Investor Alert

New 100% Tariffs on Chinese EVs: Biden’s Strategy to Boost American Manufacturing

Date Posted: May 17, 2024

Read time: 38 min

On Tuesday, the Biden administration announced significant tariff increases on China, targeting roughly $18 billion in strategic industries, with a sharp focus on electric vehicles (EVs). These tariffs, which quadruple to 100% on Chinese-made EVs, are designed to counter China’s unfair trade practices and overcapacity while boosting U.S. industries. The move also aims to strengthen President Biden’s position heading into the November presidential election.

For decades, China has strategically moved to dominate various industries, from toys and clothing in the 1980s to semiconductors and renewable energy today. As of now, China produces a third of the world’s manufactured goods, surpassing the combined output of the U.S., Germany, Japan, South Korea and the U.K. This industrial might has given China a trade surplus in manufactured goods equal to a 10th of its entire economy.

The world’s second largest economy was a minor player in car exports just four years ago, shipping about 1 million low-priced vehicles annually to less affluent markets. Today, China has surged past Japan and Germany to become the world’s biggest car exporter, with shipments running at an annual pace of nearly 6 million vehicles. China’s car exports, in fact, hit a record high in April, with a year-on-year increase of 38%.

The $11,000 EV Challenging Tesla

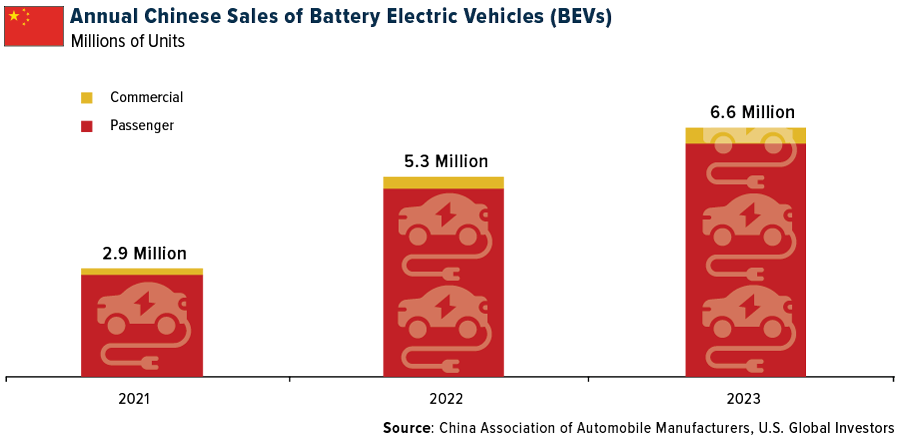

As for EVs in particular, domestic sales have been strong and are growing. Last year, Chinese consumers purchased some 6.6 million EVs, according to the China Association of Automobile Manufacturers (CAAM).

Demand doesn’t appear to be slowing down. China’s introduction of 71 models of electric cars this year, many of them equipped with advanced features and priced lower than comparable models in the West, poses a direct threat to American automakers. The model that has a lot of U.S. companies worried is the Seagull, a small EV manufactured by BYD (“Build Your Dreams”), which sells for around $11,000. Some people are already calling BYD a “Tesla killer.”

Protecting U.S. Industries in an Election Year

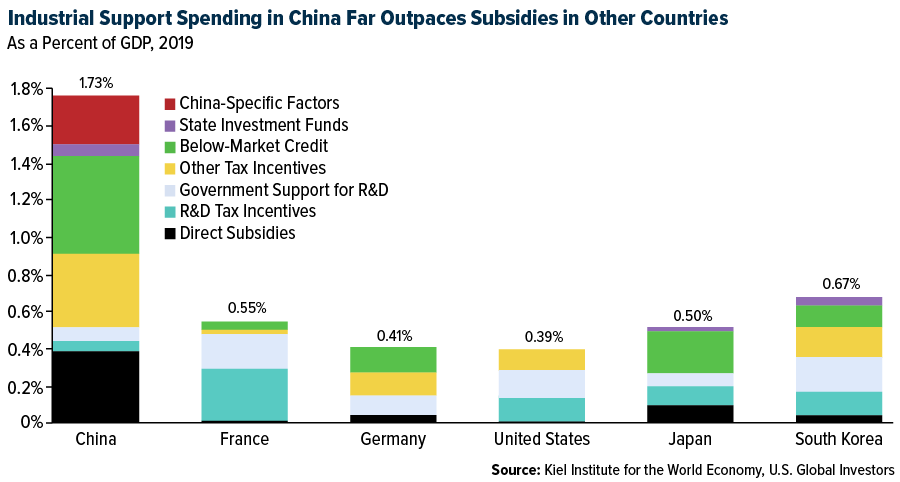

Historically, China has benefited from substantial subsidies, a key gripe from American and European business leaders and politicians. Chinese subsidies relative to GDP are about three times higher than in France and about four times higher than in Germany or the U.S., according to a report by the Germany-based Kiel Institute for the World Economy. This disparity underscores the aggressive tactics employed by China to gain a competitive edge.

President Biden’s tariffs are not just about countering China’s dominance; they are also about protecting American industries. Through the Chips and Science Act and the Inflation Reduction Act, Biden has already provided significant support to American companies in sectors like semiconductors and renewable energy. The tariff increases on China are an extension of that protection, ensuring that American businesses can compete on a more level playing field.

It’s crucial to view Biden’s actions through the lens of the upcoming U.S. presidential election. President Biden is trailing former President Donald Trump in national polls, including in swing states, and this move is likely aimed at rallying support among voters who are concerned about job losses and industrial decline due to unfair trade practices.

Potential Setbacks

While the tariffs are aimed at protecting U.S. industries, they could have unintended consequences on the nation’s efforts to decarbonize its grid, warns the Atlantic Council, a Washington, D.C.-based think tank. China is the largest exporter of lithium-ion batteries to the U.S., which are crucial for grid storage that complements solar power. Depending on the details of the tariffs, U.S. efforts to transition to renewable energy could face slowdowns.

Another critical factor to consider is the declining consumer demand for EVs in the U.S. According to the J.D. Power 2024 U.S. Electric Vehicle Consideration (EVC) Study, the percentage of new vehicle buyers considering an EV has dropped for the first time since 2021. Key barriers include a shortage of affordable models, concerns about charging infrastructure and limited consumer understanding of EV incentives. Economic factors like lower fuel prices and high inflation further dampen demand.

Remarkably, Biden’s tariffs aren’t the worst-case scenario for China. Former President Trump has said he would impose 60% tariffs on all imports from China if reelected, which Bloomberg Economics estimates would effectively eliminate all trade between the two nations.

New Energy Metals on the Rise

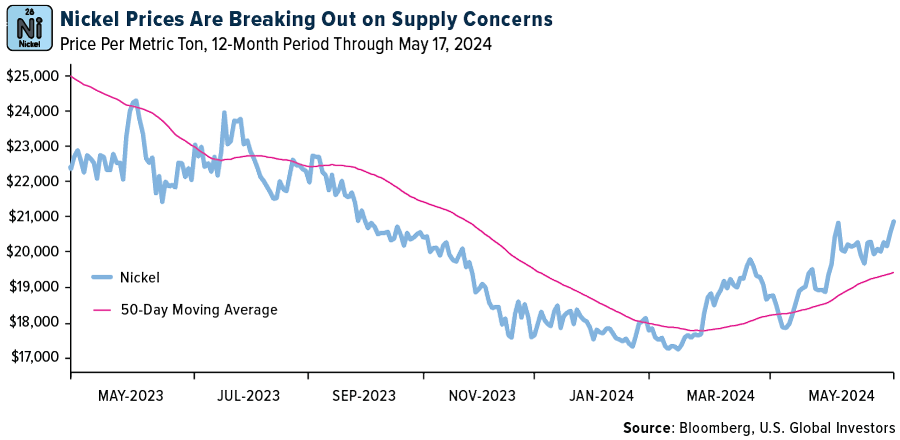

With EVs gaining in popularity across the globe and governments spending to build out wind and solar facilities, we’re seeing prices for key metals and materials start to break out. Copper futures have recently hit a record high, while nickel prices are breaking out on near-term supply concerns. Unrest in New Caledonia, a French territory in the South Pacific and the world’s number three nickel producer, has disrupted output of the white metal, which is used in the production of batteries. Nickel traded above $21,000 per metric ton yesterday for the first time in about a month.

Government Policy Is a Precursor to Change

Biden’s sweeping tariff increases on China are a calculated move to protect American industries, counter unfair trade practices and gain political clout ahead of the November election. While these measures are necessary to level the playing field, they come with challenges and potential unintended consequences. As investors, it’s crucial to stay informed and understand the broader implications of these policies on the market and the economy.

Watch our latest video on gold’s Fear Trade by clicking here!

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 1.24%. The S&P 500 Stock Index rose 1.48%, while the Nasdaq Composite climbed 2.10%. The Russell 2000 small capitalization index gained 1.64% this week.

- The Hang Seng Composite fell 0.69% this week; while Taiwan was up 2.65% and the KOSPI fell 0.11%.

- The 10-year Treasury bond yield fell 7 basis point to 4.42%.

Airlines and Shipping

Strengths

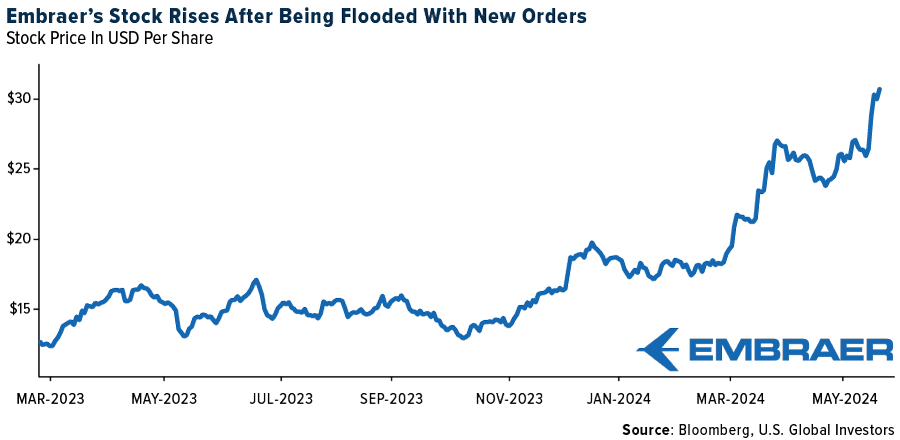

- The best performing airline stock for the week was Embraer, up 19.4%. Copa Holdings delivered earnings upside and strong margins (24% operating margin) despite a significant headwind from the MAX-9 grounding in January. During the first quarter of 2024, Copa earned $4.19 per share (up 5% year-over-year), well ahead of ISI’s $3.32 due to better non-fuel unit cost and slight unit revenue outperformance.

- According to Morgan Stanley, container volumes continue to show improvement with volumes up 11% year-over-year; a seventh consecutive month in positive territory. Asia – North America also continued to show strong volume improvement, moving from positive 6% year-over-year in August to over 20% positive in the last six months as data continues to lap easier comps.

- According to Simple Flying, United Airlines is anticipating a 5% year-over-year increase in travel over the Memorial Day holiday, making it the busiest Memorial Day weekend in the company’s history

Weaknesses

- The worst performing airline stock for the week was Wizz, down 7.4%. U.S. ULCCs are seeing off-peak pressure, with disappointing second quarter revenue guides citing very weak off-peak trends. Three also lowered fourth quarter 2024 capacity guidance for various reasons, according to Raymond James.

- Two major shipping routes, Asia to Europe and the Pacific route, saw a large increase in canceled sailings in March and April, according to a new analysis from Sea-Intelligence. The route worst affected by blank sailings was Asia-North Europe, which lost 21% of its planned capacity in April.

- According to Aero Analysis Partners, Boeing delivered only three MAXs as of May 9, reflecting a slowdown compared to the nine made on the same date last year, but matching delivery figures from the same period last month.

Opportunities

- Embraer hit its highest level since 2015. In JPMorgan’s view, this strong outperformance came on the back of an article published by Economic Times stating that InterGlobe Aviation – an Indian airline also known as IndiGo – is in talks with Embraer, Airbus and ATR for the acquisition of “at least 100 smaller jets.”

- The latest Global Port Tracker (GPT) from the National Retail Federation (NRF) continues to point to healthy import volumes. The GPT now expects May imports to come in at 2.06MM TEUs, up 6.8% year-over-year. For June, imports are expected to hit 2.03MM TEUs, up 10.7% year-over-year and versus last month’s projection of up 8.9% year-over-year.

- Frontier recently reactivated its codeshare with Volaris which will connect over 40 cities in Mexico and nearly 30 cities in the U.S., and Central and South America. This codeshare agreement was originally announced in January 2018 in order to offer more affordable fares between the U.S. and Mexico, but in 2021 the codeshare was suspended as the Federal Aviation Administration (FAA) downgraded Mexico’s safety status to Category 2 from Category 1, according to Morgan Stanley.

Threats

- JetBlue lowered September and October capacity by 750 basis points (bps) and 580bps, respectively. In September, Latin American flying saw greater reductions at 930bps, compared to domestic reductions at 740bps. While all regions saw meaningful reductions in October, Atlantic flying saw the greatest reduction at -13.5%, reports Bank of America.

- Bank of America cut its 2024-2026 estimates after Evergreen’s first quarter 2024 results missed consensus on higher unit costs. The bank acknowledges Evergreen profitability should sequentially improve in the second and third quarters on seasonally stronger volumes, normalization of unit costs, and freight rates staying higher-for-longer. Bank of America believes there is downside likely beyond the near-term spot surge on normalization seasonality, new vessel deliveries, and an eventual resumption of Red Sea sailings.

- The Justice Department alleges that Boeing has violated the Deferred Prosecution Agreement (DPA) it reached with the company in 2021 over the 2018-2019 737 MAX crashes. The DOJ says Boeing has failed to take steps to prevent violation of anti-fraud laws; Boeing indicated that it believes it has honored the agreement, according to JPMorgan.

Luxury Goods and International Markets

Strengths

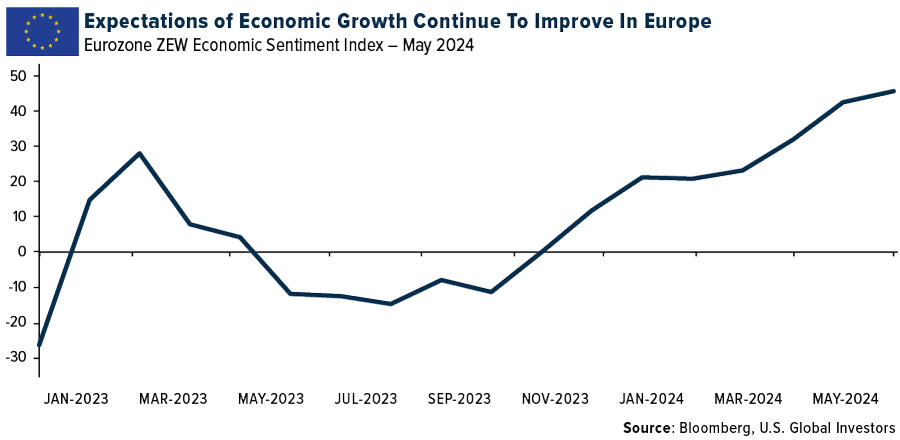

- The Eurozone ZEW Economic Sentiment Index was reported at 47 in May, compared to 43.9 in April and versus the market expectation of 46.1. Expectations of stronger economic growth in Europe are reflected particularly in the sharp rise in expectations for domestic consumption, followed by the construction and machinery sectors, the ZEW Institute said in its press release.

- Shares of Watches of Switzerland surged on Thursday, rising 19% in London, the biggest intraday move since November. The top seller of Rolex watches in the UK saw U.S. sales jump 14% in its fiscal fourth quarter, Bloomberg reports. This helped total sales rise 3% (more than analysts expected) to £380 million ($482 million) in the period ended April 28.

- Faraday Future Intelligent, the maker of the luxury FF 91 EVs, was the best performing S&P Global Luxury stock, gaining 2,210% in the past five days. The company’s shares were in danger of being delisted after losing 99% of their value in a year. On Friday, shares closed at $1.10 compared to just $0.05 cents a week ago.

Weaknesses

- Burberry reported a profit decline for fiscal 2024 due to weaker sales and expects the first half of the year to remain challenging. The British luxury company said on Wednesday that it made a pretax profit of 383 million pounds ($482.2 million) for the year ended March 30, down from GBP 634 million a year earlier.

- In the United States, retail sales were unchanged from March. April spending missed the 0.4% increase that economists had projected, according to FactSet. By comparison, a year ago, retail sales surged by 3%.

- Li Auto, a Chinese EV maker, was the worst-performing S&P Global Luxury stock, losing 9.0% in the past five days. The White House unveiled a slate of tariffs on China-made products from steel to electric vehicles on Tuesday, escalating trade tensions between the world’s two largest economies.

Opportunities

- BofA’s latest Global Fund Manager survey stated that investors are the most bullish since November 2021, noting that stock allocations are the highest since January 2022 and cash levels are at the lowest since June 2021. However, the team cautioned against growing risk assets as global growth expectations fell for the first time since November, with a net 9% expecting a weaker economy over the next 12 months. Higher inflation remains the biggest risk.

- Luxury store openings slowed worldwide in 2023 but are expected to pick up again in 2025 as more properties come onto the market and customers regain their appetite for spending, according to a report from the international estate agents Savills. Luxury companies may be opening more stores in India, China, and Dubai.

- Alexander Lacik, CEO of Danish jewelry maker Pandora, says his company is looking to significantly boost its crafting capacity with a new factory in Vietnam. The $150 million manufacturing facility, which will begin operations in early 2026, is its largest capital expenditure ever. Lacik also told David Ingles and Yvonne Man on “Bloomberg: The China Show,” that Pandora is seeking to reset its China business strategy.

Threats

- Month-over-month PPI for April was reported at 0.52%, well above the consensus of 0.3%, and March’s downwardly revised -0.1%. Annualized PPI was reported at 2.17%, in line with the consensus, reflecting the largest increase since April 2023. Core month-over-month PPI (excluding food and energy) was reported at 0.55%, above the consensus of 0.2%, and March’s downwardly revised -0.1%. Annualized core PPI was reported in line with the consensus at 2.37%. Odds for September rate cuts dropped slightly after the report, now at 60%.

- Ted Baker Canada, a luxury retail company operating in Canada and the United States, filed for bankruptcy and is shutting down 31 stores in the United States and nine stores in Canada. A 30% discount will be offered in stores during the liquidation sale.

- The Eurozone manufacturing PMI is likely to remain in contractionary territory. May’s preliminary index data will be reported on May 23. The prior reading was 45.7. A reading above the 50 mark would indicate expansion, while less than 50 indicates a contraction in manufacturing activities.

Energy and Natural Resources

Strengths

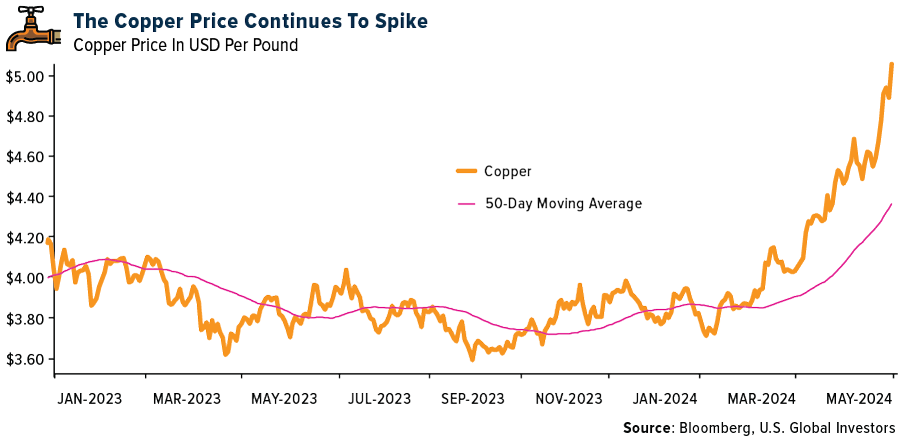

- The best performing commodity for the week was natural gas, rising 17.10%. Inventories rose less than expected and liquid natural gas (LNG) utilization is back to around 90%, boosting export demand. Copper and industrial metals saw broad advances, with fresh Chinese stimulus measures are boosting sentiment. Copper has rallied about 18% this year, buoyed by major supply disruptions and rising hopes for a global rebound in manufacturing and industrial activity, according to Bloomberg.

- China National Offshore Oil, the country’s state-owned oil and gas giant, is expanding its fleet of LNG carriers to increase its trading power on the global market. CNOOC Gas and Power Group, a company unit and the country’s biggest LNG importer, is more than doubling the fleet to increase its flexibility to move cargoes around the world and boost profit potential, it said in a statement.

- Overcapacity in China’s battery industry looks unlikely to deter producers of the raw ingredients that are powering the energy transition Tianqi Lithium is hunting for more reserves as it targets a major expansion in capacity, while Ganfeng Lithium Group just bought out its joint venture partner in a Mali project. Zijin Mining Group and CMOC Group also are looking for acquisitions, according to Energy Daily.

Weaknesses

- The worst performing commodity for the week was sugar, dropping 6.06% as production from Brazil, the world’s largest exporter, appears to be off to a strong start for the growing season. Returns from making diesel have fallen sharply over the last few months as supply of the industrial and transport fuel has outpaced demand, spurring refiners to cut run rates and focus on producing gasoline and jet fuel instead, according to Bloomberg.

- Two miners were killed and one remains missing after a cave-in at the Myslowice-Wesola coal mine in southern Poland early Tuesday in which 12 other miners were hurt, mining authorities said Tuesday.

- Spot HRC steel, or hot-rolled coil steel prices, are declining to $805 per ton, according to BMO, driven by limited spot activity, buyers continuing to purchase only on an as-needed basis and some mills offering larger tonnage deals through contract mechanism at meaningful discounts.

Opportunities

- Canaccord is raising their near and medium-term copper price forecasts to reflect changing market dynamics, particularly ongoing demand increases from data centers from the accelerating ramp up in artificial intelligence (AI).

- Oil prices have faced headwinds this quarter as choppy economic data has the market concerned over weaker prices with diesel demand waning, a key indicator of economic activity. However, over the past month, Kpler and Vortexa estimate that China has added more than 30 million barrels of crude inventories just over the past month, as reported by Bloomberg. This represents their fastest accumulation rate to restock inventories in the past year and Kpler’s analyst expect this trend to continue into May as China takes advantage of lower prices. This is big positive for the major oil producers that clearly make money at these price levels which are being supported by Chinese buying.

- Mining group Rio Tinto reportedly considered a bid for multinational Anglo American, which is now the subject of a $39 billion takeover bid by Australian giant BHP Group. According to the Australian Financial Review, Rio management had not ruled out making a play for part or all the mining group and continued to study the day-to-day situation, citing sources it said are close to Rio.

Threats

- President Joe Biden’s signature climate law unleashed a $16 billion flood of promised investments in solar manufacturing, as companies unveiled plans for factories across the U.S. and raised hopes of eroding China’s green tech dominance. But less than two years later, manufacturers have quietly shelved or slowed plans for at least four of those plants. High borrowing costs and record-low panel prices — the result of cheap imports pouring into the market — have made some projects uneconomical, according to Bloomberg.

- Recent agency actions should curb power and oil and gas emissions but face numerous challenges. Some regulations are already facing legal opposition, like the Good Neighbor Plan and GHG emission standards. Bank of America anticipates U.S. load growth of 2.1% year-over-year through 2030, which may test regional grid stability as utilities struggle to meet the call on thermal power.

- The Cobalt Institute has released its latest annual Cobalt Market Report, providing industry data for 2023. However, amid strong supply gains the market surplus widened in 2023 to 14.2kt (7% of overall market), and with both the DRC and Indonesia set to see further growth in the coming years, overcapacity seems a perennial issue, unless geopolitics limits material flow, according to BMO.

Bitcoin and Digital Assets

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performer for the week was Floki, rising 23.98%.

- El Salvador now owns 5,750 Bitcoin worth about $353 million at today’s prices, according to its government. The National Bitcoin office this week launched a tracking website for the Treasury’s holdings of the coin, according to Bloomberg.

- Coinbase Global shares rose as much as 5.3% on Friday after BofA Global Research analyst Mark McLaughlin raised the recommendations to neutral from underperforming, Bloomberg reports.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performer for the week was Ethena, down 13.44%.

- TeraWulf shares dropped 8% in premarket trading after the Bitcoin miner posted first quarter revenue that missed the average analyst estimate. Revenue was $42.4 million, and the estimate was $45.1 million. The company’s gross profit was $28 million, and the estimate was $32.6 million, reports Bloomberg.

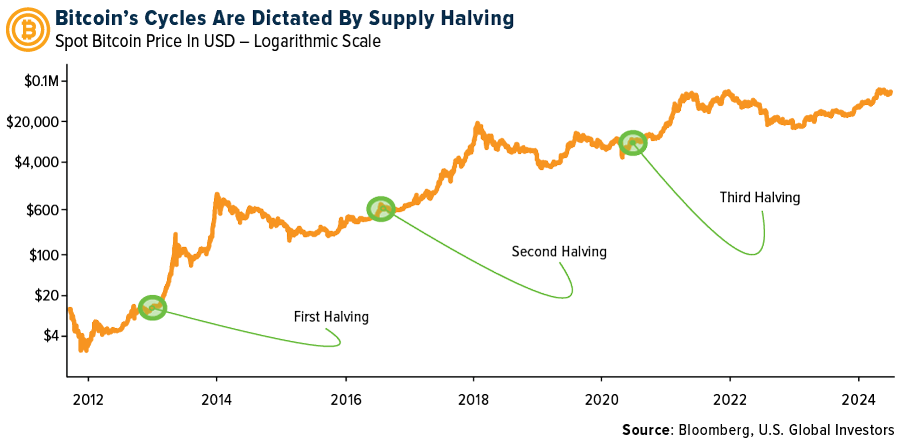

- Bitcoin could be losing its sizzle, and the next rally looks like a hard sell, according to some industry experts. The disappointing halving year appears to have dented the long-term bullish thesis and may drain money out of an industry that’s yet to prove its worth, writes Bloomberg.

Opportunities

- Michael Novogratz, the founder of digital-asset financial services firm Galaxy Digital Holdings, said Bitcoin is likely to remain stuck in a relatively narrow trading range for at least the current quarter while the adoption of crypto in traditional finance continues.

- CME group, the world’s largest futures exchange, is planning to launch Bitcoin trading, writes Bloomberg, aiming to capitalize on surging demand this year among Wall Street managers.

- Michael Ashby, who most recently led the digital-asset strategy implementation at hedge fund Point72, has joined a proprietary crypto trading firm AlgoQuant. He has joined as CEO and relocated to Dubai as part of AlgoQuant’s plans to build out operations in the UAE, reports Bloomberg.

Threats

- Alexey Pertsev, the developer of cryptocurrency mixing service Tornado Cash, was sentenced to five years and four months in prison by Dutch authorities for helping launder more than $2 billion, Bloomberg reports. Pertsev co-founded Tornado Cash with two other men in 2019 as a tool to make financial transactions harder to trace using a cryptocurrency.

- BlockTower Capital’s main hedge fund has been compromised and partially drained by fraudsters, according to people familiar with the matter. The funds are still missing, and the hacker has not been apprehended, according to Bloomberg.

- China busted an underground bank that illegally used cryptocurrency to conduct currency exchange operations between the Chinese yuan and the south Korean won involving at least 2.14 billion yuan ($295.8 million), writes Bloomberg. The local police arrested six suspects who allegedly facilitated the case in China and South Korea.

Defense and Cybersecurity

Strengths

- The U.S. Air Force has awarded Northrop Grumman a $7 billion contract to develop the B-21 Raider, a next-generation stealth bomber aimed at sustaining aerial superiority. Despite the significant investment, however, the 100 planned bombers may be insufficient for global needs, prompting analysts like Christopher Bowie to advocate for up to 300 to effectively counter major threats such as China.

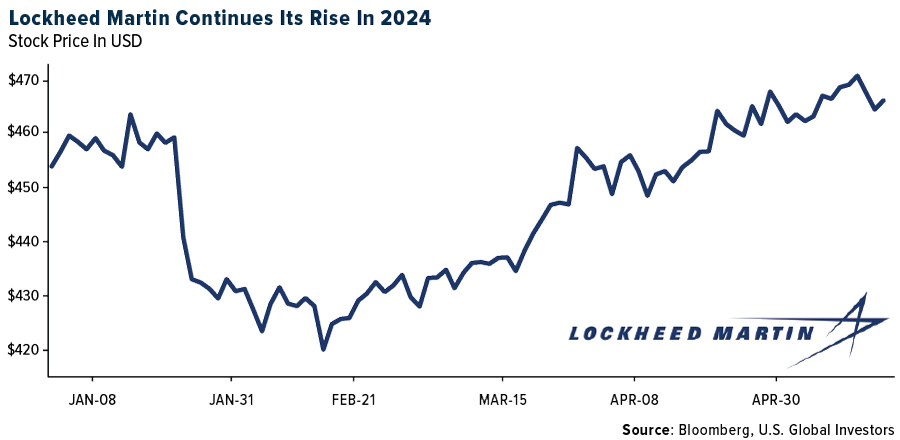

- Lockheed Martin has been awarded a $451 million contract by the U.S. Army to continue upgrading M270 missile launchers to enhance operational capabilities and interoperability with NATO forces. The upgrade includes incorporating new engines, armored cabs, and a Common Fire Control System, as part of an effort that began in 2019 and extends the systems’ functionality through 2050.

- The best performing stock this week was Mercury Systems, rising 13.08%, after Scopia Management reported a big position in the stock.

Weaknesses

- Boeing faces potential criminal prosecution after the U.S. Justice Department found it violated a deferred-prosecution agreement related to two fatal crashes, intensifying legal risks and scrutiny over its compliance with safety regulations and quality control. The company now has four weeks to respond to the allegations and the Justice Department will determine how to proceed.

- The Department of Justice announced that Boeing violated a 2021 settlement agreement by failing to implement a required compliance and ethics program to prevent fraud. This potentially could lead to prosecution for conspiracy to defraud the FAA and the company could face a $2.5 billion penalty, following the deadly 737 Max crashes in 2018 and 2019.

- The worst performing stock this week was V2X, falling 5.17%, after a change in the company’s top management.

Opportunities

- The House Armed Services Committee released its 2025 National Defense Authorization Act proposal, starting negotiations for the $849.8 billion military policy legislation, which includes $1 billion to fund two Virginia-class submarines but cuts funding for a new Fincantieri Marinette Marine frigate. Additionally, Rep. Andy Kim, running for Senate, diverges from the New Jersey party line by emphasizing mass transit improvements over highway projects.

- Northrop Grumman announced that CFO Dave Keffer will retire on February 21, 2025, with Kenneth B. Crews set to succeed him starting October 1, 2024, after serving as vice president of corporate finance from July 1 to ensure a smooth transition.

- Rapid7 has partnered with CSIT at Queen’s University Belfast to use AI and machine learning for advancing cloud security and detecting threats, as cybercriminals increasingly exploit AI for accessing cloud services.

Threats

- Russia has launched an offensive in Ukraine’s Kharkiv region, making tactical gains and already capturing a few villages and the city of Vovchansk. This renewed offensive is worse than expected, and all Ukrainian reserves are participating in the battle, but Russia is preparing for another attack from Sumy.

- Lockheed Martin’s F-35 aircraft are delayed on tarmacs awaiting crucial hardware and software upgrades, causing significant concern among lawmakers, and prompting proposed cuts in the defense budget until these issues are resolved.

- Russian President Vladimir Putin signed a decree appointing a new government, replacing the defense minister with a former deputy prime minister and economics expert with no military background. The news comes after the government submitted its resignation in line with Russian law following Putin’s inauguration for a new six-year term, reappointing Mikhail Mishustin as prime minister, moving Sergei Shoigu from defense minister to head of the national security council, and nominating Andrei Belousov as the new defense minister, (while also proposing names for returning and new Cabinet members, all approved by parliament).

Gold Market

Gold futures closed the week at $2,420.10, up $45.10 per ounce, or 1.90%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 3.73%. The S&P/TSX Venture Index came in up 2.98%. The U.S. Trade-Weighted Dollar fell 0.79%.

Strengths

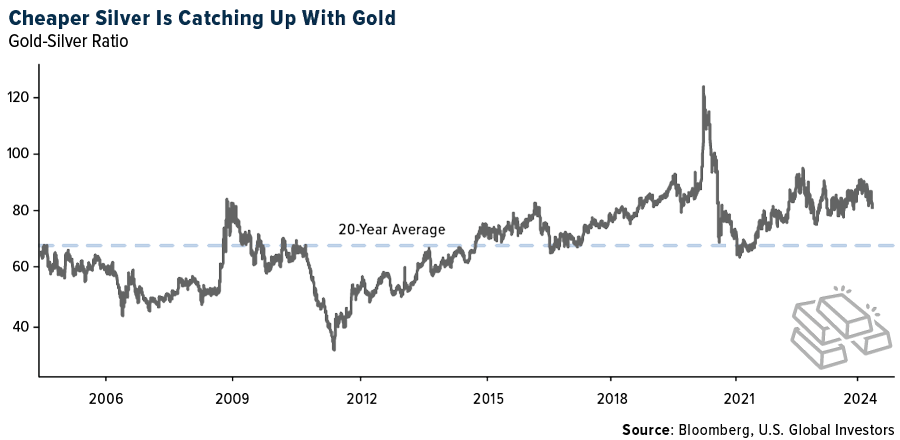

- The best performing precious metal for the week was silver, up 11.29%, breaking through $30 per ounce for the first time in more than a decade with an increasingly supportive supply picture for prices with a projected fourth year of market deficit in production, reports Bloomberg. Gold’s record-setting rally may have captured the headlines this year, but it is silver that’s running harder and faster as the less glamorous metal benefits from robust financial and industrial demand. Silver has soared by almost 29% in 2024, outpacing gold and making it one of the year’s best-performing major commodities, Bloomberg explains. Yet in relative terms, silver is still cheap. It currently takes about 80 ounces of silver to buy 1 ounce of gold, compared with the 20-year average of 68.

- Johnson Matthey sated that the platinum market deficit will increase to 598,000 ounces this year following a shortfall of 518,000 ounces in 2023. This represents the biggest deficit in the last 10 years. The primary supply is projected to decline by 2% as shipments from Russia return to normal levels from last year’s highs.

- Gold rose to the highest level in more than three weeks after the latest data showed ebbing inflation and weak retail sales, reinforcing expectations that the Federal Reserve will start cutting interest rates this year, writes Bloomberg.

Weaknesses

- The worst performing precious metal for the week was gold, but still up 1.90%. Gold slipped from a three-week high, says Bloomberg, as traders weighed a potential slowdown in the U.S. economy against persistent inflationary pressures that may hamper plans by the Federal Reserve to lower borrowing costs this year.

- South Africa’s gold production fell 4.5% y-ear-over-year in March versus revised -5% in February, according to Statistics South Africa. Mining production fell 5.8% year-over-year, according to Bloomberg.

- The volume of rough diamond imports in April fell by 15% year-over-year and 10% month-over-month, while their value declined by 18% year-over-year and 15% month-over-month. Run-rates are now back at their five-year average range, indicating a normalization of imports, according to Morgan Stanley.

Opportunities

- Gold equities’ performance has deviated from the underlying commodity due to various factors. However, Morgan Stanley expects this trend to reverse as headwinds fade and consensus expectations reset. Moreover, history points to gold equities typically outperforming gold following the initial Fed rate cut.

- The platinum market will remain in a deficit this year as a slowdown in the electric-vehicle boom supports demand for auto catalysts, according to the World Platinum Investment Council. Demand for the metal in the pollution-control devices climbed to the highest since 2017 in the first quarter and is expected to rise about 2% for the whole year, the WPIC said in a report on Monday.

- Anglo American Plc will exit diamond, platinum and coal mining in a massive restructuring designed to fend off a £34 billion ($43 billion) bid from rival BHP Group and turn itself into a copper giant. Anglo’s hand was forced by BHP’s approach — which it has twice rejected — but the move also responds to pressure from shareholders to shed less profitable businesses, reports Bloomberg.

Threats

- The diamond industry has already been feeling the heat. Prices have slumped, Russian sanctions are threatening trade, and the emergence of lab-grown gems is eating into some key traditional markets. Now, the sector’s most dominant name is being cast adrift, writes Bloomberg. Anglo American Plc on Tuesday said it will spin off or sell its De Beers business, ending an almost century-long relationship with the industry’s most famous name.

- The month-over-month import and export values of lab-grown diamonds have both declined, falling close to historical lows. This trend may reflect a weak pricing environment in the lab-grown market and/or a slowdown in demand, according to Morgan Stanley.

- Precious metals refiner Heraeus notes that, “Logically, a second year of (platinum) market deficits could indicate the possibility of a rising price environment. However, during the pandemic period alone, the platinum market built up in excess of 2 million ounces of additional stock that demand did not absorb. Therefore, the market is likely to require several years of fundamental market shortfalls before we see a meaningful impetus for higher prices”.

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission (“SEC”). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product. Certain materials in this commentary may contain dated information. The information provided was current at the time of publication. Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content. All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (03/31/2024):

Copa Holdings SA

United Airlines

Boeing The/Co

Frontier Group Holdings

JetBlue Airways

Burberry

Tesla

BHP Group Ltd.

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The S&P Global Luxury Index is comprised of 80 of the largest publicly traded companies engaged in the production or distribution of luxury goods or the provision of luxury services that meet specific investibility requirements.

In the Euro Area, the ZEW Economic Sentiment Index measures the level of optimism that analysts have about the expected economic developments over the next 6 months. The survey covers up to 350 financial and economic analysts.