalty companies (1.8x NAV average for the senior royalty companies versus 1.0x for the intermediate/juniors), the group expects more consolidation to come. The benefit here would be better diversification, scale, and lower cost of capital.

Weaknesses

- The worst performing precious metal for the week was platinum, down 3.90%, as bears put on more shorts for the week. Wheaton Precious Metals announced that it has agreed to terminate its silver stream on Glencore’s Yauliyacu mine in Peru. As compensation, Wheaton will receive an upfront cash payment of $150 million less net proceeds already received from the stream year-to-date in 2022. Management notes that the stream termination is consistent with its core principle of working with its partners, and that the company looks forward to maintaining a strong partnership with Glencore.

- Sibanye Stillwater had a weak quarter, with a 6% EBITDA/EPS miss and negative developments in its ongoing South African labor negotiation. However, the company did maintain guidance.

- Shares of Ramelius Resources slid over 7% this week after the company revealed a hit of up to $84.7 million on its full-year results to be released in one week. The gold miner announced that it would recognize an impairment in the value of its Edna May operation worth $90 million – $95 million. The impairment is being explained due to high input costs being experienced throughout the industry.

Opportunities

- One of the world’s largest platinum group metal refineries Heraeus Metals Germany GmbH & Co said output at one of its refineries will be constrained due to a supplier of a crucial chemical to the extraction process declaring force majeure. Palladium prices jumped over 5% on the news. Heraeus noted this is a short-term issue for one of its refineries in Germany, but delays could be drawn out until November 30. It is not known to what extent the chemical reagent may be restrained or whether other refineries could be impacted.

- First Majestic Silver climbed as much as 6.3%, for its biggest intraday gain since August 4, after a drilling project in Nevada returned high grades of gold. The exploration results “validate our thesis” that areas between the company’s SSX and Smith mines are favorable “for new, near-mine gold discoveries,” president and CEO Keith Neumeyer said in a press release.

- According to Raymond James, production levels generally increased in the second quarter after a weak first quarter. Gold production grew by an average of 4% and copper production by 19% quarter-over-quarter for producers under coverage. Despite higher production levels, costs remained elevated as input pricing continued to rise through the early part of the second quarter. Gold and copper cash costs increased by an average of 12% sequentially in the second quarter.

Threats

- An airstrip in a remote jungle, built by the Brazilian government to provide healthcare to the Indigenous people in the region, has been taken over by illegal miners. The miners seized the opportunity to fly in small planes with mining supplies into a region with no roads. Now that they have established their operations, they watch over the airport, controlling all traffic in and out of the landing site. If a plane approaches that they do not recognize, the miners spread fuel canisters across the runway, making it impossible for the government to land. The success of the operation has led to the illegal miners building four more nearby airstrips on the protected land of the Yanomami people, reports the New York Times.

- Russian miners are leading the push into yuan-bond issuance on the local market as international sanctions deepen the nation’s economic ties with China. Polyus PJSC, Russia’s biggest gold miner, will collect offers for 3.5 billion yuan ($511 million) of five-year bonds, at a yield of 4.2% or lower, according to people familiar with the matter who asked not to be identified because the details aren’t public.

- The panic that gripped the diamond world this year is starting to unwind as sanctioned Russian mining giant Alrosa PJSC has quietly revived exports to near pre-war levels, writes Bloomberg. Alrosa accounts for about a third of global rough-diamond supply, and the $80 billion industry was thrown into turmoil as cutters, polishers and traders hunted for ways to keep buying from Russia while their banks couldn’t or wouldn’t finance payments. The sudden shortage of stones sent diamond prices surging, the article explains, especially for the smaller and cheaper gems that Alrosa specializes in. Now, after months of paralysis when it was hit with U.S. sanctions, Alrosa is back selling more than $250 million of diamonds a month, with sales currently only about $50 to $100 million a month below pre-war levels, according to people familiar with the matter.

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission (“SEC”). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product. Certain materials in this commentary may contain dated information. The information provided was current at the time of publication. Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content. All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (06/30/22):

Boeing Co/The

American Airlines

United Parcel Service (UPS)

Wheaton Precious Metals

Ferrari

Toll Brothers

Cartier

Tesla

ConocoPhillips

Occidental Petroleum Corp.

Alaska Air Group Inc.

AP Moller-Maersk A/S

Mitsui OSK Lines Ltd.

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The U.S. dollar index (USDX) is a measure of the value of the U.S. dollar relative to a basket of foreign currencies.

The Job Openings and Labor Turnover Survey (JOLTS) program produces data on job openings, hires, and separations.

The Michigan Consumer Sentiment Index (MCSI) is a monthly survey of consumer confidence levels in the United States conducted by the University of Michigan.

The S&P 500 Energy Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period.