Investor Alert

Miami’s Mining Disrupt Conference Shows the Path Forward for Bitcoin and Digital Assets

Date Posted: July 28, 2023

Read time: 37 min

I just returned from an invigorating week in hot and humid Miami, Florida, where I was privileged to present at the Mining Disrupt conference. This annual event attracts the who’s who of the digital asset mining industry, including top players, enthusiastic investors and Bitcoin advocates alike.

In my capacity as Executive Chairman of HIVE Digital Technologies, I was excited to shed light on our company’s involvement in the great digital transformation and expansion into the realm of artificial intelligence (AI) and Web3 applications. You can read about HIVE’s plans here.

Undeterred Optimism Amid the Ongoing Bitcoin Bear Market

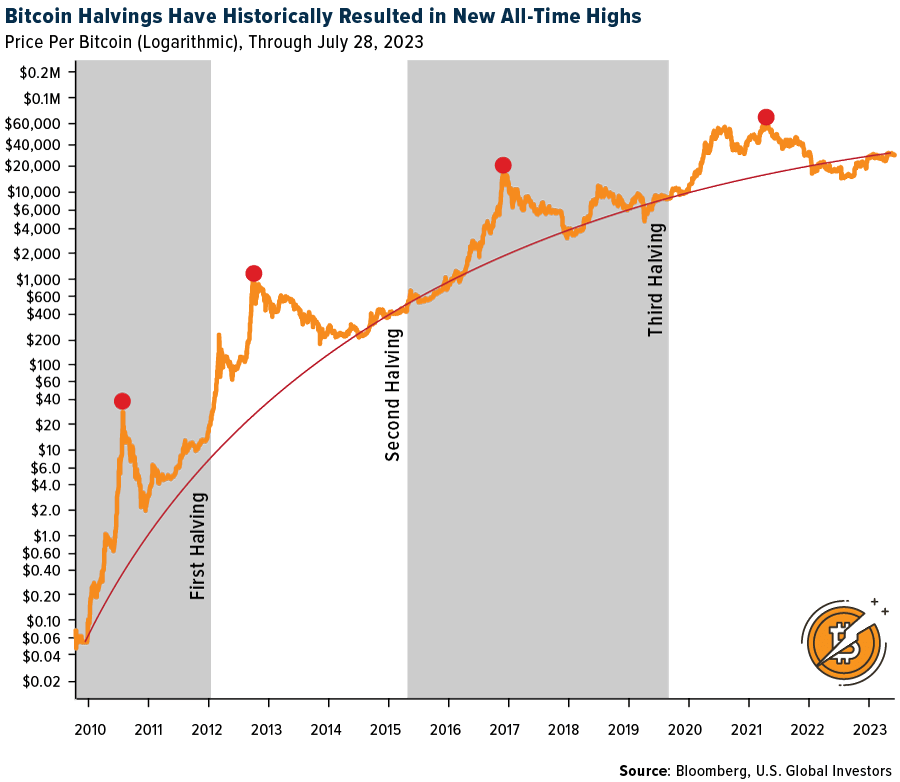

My fellow presenters and attendees were all incredibly bullish on Bitcoin, despite the ongoing bear market that has seen the digital asset retreat from its all-time high of nearly $69,000 in November 2021.

The conference coincided with Bitcoin crossing a significant milestone: the successful mining of the 800,000th block. This landmark event teases the upcoming fourth Bitcoin halving event, projected to happen when block 840,000 is mined in less than nine months from now. The halving process, which occurs approximately every four years, cuts the rewards for Bitcoin miners in half, thereby limiting new supply and creating scarcity.

Historically, every new cycle has resulted in a fresh record high price for Bitcoin. This phenomenon is attributed to the realization among investors that the asset’s supply is capped at 21 million coins, a factor that could spur the price to visit new highs.

Bitcoin in Need of Regulatory Clarity

Many presenters and panelists at the conference centered their message on the need for regulatory clarity in the mining space. Among the most esteemed speakers was Dennis Porter, co-founder and CEO of the Satoshi Action Fund, whose mission is to educate legislators and policymakers across the U.S. on Bitcoin’s varied benefits.

During his presentation, Dennis drew interesting parallels between Bitcoin and the cannabis industry, both of which have had to lobby for state-level acceptance and legislation, even as they continue to face federal-level restrictions. He touted his group’s success in getting Montana and Arkansas to pass the Right to Mine law, which protects Bitcoin miners and prohibits energy producers from imposing discriminatory rates on them. The Fund was also instrumental in moving the Texas legislature to kill a proposed anti-mining bill.

Democratic presidential candidate Robert F. Kennedy Jr. also participated at Mining Disrupt via Zoom, representing one of four current candidates who expressly support Bitcoin-friendly policies, the others being entrepreneur Vivek Ramaswamy, Florida governor Ron DeSantis and Miami mayor Francis Suarez, who opts to take his mayoral salary in Bitcoin.

Kennedy, who recently disclosed purchasing two bitcoins for each of his seven children, reaffirmed his intention to back the U.S. dollar with Bitcoin and exempt the asset from capital gains taxes if elected president, saying that such exemptions should primarily benefit small investors and businesses.

A Legislative Milestone for Digital Assets?

Meanwhile, in Washington, a bipartisan bill that aims to provide a regulatory framework for cryptocurrencies was advanced by a key congressional committee this week. This legislation, endorsed by the House Financial Services Committee, was in response to last year’s sudden collapses of several crypto firms, including Celsius and Voyager. It defines a cryptocurrency’s status as either a security or a commodity, expands the Commodity Futures Trading Commission’s (CFTC) oversight of the industry and clarifies the Securities and Exchange Commission’s (SEC) jurisdiction.

Despite some opposition, the bill received support from committee Republicans and some Democrats, marking a major legislative moment for the digital asset sector.

Make no mistake, the bill has been met with opposition, primarily from Rep. Maxine Waters, the leading Democrat on the Financial Services Committee, who believes the bill would cause confusion and reduce protections for consumers and investors. Similar concerns have been raised in the Democratic-led Senate.

However, many in the crypto industry remain optimistic, asserting that with bipartisan support, the bill could stand a chance in the Senate. The debate continues over whether these assets should be treated as securities or commodities, highlighting the need for regulatory clarity in this evolving sector.

Spot Bitcoin ETFs and Their Potential Approval

I also want to highlight the possibility of a spot Bitcoin ETF being approved in the U.S. At the Mining Disrupt conference, there was guarded optimism that this may happen soon, following repeated rejections in the past. I believe a spot ETF would be a significant catalyst for Bitcoin, potentially streamlining access for both institutional and retail investors and driving up demand and price.

Applications for such an ETF from multiple firms, including BlackRock, Fidelity, Invesco, VanEck and WisdomTree, have been published in the Federal Register, moving them one step further in the SEC’s approval process. The official journal of the U.S. government now has a window to accept, reject, extend or open these applications for public comments.

With the Bitcoin network inching closer to the next halving event and the simultaneous evolution of the ecosystem and regulatory landscape, the world is keeping a watchful eye on the digital asset’s progress. Here’s to the fascinating journey ahead!

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 0.66%. The S&P 500 Stock Index rose 1.01%, while the Nasdaq Composite climbed 2.02%. The Russell 2000 small capitalization index gained 1.09% this week.

- The Hang Seng Composite gained 4.82% this week; while Taiwan was up 1.54% and the KOSPI fell 0.06%.

- The 10-year Treasury bond yield rose 11 basis points to 3.954%.

Airlines and Shipping

Strengths

- The best performing airline stock for the week was Boeing, up 12.7%. For the week, TSA throughput was up 13% year-over-year on capacity up 10% year-over-year. July load factors are one percentage point higher year-over-year versus two percentage points in June. Airline web traffic increased 12% year-over-year for the week ending July 17.

- Bank of America’s tracker of the latest high-frequency freight indicators shows that ocean spot rates improved in July, in particular the Transpacific, driven by a successful July 15 price increase. Container spot rates are up 5% month-over-month, putting them 22% above January 2019 levels.

- Ryanair’s first quarter 2024 profit after tax is €663mn, 7% ahead of consensus. The beat relative to consensus was primarily driven by higher average fares in the quarter, up 42% year-over-year. The net cash position reached close to €1bn.

Weaknesses

- The worst performing airline stock for the week was Alaska Air, down 11.1%. Domestic leisure fares have been trending down over the past few months, although other airlines have been less concerned about that trend. Airlines with a larger component of long-haul international traffic continue to see strong demand, but there have been warning signs of pricing declines. ARC Corp., for example, reported domestic fares declined 6.5% in the June quarter, with each month successively lower. This data only reflects agency sales and misses web sales, but the trend is important because it is likely to continue through at least mid-fourth quarter 2023.

- Product tanker rates have declined materially on a time-charter-equivalent (TCE) basis to $31,000/$26,000 per day for LR2/MR vessels from $53,000/$37,000 per day at Scorpio Tanker’s 2QTD Update. The lower rates are driven by weaker Asia petrochemical feedstock demand, a prolonged maintenance cycle, and a slower ramp in China.

- On July 24, Volaris reported second quarter 2023 results, with adjusted EBITDAR of $212 million, for an EBITDAR margin of 27% and EBITDA of 172 million. Meanwhile, EBIT came in at 51 million, 30% below Bloomberg consensus on lower-than-expected unit revenues. The company reported unit revenue (TRASM) at -4% year-over-year, mostly in line with historical seasonality. Unit costs (CASM) fell by 13% year-over-year, mainly driven by CASM fuel, with CASM ex-fuel coming in up 14% year-over-year.

Opportunities

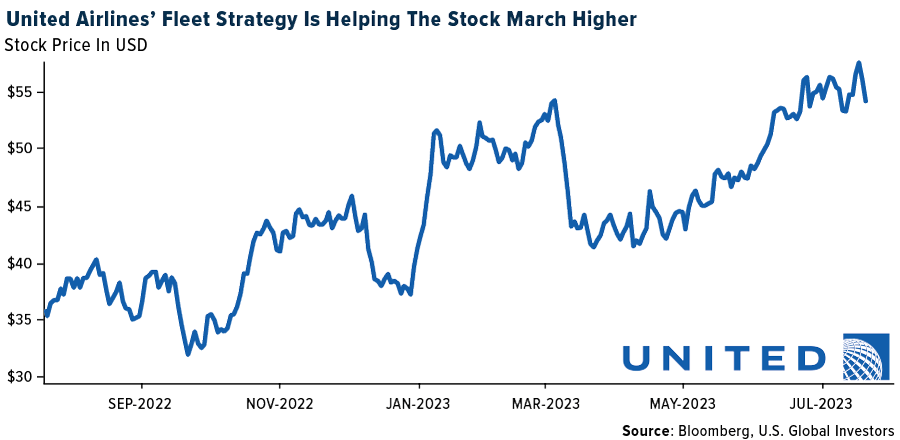

- United Airlines noted a large part of its strategy revolves around the larger single aisle narrowbody MAX 10 and A321 aircraft, which are not included in the carrier’s fleet today. Since 2019, United has increased gauge by 20%, which is “more than any other U.S. airline and 8 points more than the industry,” and management expects increasing gauge going forward will help drive costs down in the future. In addition to “superior economics,” these new aircraft are expected to serve the increase in premium leisure demand. All in, United has a large order book for narrowbodies, which will either allow for growth or retirement, depending on industry conditions, and management feels best positioned going forward as the largest international network amongst U.S. carriers.

- According to ISI, tanker EPS and dividend estimates remain robust, with 75% of its coverage universe providing yields of at least 7.5% for the next 12 months. Yet, ISI’s entire coverage trades at a discount to NAV, with some valuations matching those from times or prolonged losses and liquidity risk. Earnings season should again provide big gains and dividends and remind investors of the strong multi-year set-up, and winter will again be on the horizon, particularly for a continent that has lost its largest fossil fuel supplier.

- The International Air Transport Association (IATA) is projecting APAC to witness the highest pickup in activity during summer travel season as the region is the last one to re-open (versus North America and Europe). Specifically, forward bookings tracked by IATA indicate the region will witness the highest growth during May-September 2023.

Threats

- American Airlines announced a new pilot contract that matches the recently announced United Airlines agreement in principle. American’s newly announced contract raised its offer for pilots by more than $1 billion, increasing the four-year contract value to $9 billion, and will “match United pay rates, backpay and other benefits such as sick time and life insurance,” AAL’s CEO Robert Isom stated to pilots. Management made clear during the second quarter conference call that they are committed to match United’s wages and that they will return to the negotiating table if changes are not approved on a timely basis.

- According to ISI, the group’s initial view is that the overall labor cost inflation from the recent UPS Teamsters deal would approximate high-single-digit impact of costs (7-8%) in year one and a mid-single-digit increase (4-5%) in the last four years of the contract. ISI had been factoring in closer to 4% for year one and 3% going forward, thus there is the potential for cost per package inflation to exceed the estimates by several hundred basis points through ISI’s forecast horizon.

- Alaska reported a June-quarter beat but guided to a lower-than-expected September quarter unit revenue (“RASM”) and margin outlook. The worse-than-expected September quarter RASM guide implies a steeper deceleration than what is expected by its legacy peers that have exposure to stronger international markets, exacerbating investor concerns on domestic pricing that is coming off peak levels experienced in 2022.

Luxury Goods and International Markets

Strengths

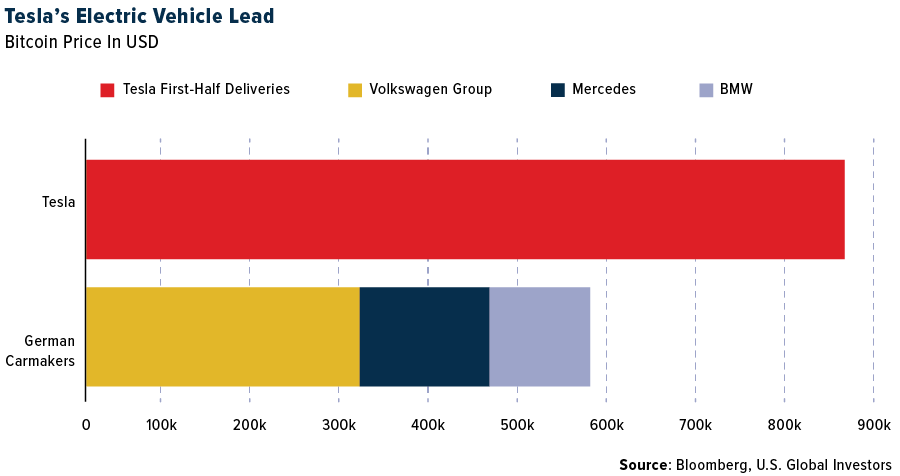

- Tesla Inc. has begun providing 84-month auto loans to customers after Elon Musk stated that the company would “have to do something” about rising interest rates. Musk also discussed with the Indian government the establishment of a new plant, which earlier claimed should produce 500,000 cars in India every year, as well as low-cost electric vehicles (EVs) for the Indian market. Tesla is the top EV vehicle manufacturer, but German manufacturers have revealed big intentions in recent years to compete with Tesla. Nevertheless, in the first half of the year, Tesla delivered 890,000 automobiles, which is more than Volkswagen, BMW, Mercedes, and Porsche combined.

- Kering SA has agreed to acquire a 30% stake in fashion house Valentino for €1.7 billion ($1.87 billion) in cash, as it seeks to boost growth amid struggles with its flagship brand, Gucci. The deal includes an option for Kering to purchase the remaining stake from Mayhoola, Valentino’s owner, by the end of 2028, and forms part of a strategic partnership that could lead to Mayhoola taking a stake in Kering.

- Nio Incorporated was the best performing S&P Global Luxury stock in the past five days, gaining 39.32%. After Volkswagen signed a framework agreement with Xpeng Incorporated, all Chinese EV carmakers reacted positively, and as a result, Nio also rose.

Weaknesses

- Louis Vuitton shares slumped this week as a sluggish U.S. economy impacted luxury sales, resulting in a 1% revenue drop. However, the company reported a 21% jump in sales in China, as its bigger global footprint has helped weather the U.S. slowdown better than its peers.

- Porsche AG is facing disruptions in its electric vehicle production due to severe supply chain issues, casting doubt on achieving its target of having battery electric vehicles account for 12-14% of total sales. Despite reporting a 10.7% increase in operating profit for the first half of 2023, reaching 3.85 billion euros ($4.25 billion), the company’s slower-than-expected recovery in the Chinese market and a potential slowdown in the German market present additional challenges.

- Sleep Number Corporation was the worst performing S&P Global Luxury stock in the past five days, losing 29.02%. After the company announced its second quarter results, shares reacted negatively due to a miss on sales.

Opportunities

- Remy Cointreau SA is optimistic about the recovery of high-end drink demand in the U.S. later this year and reiterates its expectation of steady annual sales growth. The company’s sales declined by 35% on an organic basis to €257.5 million ($285.4 million), as predicted, with U.S. cognac consumption returning to normal levels following a 2022 boom. Remy’s stock experienced a significant 8% increase during early trading. The company maintains its positive outlook, forecasting stable organic sales growth with a strong rebound in the U.S. starting in the third quarter and continued growth in China.

- BMW Group opened a new research and development facility in Shanghai to support its localization strategy in China, the world’s largest vehicle market. China is BMW’s largest R&D system outside of Germany, with advanced capabilities and 3,200 R&D employees focused on developing products tailored for Chinese customers, including the BMW Operating System 9 and the locally produced all-electric BMW i5 sedan.

- Volkswagen AG plans to invest $700 million in Xpeng Inc. to jointly develop electric vehicles in China and halt its sales slide. The company will eventually hold a 4.99% stake in Xpeng and deepen ties with SAIC Motor Corp Ltd. for its Audi brand’s EV lineup in China. The partnership aims to introduce two new battery-powered models to the market by 2026.

Threats

- The release of the iPhone SE 4 has been delayed until 2025, according to reports. The likely cause of this delay is related to troubles with the 5G modem. For the first time, the iPhone SE 4 was rumored to have Apple’s own 5G modem, although experts anticipate Qualcomm will continue to supply modems for both the iPhone SE and iPhone 16 lineups into next year.

- General Motors and its autonomous vehicle developer, Cruise, present a significant challenge to Tesla in the electric vehicle and autonomous vehicle market. Under the leadership of Kyle Vogt, Cruise aims to achieve costs below $1 per mile, potentially making robo-taxis more affordable than traditional car ownership. With General Motors’ broader global footprint and diverse range of brands, including Chevrolet, it has the capacity to challenge Tesla’s market share and pose tough competition in the EV and autonomous vehicle industry.

- This week was rich in economic statistics in the United States and the Eurozone; on Wednesday, the Federal Reserve raised interest rates by 25 basis points to 5.5%, the highest rate since 2001. The ECB also raised interest rates by 25 basis points. GDP in the U.S. came in significantly better than predicted, with annualized GDP quarter-over-quarter 2.4% versus 1.8% projected, and personal consumption 1.6% over 1.2% expected. The market remains robust, but it is already in a perilous state of greed, with 52-week highs on indexes and many assets, creating more risk of rates rising soon, credit levels falling, and growth drivers progressively melting away.

Energy and Natural Resources

Strengths

- The best performing commodity for the week was WTI crude oil, rising 4.58% on tightening supplies, perhaps on news that the European Union is looking at adding Russian nickel to its import ban this year. Fertilizer equities were up again this past week, supported by a combination of higher crop prices, upticks in nitrogen/phosphate, and stronger global energy prices. Nitrogen and phosphate markets continued to strengthen this past week, especially in Western markets: Brazil due to seasonal strength and the U.S. due to ongoing tightness exiting the spring season.

- Electra Battery Materials Corporation said its battery grade cobalt supply agreement with LG Energy Solution, a global manufacturer of lithium-ion

batteries, has been extended and expanded from terms initially

announced in September 2022. Electra will now supply LG Energy Solution with

19,000 tons of battery grade cobalt over a five-year period from 2025. The

material will be supplied from the only cobalt sulfate refinery in North

America, in Ontario. - World steel output rose 2.1% month-over-month, mostly driven by Chinese production, up 4.5% month-over-month. Ex-China output was down 1% month-over-month. Turkey rose another 5% month-over-month, continuing the post-earthquake recovery but Ukraine fell 23% month-over-month after the January-May improvement. Global utilization increased to 76.5% in June.

Weaknesses

- The worst performing commodity for the week was lumber, dropping 5.49%, on news that U.S. housing starts corrected sharply in June from a strong print in May. Global copper inventories remain low, but they have been rising in recent weeks and are now up 11% from this year’s trough, led by rising stocks in China. Bonded inventory continues to fall, but onshore stocks have been rising. China has been producing record volumes of refined copper this year, with very strong copper concentrate imports.

- S&P Global Platts believes further upside for ethane price is unlikely and that prices should moderate back to an average of $0.25 per gallon in the second half of the year. Ethylene stream cracker feedstock demand remains limited given prevailing weak petrochemical margins, with Ineos’ unplanned Chocolate Bayou, TX cracker outage in mid-July further reducing demand. Additionally, ethane export demand for June was down more than 20% from May. With the current infrastructure issues in the process of being resolved, the spike in ethane prices is expected to be temporary.

- According to UBS, copper demand in 2022 and the first half of 2023 has been lackluster but stable with energy transition demand offsetting weakness from the slowdown in construction/mixed domestic consumption in China and weakness in Europe/U.S. construction/manufacturing. UBS remains concerned about further weakness in demand in Europe in the second half of 2023 but expects a bottoming out in traditional demand drivers in Europe/U.S. in 2024.

Opportunities

- Lithium should be tight through the end of the decade. The swoon (and recovery) in prices year-to-date has likely given the market pause and volatility continues to hamper capital formation. While the demand side continues to tick along with regional and seasonal volatility (particularly from Asia) it is the supply side that remains relatively opaque.

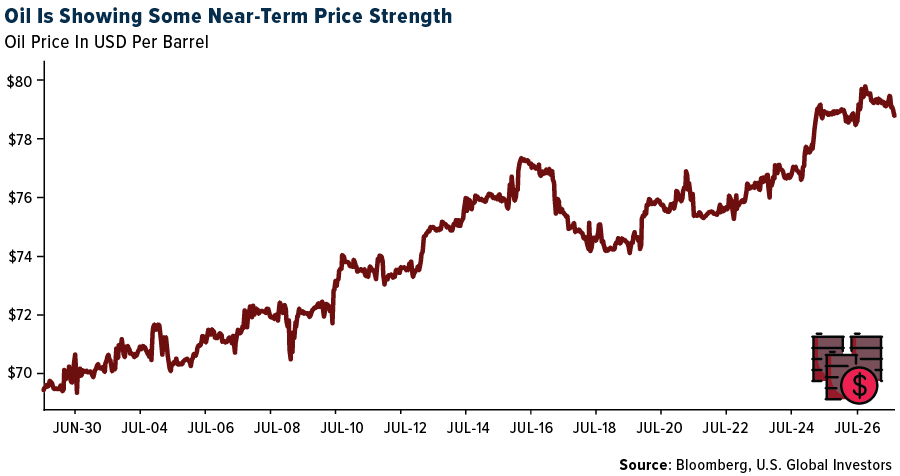

- Oil rose to $82.93 per barrel this week. The oil price recovery accelerated, supported by news of upcoming Chinese stimulus. The Chinese politburo met yesterday and signaled plans to adjust property policies and boost domestic demand. This more than offset weaker PMIs than expected in both the U.S. and Europe.

- U.S. raw steel mill capability utilization rose in the week, the American Iron and Steel Institute reported. Raw steel production was at 76.6%, up from 75.5% the previous week. Production during the week totaled 1.741 million tons, up 1.5% from the week ended July 15 when production was 1.716 million tons. Production increased 1.2% from the corresponding week a year ago, when capability utilization was at 78.1% and production totaled 1.721 million tons.

Threats

- JPMorgan has several indicators in its dashboard suggesting caution; cathode premiums are low (spot demand not as strong as it was), the copper/aluminum ratio is back to its high of 4x (substitution risk), prices are well above marginal cost, Chinese copper imports are flat year-over-year, and global production to April has risen a solid 4.5%.

- With regards to Belarus trying to build a new port in Russia for potash, the key takeaway is that it looks like no progress has been made in 18 months as BPC found existing Russian port operations. However, BPC exports out of Russia have been flat at around 650-700,000 tons per month for months and Russian exports from Uralkali/EuroChem stepped down in June.

- Steel imported from Mexico to the U.S. has increased materially in the past two years relative to pre-pandemic levels — up 43% in 2022 relative to 2018 and 92% relative to 2015. In fact, whereas prior to 2018, Mexico had a negative steel trade balance with the U.S., since 2018, it has become a net exporter of steel in trade with its northern neighbor. Among market participants, this has raised concerns that the U.S. might impose tariffs on imports of steel from Mexico.

Bitcoin and Digital Assets

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performer for the week was XDC Network, rising 42.23%.

- Binance will roll out full services on its new platform for Japan in August. The firm bought Sakura Exchange Bitcoin last November and said this May that it was creating a platform to fully comply with local rules, according to Bloomberg.

- 8000 Stan Lee digital collectibles sold out “nearly instantaneously” on Monday, illustrating strong demand for some virtual assets still exist despite the slow recovery of the NFT market, writes Bloomberg.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performer for the week was Gala, down 14.30%.

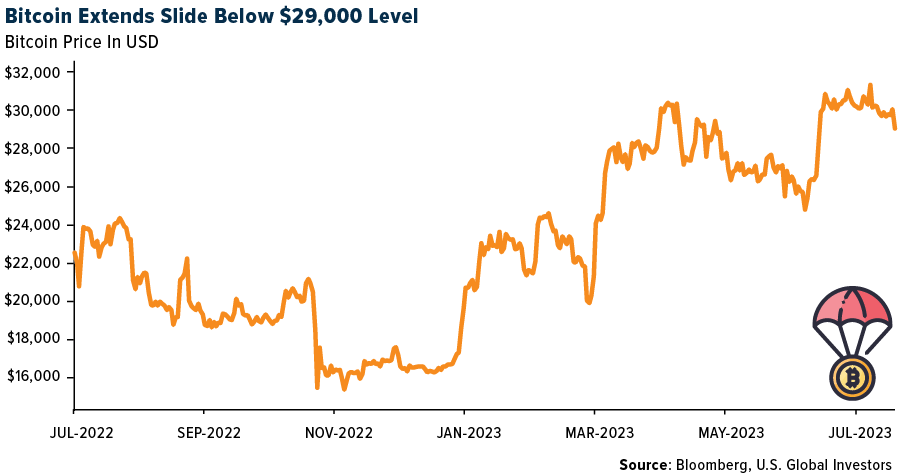

- Crypto miner stocks dropped this week as Bitcoin slid below $29,000. Stocks like Cipher Mining, Stronghold Digital, Hut 8, and Marathon fell alongside Bitcoin, according to Bloomberg.

- One of the most head-scratching phenomena playing out in the digital-asset world is the shrinking of the stable coin market while most cryptocurrencies are posting outsized gains this year, according to Bloomberg.

Opportunities

- Worldcoin, the token of the crypto project co-founded by OpenAI CEO Sam Altman, rallied on its first day of trading on Monday as investors piled into the hype surrounding artificial intelligence, writes Bloomberg.

- TD Cowen has initiated coverage and rated MicroStrategy “outperform” as the group cites both Bitcoin exposure and upside on business intelligence software. The stock has rallied about 209% this year through Tuesday’s close, writes Bloomberg.

- Digital Currency Group is nearing a deal to sell its media company CoinDesk to an investor group. The group is led by the founder of Tilly Capital and Venture capital firm Capital6, according to an article published by Bloomberg.

Threats

- FTX co-founder Sam Bankman-Fried was summoned to federal court in the Southern District of New York this Wednesday, according to a court filing. Bankman-Fried was summoned to address the adequacy and continuation of current bail conditions, writes Bloomberg.

- Sequoia Capital pared back the size of two major venture funds, including its cryptocurrency fund, as part of a dramatic downsizing the storied venture firm is undertaking amid a broad startup downturn, writes Bloomberg.

- Binance has withdrawn its application for a license from German financial regulator BaFin. The move follows a retrenchment from markets including Austria, Belgium, and the Netherlands and as its U.S arm is sued by regulators for operating an unregistered exchange, writes Bloomberg.

Gold Market

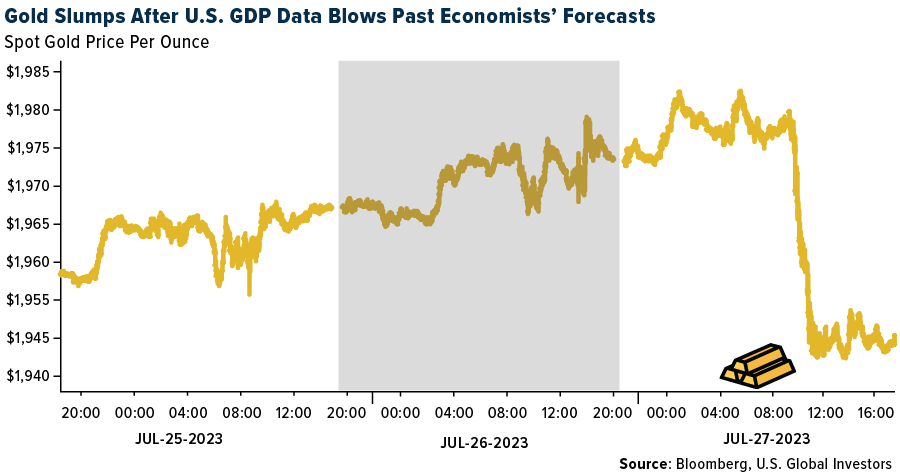

This week gold futures closed the week at $1,967.70, down $7.60 per ounce, or 0.38%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 2.21%. The S&P/TSX Venture Index came in up 1.37%. The U.S. Trade-Weighted Dollar rose 0.57%.

Strengths

- The best performing precious metal for the week was gold, but still down 0.38%. U.S. GDP came in higher than anticipated and pushed the dollar up on expectations the Fed still has room to raise rates higher. K92 Mining has completed its tender process and was awarded the engineering, procurement, and construction contract for its 1.2 million tons per year Stage 3 Expansion Process Plant to GR Engineering Services Limited, an Australian engineering consulting and contracting company. The contract is fixed at a price of $81 million, resulting in 94% of forecast capital cost for the process plant being fixed, which puts total capital costs within 10% of the $177 million projected.

- Agnico Eagle reported second quarter 2023 EPS of $0.65, a meaningful beat versus $0.55 consensus. Against consensus, the EPS beat was driven fundamentally by higher production. Second quarter gold production was 873,000 ounces, a beat versus 854,000 ounces consensus. Second quarter was the first full quarter of 100% ownership of Canadian Malartic.

- MAG Silver released second quarter production results at its 44% owned Juanicipio project. Silver production of 5.27 million ounces versus consensus of 3.39 million ounces and gold production of 10.6k ounces versus the 8.3k ounce consensus. Overall tonnage was 38% above consensus. Silver grade came in at 498 grams per ton versus the 450 grams per ton consensus. The company continues the mill-ramp up and remains on track to achieve 100% of the 4,000 tons per day nameplate capacity in the third quarter.

Weaknesses

- The worst performing precious metal for the week was palladium, down 3.23%, perhaps on news that the world’s largest producer, Nornickel, reported first half of the year production was higher than projected due to higher grades and improved recoveries. Newcrest’s fourth quarter result was weak with gold slightly below expectations and AISC 15% above consensus. Higher sustaining capex was in part a contributor, as was lower gold sales versus production, but copper by-product credits were in-line.

- According to UBS, Amplats’ first-half miss was primarily driven by a larger-than-expected loss on third-party purchases due to the adverse impact of a declining PGM basket price during the period. However, the mined operational performance was broadly in line with expectations, with medium-term production guidance unchanged and unit costs expected to moderate in the second half of the year.

- According to JPMorgan, De Beers’ cycle 6 sale of 2023 recorded $410 million of sales, down 10% versus cycle 5 of 2023 and down 36% versus cycle 6 of 2022. Cycle 6 sales track 13% below the $472 million average for cycle 6 over the 2016-2019 period.

Opportunities

- According to Stifel, K92 Mining’s share price is down 19% year-to-date, underperforming both the GDX and GDXJ. With the stock now trading at a P/NAV of 0.40x, despite having made substantial progress, the group views the current share price as an attractive buying opportunity.

- The North American Canaccord Genuity mining research team forecasts average AISCs up 3% to $1,343 per ounce in 2023 across its coverage universe (on a production-weighted basis), well below the 17% jump in 2022. Based on its 2023 forward-curve gold price of $1,942 per ounce, the research team forecasts AISC margins increasing by 21% to $599 per ounce, up from $496 per ounce in 2022.

- Analyst Giovanni Staunovo of UBS AG forecast that inflows into gold back ETFs will turn positive in the fourth quarter as consensus thought will conclude the Fed will be forced to cut interest rates by 25 basis points in December. Staunovo cites interest rates being the highest in 22 years and gold stockpiles in vaults backing the ETFs are at their lowest in three years. There is currently a significant spread between the correlation of the price of gold and the total know gold ETF holdings which manifests itself in November of 2022 as gold prices rallied 8.3% for the month while total known ETF holdings of gold actually fell 0.9% for the same period.

Threats

- The Globe and Mail published an article about how Russian cybercriminal group Clop targeted Barrick Gold as part of a global data theft incident in late May (in total, at least 376 organizations were impacted). Barrick has not revealed what effect the cyberattack has had, what data was stolen, or confirmed that an attack took place.

- Stifel is updating its model for Bear Creek Mining’s second quarter financials and Mercedes first-half production expectations. With weak production in the second quarter, Stifel now expects corporate FCF to come in at $7.4 million. Stifel is modeling second-quarter adjusted EPS of ($0.03) and operating CFPS pre-WC of ($0.06). The group’s modeling shows that Mercedes needs to consistently produce at head grade >3.3 grams per ton in order to work, so waste dilution is something it will be watching closely in the upcoming quarters.

- The number of so-called service-delivery protests in South Africa — demonstrations over the failure of municipalities to provide services such as electricity and water — may reach a new annual record. The country is suffering its worst-ever electricity blackouts and patience is fraying over the deterioration of municipal services, leading to 122 protests in the first six months of the year. At that rate, this year may overtake the 237 incidents of 2018, dwarfing the lull during the pandemic years.

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission (“SEC”). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product. Certain materials in this commentary may contain dated information. The information provided was current at the time of publication. Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content. All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (06/30/2023):

American Airlines

United Airlines

Alaska Air

Tesla

Kering

Volkswagen

BMW

Mercedes

Louis Vuitton

Remy Cointreau SA

BMW Group

Apple

Electra Battery Materials

K92 Mining

Agnico Eagle

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The S&P Global Luxury Index is comprised of 80 of the largest publicly traded companies engaged in the production or distribution of luxury goods or the provision of luxury services that meet specific investibility requirements.

Frank Holmes has been appointed non-executive chairman of the Board of Directors of HIVE Digital Technologies. Both Mr. Holmes and U.S. Global Investors own shares of HIVE. Effective 8/31/2018, Frank Holmes serves as the interim executive chairman of HIVE.