Ivanhoe Mines and Franco-Nevada Look Favorable Ahead of Earnings

Date Posted: July 31, 2020

Read time: 50 min

It's earnings season, and as I write this, profits for S&P 500 companies are down roughly 34 percent compared to the same time a year earlier, with 62 percent of companies reporting.

By Frank Holmes

CEO and Chief Investment Officer

U.S. Global Investors

It’s earnings season, and as I write this, profits for S&P 500 companies are down roughly 34 percent compared to the same time a year earlier, with 62 percent of companies reporting.

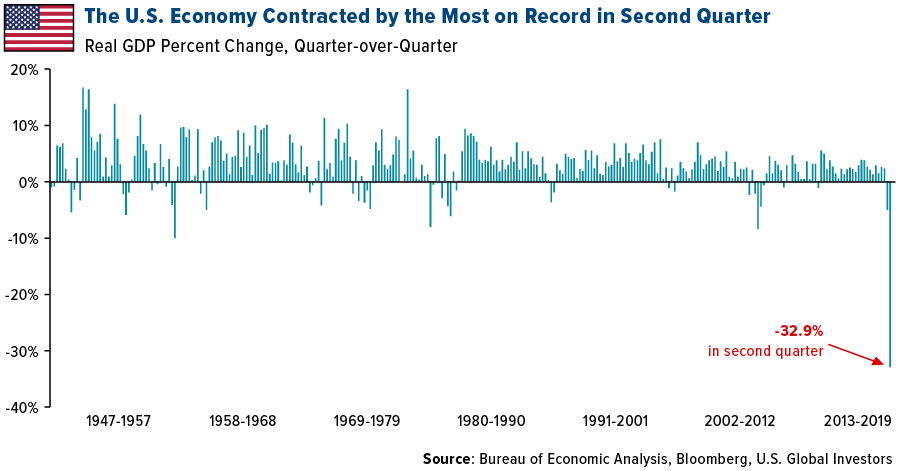

Coincidentally, that decline is close to the rate at which the U.S. economy shrank in the second quarter due to coronavirus lockdown measures. U.S. GDP plunged an historic 32.9 percent compared to the previous quarter, the fastest pace on record.

I know that sounds bad—and for the millions of Americans who are still out of work, it is—but I expect third-quarter GDP to be just as historic on the upside.

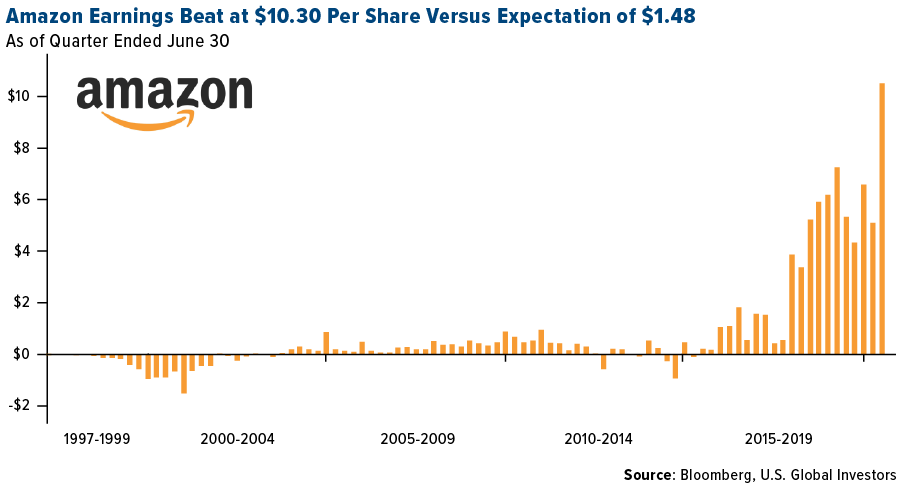

Not all companies have suffered in the age of COVID-19, though. Big tech earnings surged as a large percentage of the population was restricted to staying home, surfing the internet and making purchases online.

Retail giant Amazon had among the largest earnings beats, despite costs associated with the virus—protective gear, mostly, but also bonuses—reaching $4 billion. Earnings per share (EPS) came in at an off-the-charts $10.30, seven times above Wall Street’s expectation of $1.48. That’s the highest-ever EPS in the company’s 23 years as a publicly listed company. According to Amazon, video hours on Amazon Prime doubled during the three months. Online grocery sales tripled.

Copper Miner Ivanhoe Mines at an Advantage After Chile’s Charge Against BHP

Metal miners have also been reporting strong profits as prices for both industrial and precious metals were up during the quarter. Total earnings for those that have reported stand at more than $713 million, compared to estimates of $216 million.

Just under 40 North American gold producers have reported so far out of 284. Sales have been right in line with expectations, but earnings have surprised to the upside, with Yamana Gold, New Gold, Sandstorm Gold and Dundee Precious Metals pulling off the biggest beats.

Two companies in the metals and mining space I’m looking forward to hearing from are Ivanhoe Mines and Franco-Nevada. Both are scheduled to report next week.

For the two-year period, copper producer Ivanhoe has far outperformed copper prices and an index of global copper miners. Like most industrial metal producers, its stock price fell on fears the coronavirus would lead to mass mine closures and a global slowdown in demand for the red metal. Since hitting the bottom in mid-March, Ivanhoe shares have exploded more than 142 percent.

In a press release dated July 27, Ivanhoe founder and co-executive chairman Robert Friedland (pictured below, from when he visited our office in January 2018) calls 2020 an “extraordinary year” for metal prices. Copper is at a two-year high, silver at a silver-year high and gold at an all-time high.

“Our tier-one projects in Africa will produce all of these metals,” Robert says, referring to the company’s 100 percent-owned Western Forelands Project, Kamoa-Kakula mining license and Platreef Project.

|

|

|---|

Copper prices have been supported by global supply strains due to the pandemic, and further disruptions are a real possibility. Today, the Chilean government announced it would charge BHP, the world’s largest copper producer, for drawing too much water from the Chilean desert at the company’s Escondida copper mine.

Credit Suisse analysts rate this news as negative, as BHP could be fined, have its environmental permit revoked or even forced to close Escondida.

I agree that this is negative for BHP, but it could be positive for other copper mining jurisdictions, especially those that are friendlier to metal producers and that have an abundance of fresh water. That includes the Democratic Republic of the Congo (DRC), where Ivanhoe operates.

“We are blessed with incredibly high-grade depoists in areas that have an abundance of clean, sustainable hydro power potential—providing us with a distinct advantage in our goal to become the world’s ‘greenest’ miner,” Robert said in June, speaking of the Kakula Mine, which sits on the mighty Congo River.

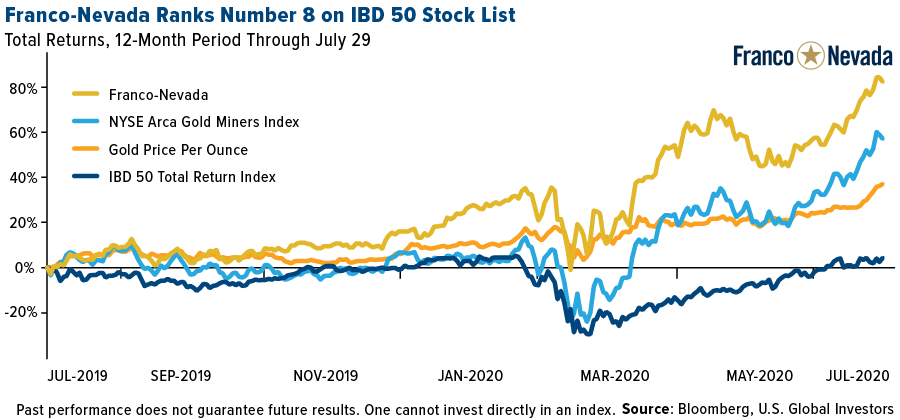

Franco-Nevada Rises to Number 8 on IBD 50 Stock List

I’m also expecting a strong report from Franco-Nevada. The world’s largest gold royalty company is up more than 83 percent for the 12-month period, beating gold producers and the price of the yellow metal.

It’s also beating the IBD 50 Index, which I’m including below because Franco-Nevada is now a member of the IBD 50 Stock List, the publication’s flagship screen of leading growth stocks. On Thursday the stock climbed to number eight on the list and is currently ranked first in the Mining-Gold/Silver/Gems Group based on its earnings potential. Analysts are looking for earnings growth of 41 percent in the second quarter, according to IBD.

Good for Gold: U.S. Yields Hit All-Time Lows

Spot gold continued to trade near all-time highs Thursday and Friday in its quest to break through $2,000 an ounce. Supporting the yellow metal was a falling U.S. dollar and anticipation of another round of fiscal stimulus. The real yield on the 10-year Treasury closed at a record low on Tuesday. The bond continued to trade lower throughout the week, falling to negative 95 basis points.

This week I shared with you my thoughts on gold being overbought, and whether this should prompt selling. In the period between 1980 and 1999, taking your profits was a good strategy after gold became overbought, but that same strategy has not worked in investors’ favor since 2000.

In the oscillator chart below, you can see that gold looks overbought at 2.14 standard deviations for the five-year period, so it’s important for investors to be cautious. A correction in the short term wouldn’t be unexpected. However, over the long term, I still believe gold will continue to head higher. Gold has been in a “golden cross” for around 18 months now, since January 2019, when the metal went above 1 standard deviation and then reverted to the mean. Afterward, it traded up.

Click here to see my complete analysis.

Congratulations, Thunderbird!

Some of you may not know that besides my roles at U.S. Global Investors and HIVE Blockchain Technologies, I am also an independent director at Thunderbird Entertainment, which was involved with the production of 2017’s Blade Runner 2049, among many other films and TV shows. The company trades in Toronto under the ticker TBRD.

I’m pleased to tell you that Thunderbird recently received some well-deserved accolades. Among them was an Emmy and four Leo Awards for the Netflix family series The Last Kids on Earth, three Leo Awards for the Canadian sitcom series Kim’s Convenience, and a Leo Award for the documentary TV series Highway Thru Hell. Congratulations to all who were involved! Kudos especially to CEO Jennifer Twiner-McCarron.

Upcoming Conferences and Webinars

A couple of notices about upcoming conferences and webinars you might be interested in…

This Monday, August 3, at 09:30 AM EST and 11:00 AM EST, I will be participating in an SNN Network Virtual Conference, discussing U.S. Global Investors and HIVE Blockchain Technologies. You can register for FREE by clicking here to attend the GROW webinar and here to attend the HIVE webinar.

Also, we are still trying to settle on a new date for the webinar co-hosted by me and Kevin O’Leary of O’Shares ETFs and Shark Tank. Some of you have already expressed interest in attending. If you’d like to be among the first to get the details as soon as they become available, please email us at info@usfunds.com. Have a wonderful, safe weekend!

Gold Market

This week spot gold closed at $1,975.86, up $73.84 per ounce, or 3.88 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 2.80 percent. The S&P/TSX Venture Index came in up 4.32 percent. The U.S. Trade-Weighted Dollar fell 1.0 percent and had its worst monthly drop of 4.04 percent in a decade.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Jun-27 | Hong Kong Exports YoY | 3.8% | -1.3% | -7.4% |

| Jun-27 | Durable Goods Orders | 6.9% | 7.3% | 15.1% |

| Jun-28 | Conf. Board Consumer Confidence | 95.0 | 92.6 | 98.3 |

| Jun-29 | FOMC Rate Decision (Upper Bound) | 0.25% | 0.25% | 0.25% |

| Jun-30 | Germany CPI YoY | 0.1% | -0.1% | 0.9% |

| Jul-30 | GDP Annualized QoQ | -34.5% | -32.9% | -5.0% |

| Jul-30 | Initial Jobless Claims | 1445k | 1434k | 1422k |

| Jul-31 | Eurozone CPI Core YoY | 0.8% | 1.2% | 0.8% |

| Aug-2 | Caixin China PMI Mfg | 51.1 | — | 51.2 |

| Aug-3 | ISM Manufacturing | 53.6 | — | 52.6 |

| Aug-4 | Durable Goods Orders | — | — | 7.3% |

| Aug-5 | ADP Employment Change | 1200k | — | 2369k |

| Aug-6 | Initial Jobless Claims | 1450k | — | 1434k |

| Aug-7 | Change in Nonfarm Payrolls | 1510k | — | 4800k |

Strengths

- The best performing metal for the week was silver, up 7.13 percent, again outpacing gold on recent gains. Spot gold broke its record high this week and could soon hit $2,000 an ounce. Bullion rose as high as $1,983.36 on Friday and is up 10 percent for July – its best month in four years. Precious metals producers are soaring thanks to gold and silver’s gains. The NYSE Arca Gold Bugs Index rose 108 percent from a March 13 low through July 24. The Solactive Global Silver Miners Index rose 117 percent over the same period.

- The real yield on 10-year Treasuries closed at its lowest level ever of negative 0.9277 percent on Tuesday. This greatly boosts gold’s appeal since it does not offer interest like government bonds usually do. Germany became the biggest retail buyer of gold bars and coins by the end of the second quarter, taking the top spot from China, according to the World Gold Council (WGC).

- The number of gold bulls is growing. Bank of America is sticking by its forecast for $3,000 an ounce gold over the next 18 months. Citigroup said that the current gold cycle is unique and prices could “stay in a higher range for longer.” Goldman raised its 12-month price forecast to $2,300. Miners are also bullish. Agnico Eagle Mines CEO Sean Boyd said, “we would not be surprised to see $2,500 within the next two years because there’s still so much uncertainty out there.”

Weaknesses

- The worst performing metal for the week was palladium, down 6.12 percent even though hedge funds boosted their net long position to a 21-week high, however, Nornickel announce a 32 percent quarter-over-quarter growth in its production of palladium taking some of the enthusiasm out of the price. Gold retreated on Wednesday after rallying for nine straight days that led to its record price. Investors weighted impending U.S. GDP data and second-quarter corporate earnings.

- The U.S. Mint said it has reduced the volume of gold and silver coins for distribution as the pandemic slows production. A document obtained by Bloomberg says that the Mint’s West Point complex in New York will probably slow coin production for 12 to 18 months as it implements measures to prevent the virus spreading among employees.

- JPMorgan says the gold rally could start to lose steam in the second half of this year. Analysts said in a report that “gold will likely see one last hurrah before prices turn lower into year-end.” Some believe that the gold rally is overdone and will correct soon after rising 29 percent so far this year.

Opportunities

- Gold’s new record price is winning over a wider fan base of pension funds, insurance companies and private wealth specialists, reports Bloomberg. Government bonds have been a traditional safe haven asset, but with bonds yielding next to nothing in the era of near-zero interest rates, the appeal for gold, which does not pay interest, rises. “We need to diversify our diversifier and look for safe haven beyond government bonds,” said Geraldine Sundstom of Pacific Investment Management Co.

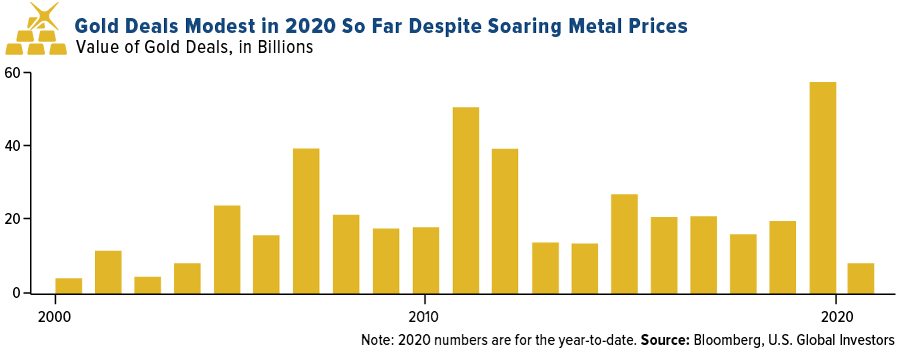

- Gold mining stocks are set to be massive beneficiaries of bullion’s rally, creating a “fat pitch”. However, miners are known for overspending and destroying shareholder value in previous cycles. So long as miners don’t repeat the mistakes of previous rallies, they should attract a surge in money flows. Gold deals are modest in 2020 despite higher metal prices, but the opportunity is there.

- Desjardins’ gold analyst David Stewart raised his price target on K92 Mining and wrote these positive remarks: “We are increasing our target to C$9.75 based on the recently released Stage 3 expansion PEA results, which beat our expectations across the board. We see the mine plan as transformative not only because it is self-funded (positive FCF even in expansion years), but because it will vault K92 into the intermediate producer category and create one of the lowest-cost producers in the industry. We see the PEA as a solid base from which to grow as exploration continues to expand resources.”

Threats

- Plummeting gold demand out of India could continue for longer than expected. Consumption fell in the first half of this year by 56 percent from a year earlier to 165.6 tons, according to the World Gold Council (WGC). “For gold demand to survive, the economy has to do well” and India’s economy has been hit severely by Covid-19 lockdowns, says P.R. Somasundaram of the WGC. However, if the economy were to surge back to life then demand could skyrocket.

- Billionaire investor Ray Dalio is warning of a “capital war” between the U.S. and China that could push the dollar down and lose its status as the world currency. “There’s a trade war, there’s a technology war, there is a geopolitical war and there could be a capital war,” Dalio said on Fox TV over the weekend. Although gold historically moves in the opposition direction of the U.S. dollar and would likely benefit from it going lower, this is still negative overall for the U.S.

- AngloGold Ashanti, the world’s third largest gold producer, announced that CEO Kelvin Dushnisky is stepping down after two years on the job. According to people familiar with the matter, shareholders pushed Dushnisky to leave after asking for further investigation into a bonus payment made by his previous employer Barrick that wasn’t initially disclosed. Bloomberg reports that before working at AngloGold, Dushnisky agreed to a signing bonus to made up for a Barrick payment that he would lose out on. However, Barrick’s annual report showed that he did in fact receive the bonus and was asked by the board to repay it.

Index Summary

- The major market indices finished mixed this week. The Dow Jones Industrial Average lost 0.84 percent. The S&P 500 Stock Index rose 0.93 percent, while the Nasdaq Composite climbed 2.71 percent. The Russell 2000 small capitalization index lost 0.81 percent this week.

- The Hang Seng Composite lost 2.19 percent this week; while Taiwan was up 2.03 percent and the KOSPI rose 1.50 percent.

- The 10-year Treasury bond yield fell 4 basis points to 0.539 percent.

Domestic Equity Market

Strengths

- Information technology was the best performing sector of the week, increasing by 4.98 percent versus an overall increase of 1.37 percent for the S&P 500.

- L Brands was the best performing S&P 500 stock for the week, increasing 27.20 percent.

- Apple blew past expectations for its fiscal third-quarter earnings, reporting revenue of $59.7 billion for the quarter ended June 30. Apple reported growth across all its product lines, from the iPhone, which has seen slowed growth in recent years, to its booming wearables and services businesses.

Weaknesses

- Energy was the worst performing sector for the week, decreasing by 4.23 percent versus an overall increase of 1.37 percent for the S&P 500.

- General Electric Co was the worst performing S&P 500 stock for the week, falling 11.52 percent.

- Exxon Mobil reported the biggest loss in its modern history and said that a full recovery in demand for petroleum won’t happen well into 2021.

Opportunities

- SAP has announced that Qualtrics, the subsidiary it purchased for $8 billion in 2018, will be going public. The company said that SAP’s board has already approved the deal, and that it plans to maintain its majority stake in the company even after the IPO.

- Amazon reported a record quarterly profit and 40 percent sales growth backed by strong Covid-related demand. Amazon had $5.2 billion in net profit, after having warned it would spend the $4 billion it was expecting to make for the quarter on Covid-related initiatives. Amazon also won FCC approval to launch 3,236 Kuiper internet satellites — a $10 billion project competing with SpaceX’s emerging Starlink network.

- Facebook beat expectations for revenue, profits and user growth. The social media giant also indicated that an ongoing advertiser boycott is not hurting badly.

Threats

- Goldman Sachs says stocks have never been more vulnerable to the failure of a few mega-companies and the risks of a blunder are quickly piling up. The stock market’s gains have been largely driven by five tech stocks and one misstep by any of them could send the market reeling.

- Alphabet announced its second quarter earnings and saw its first-ever revenue decline, as the coronavirus crisis continues to pummel the advertising industry. Google will face a full EU inquisition over its $2.1 billion purchase of fitness wearables maker Fitbit. Regulators in Europe worry that Google will use its acquisition to collect even more personal data on users and use it to inform targeted ads.

- Device maker Garmin was hit by a huge outage through Thursday thanks to a ransomware attack.

The Economy and Bond Market

Strengths

- The homeownership rate, led by young buyers, jumped to the highest since 2008, signaling that the housing boom underway before the pandemic has only accelerated. The rate was 67.9 percent in the second quarter, according to a Census Bureau report.

- Consumer spending increased for a second straight month in June, setting up consumption for a rebound in the third quarter, though the recovery could be limited by a resurgence in Covid-19 cases and the end of expanded unemployment benefits. The Commerce Department said on Friday that consumer spending, which accounts for more than two-thirds of U.S. economic activity, rose 5.6 percent last month after a record 8.5 percent jump in May as more businesses reopened.

- Orders for durable goods lasting at least three years rose to 7.3 percent in June for the second straight month after historic declines in the early spring.

Weaknesses

- The real yield on 10-year Treasuries closed below its previous record low, set in December 2012, on Tuesday. Even as stocks trade well above their March pandemic lows, inflation-adjusted yields have been sinking since early June, signaling trouble ahead for growth.

- The U.S. economy saw the biggest quarterly plunge in activity ever with second quarter GDP June plunging 32.9 percent on an annualized basis, according to the Commerce Department’s first reading on the data released Thursday. Economists surveyed by Dow Jones had been looking for a drop of 34.7 percent.

- The number of Americans applying for jobless benefits rose for the second straight week. Claims had been on a steady decline after peaking in late March. Initial jobless claims rose by 12,000 to 1.434 million in the week ended July 25. A new federal relief program for so-called “gig” workers like Uber drivers, totaled 829,607 last week.

Opportunities

- According to Bloomberg, the stability of the high-frequency statistics tracking nationwide lockdowns between the June and July payroll survey weeks suggests next week’s jobs report could show a positive gain. Expectations are for a gain of 1.5 million.

- Next week’s ISM Manufacturing Survey is expected to increase to 53.6 from the prior 52.6.

- DWS Group, an asset-management firm, said a survey of its insurance company clients in the U.S., Canada and Bermuda found that 15 percent have increased their allocations to state and local government debt, compared with 5 percent that trimmed their share. The amount boosting their municipal-bond stakes was second only to the 25 percent of clients that increased allocations to investment grade corporate bonds. DWS and Greenwich Associates polled insurance-company clients with portfolios from $1 billion to more than $20 billion.

Threats

- Billionaire investor Ray Dalio warns a developing ‘capital war’ between the U.S. and China could tank the dollar. "There’s a trade war, there’s a technology war, there is a geopolitical war and there could be a capital war," he said on Fox Business.

- The Federal Reserve left interest rates near zero and vowed to use all its tools to support the recovery from an economic downturn that Chair Jerome Powell called the most severe in our lifetime. “The path forward for the economy is extraordinarily uncertain, and will depend in large part on our success in keeping the virus in check,” he told reporters in a virtual press conference Wednesday after the Fed left interest rates near zero.

- Tens of millions of unemployed Americans will lose $600 in additional weekly jobless benefits after the White House and Congress failed to reach an agreement to extend the supplement.

Energy and Natural Resources Market

Strengths

- The best performing commodity for the week was raw sugar, up 10.01 percent and marking its third monthly gain on expectations China will increase its imports. Precious metals continue to be the winners amid commodities so far in 2020. Gold broke its record high price of $1,900. Silver has jumped to around $24 an ounce, its highest level since 2013. PGHM, the world’s second largest silver producer, has gained 32 percent so far this year. Nickel hit a six-month high on Monday as the outlook demand improves out of China and interest in batteries grows.

- The WilderHill New Energy Global Innovation Index is up 28 percent so far year-to-date led by electric car makers, solar installers and fuel cell developers. Bloomberg notes that four companies in the index have seen their shares triple from the start of 2020 to July 23. Despite fears that the Covid-19 pandemic could hurt residential solar installations and door-to-door sales, solar stocks have still gained.

- Royal Dutch Shell and Total were “saved” from a potential worst quarter ever thanks to their oil trading operations. Bloomberg notes that both companies reported gains in trading that offset losses from record low oil prices and plummeting demand amid the virus. However, Exxon Mobil and Chevron reported record low earnings. Exxon posted a $1.1 billion second quarter loss and Chevron around $3 billion.

Weaknesses

- The worst performing commodity for the week was uranium, measured by Uranium Participation Corp’s share price, down 6.09 percent on the announced restart of the Cigar Lake Mine by Cameco in the third quarter. A sharp rebound in gasoline consumption appears to be slowing. The world’s biggest gasoline market, the U.S., has seen demand flatten out during summer, which is meant to be the peak driving season.

- Iran, OPEC’s second biggest producer, is facing chronic power outages on top of low oil prices. Fatih Birol, head of the International Energy Agency, said that Iran needs to quickly boost electricity or it could threaten political stability.

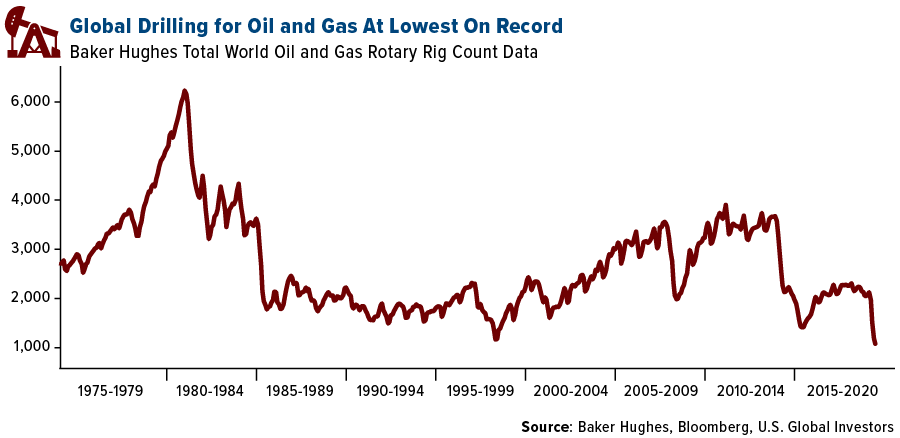

- According to Baker Hughes data, energy companies in the U.S. added one additional rig, halting a record streak of rig retirements. There are now 181 active rigs nationwide. However, global drilling for oil and gas is still at the lowest on record, as seen in the chart below.

Opportunities

- China’s biggest oil company, PetroChina Co., said it will use some of the $38 billion in proceeds from selling its pipelines on wind and solar. While oil majors globally have been slowly investing in greener energy, China has largely held back. PetroChina’s wind and solar plans mark a big shift.

- Vale SA, one of the world’s biggest miners, decided to resume its dividend saying the worst of the pandemic is behind it. In a statement on Wednesday, the miner said “Following the reduction of uncertainties related to the pandemic, with risks of a second wave in China mitigated and the stabilization and decline in Covid-19 cases, especially in the northern states of Brazil, Vale assesses that the worst is likely behind us.”

- Linde announced it will begin construction on the world’s first hydrogen refueling station for passenger trains in Germany this September, reports Bloomberg. The refueling station will serve 14 hydrogen-powered trains and has capacity of 1,600 kilograms of hydrogen per day.

Threats

- in a statement that “the flood control and flood fighting situation is severe” and “the new peak may appear later.” Bloomberg reports that more than 2 million people have been evacuated in July along the Yangtze River.

- A season of droughts and floods have taken a toll on Europe’s crops. Bloomberg reports that farmers in France, the EU’s top exporter, are pulling one of the smallest wheat crops in recent memory, down by almost a quarter. Romania, the second largest exporter, is reporting the smallest wheat crop since 2012.

- The U.S. economy shrank at a record 32.9 percent annualized pace in the second quarter and jobless claims rose almost 900,000 in the most recent week. This is sparking fears that a resurgence of the virus nationwide could have an even larger impact.

Emerging Europe

Strengths

- Russia was the best performing country this week, gaining 1.7 percent. Sberbank’s second-quarter profit fell 33 percent from a year earlier, beating estimates as Russia’s biggest bank began to recover from the coronavirus lockdown. Bloomberg reported that banks benefited from a string of interest rate cuts and state subsidies for mortgages, lending to a record volume of home loans. Polyus, a gold producer, was the best performing stock trading in the VanEck Vector Russia ETF (RSX), gaining 18 percent over the past five days.

- The Hungarian forint was the best performing currency this week, gaining 1.5 percent. The currency was supported by stronger economic data. Economic and business confidence improved slightly, unemployment rose but not by as much as expected, and average gross wages climbed 9.4 percent in May on a year-over-year basis.

- Health care was the best performing sector among eastern European markets this week.

Weaknesses

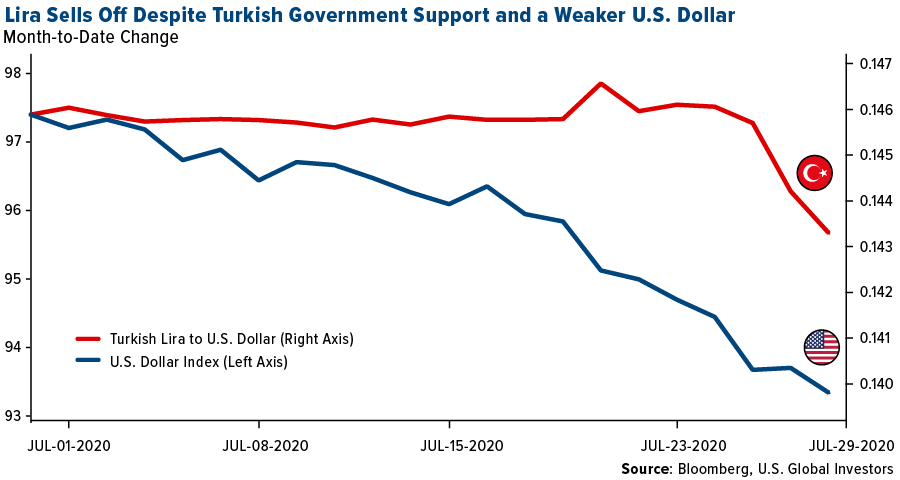

- Turkey was the worst performing country this week, losing 5.5 percent. Equities sold off on investors’ worries over the country’s growing debt level. Turkey’s gross currency reserves dropped almost 40 percent since the beginning of the year to $49.2 billion, according to Bloomberg. AD Anadolu Grubu Holdings, a holding company servicing customers worldwide, was the worst performer among stocks trading on the Istanbul Stock Exchange, losing 12.7 percent over the past five days.

- The Russian ruble was the worst performing currency in the region this week, losing 3.4 percent. Russian equities trading in local currency were the best performing among CEE countries; however, the ruble depreciated against the dollar by 3.3 percent, erasing gains for U.S. investors. The currency has been under pressure over concerns of possible U.S. sanctions and the slowing rebound in oil. Moreover, last Friday, Russia’s central bank cut its main rate by 25 basis points, from 4.5 to 4.25 percent.

- Industrials was the worst performing sector among eastern European markets this week.

Opportunities

- Russia intends to be the first one in the world to approve a coronavirus vaccine. Russian officials told CNN they are working toward a date of August 10 or earlier for approval of the vaccine, which has been created by the Moscow-based Gamaleya Institute. However, there is concern human testing of the vaccine is incomplete and that its fast approval comes amid political pressure from the Kremlin.

- A joint venture between Royal Dutch Shell Plc and Eneco NV won the right to build and operate a wind farm off the coast of the Netherlands. When it becomes operational in 2023, the wind farm will provide enough electricity for more than 1 million Dutch households. More big clean-power developers may be willing to build clean energy power plants as Europe set a plan to transform the 27-country bloc from a high-to a low-carbon economy.

- ECB President Lagarde said in an interview with Le Courrier Cauchois that we should envision support continuing beyond 2020. She added it really has to maintain the safety net and very attractive conditions at least until June 2021. She said it wants to encourage banks to continue to lend in the same volumes as before the coronavirus crisis, and pointed to the targeted nature of its loans and the attractive rates.

Threats

- The Turkish lira depreciated sharply against the U.S. dollar and may continue its downtrend. Investors worry about the country’s growing debt level, government innervations to support the lira and potential sanctions from the eurozone for Turkey’s proposed plans to drill for oil and gas in waters near Greece – not to mention U.S. sanctions for purchasing military equipment (the S400) from Russia last year.

- The FT reported that public health officials are sounding the alarm over a resurgence of coronavirus cases in Europe as countries ease lockdowns and international travel ramps up, with some experts warning that citizens have become too complacent. The increase is marked in countries such as Spain, while Eastern Europe and the Balkans, which were largely spared the worst of the early pandemic, are seeing a steep increase in recorded cases. The article points out that experts are surprised at how fast the lifting of restrictions has led to a rise in infections.

- Germany’s gross domestic product in the second quarter contracted by 10 percent, above the expected contraction of 9 percent, recording the biggest revenue decline since 1970. The GDP of the entire EU contracted by 12.1 percent in the second quarter with Spain and France recording the steepest losses. Spain’s GPD contracted by 22 percent in the second quarter and France’s 19 percent.

China Region

Strengths

- Pakistan was the best performing country this week, gaining 4.4 percent. Pakistan received over $505 million from the World Bank on Tuesday under a financing agreement signed last week to provide financial support. Honda Atlas Car, an automobile maker, was the best performing equity among stocks trading in the Global X MSCI Pakistan ETF (PAK), gaining 23.2 percent over the past five days.

- The Thailand baht was the best performing currency this week, gaining 1.3 percent. Asian currencies rallied, led by the Thai baht, on dollar weakness after data raised doubts on the strength of the U.S. economy.

- Material stocks were the best performers in the Hong Kong Stock Exchange.

Weaknesses

- Vietnam was the worst performing market this week, losing 3.7 percent. The World Bank estimated that growth in the export-reliant nation will slow to 2.8 percent this year, the slowest pace in 35 years, amid the coronavirus pandemic. FLC Faros Construction Company was the worst performing equity among stocks trading in the VanEck Vietnam ETF (VNM), losing 13.6 percent over the past five days.

- The Indonesia rupiah was the worst performing currency this week, losing 81 basis points. The currency declined on rising coronavirus cases. Indonesia recently overtook China as the country with the most confirmed coronavirus cases in East Asia, and authorities said the actual infection rate could be higher due to undetected cases.

- Energy stocks were the worst performers in the Hong Kong Stock Exchange.

Opportunites

- Official PMI figures for July in China came in at 51.1 – above the 50 level that separates growth from contraction. Non-manufacturing PMI was 54.2. PMI is a sentiment gauge, and with both readings in positive territory, it provides hope for China’s growth outlook.

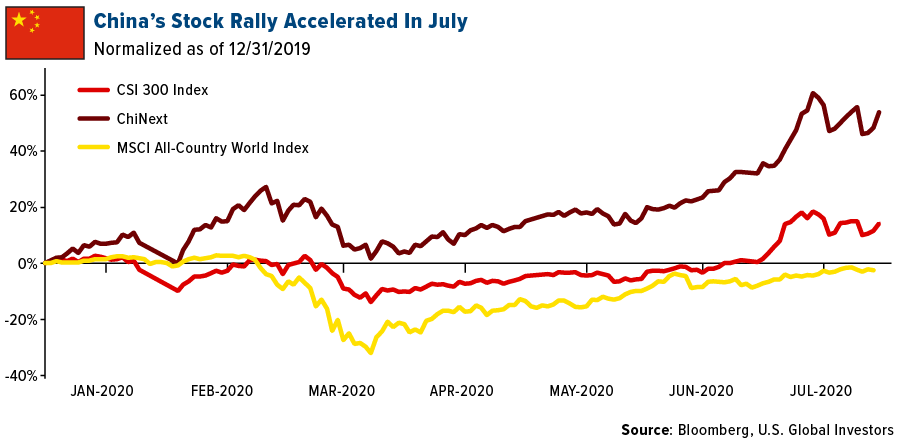

- China is opening hedge funds at its fastest pace since 2015. New fund offerings rose to 1,500 in July after a monthly pace of 1,217 in the first half of the year, reports Bloomberg News. Chinese stocks had a big run in July with the Shanghai Composite Index rising 10 percent. Bloomberg notes that its performance beat all but two of the world’s 92 other equity benchmarks.

- Despite rising U.S.-China tensions, the market has remained relatively stable due in part to the phase one trade deal. China pledged to buy an additional $200 billion worth of American farm goods by the end of 2021, adding positive sentiment.

Threats

- Hong Kong’ economy contracted 9 percent in the second quarter for a fourth straight quarterly contraction. The figure was worse than expectations of an 8.3 percent drop. The government said with the GDP release that “the recent surge in Covid-19 cases has clouded the near-term outlook for domestic economic activity.”

- Tensions continue to heat up between India and China along its border. India is adding 35,000 additional troops along the disputed Himalayan border. This follows a dispute on June 15 that resulted in 20 Indian soldiers and an unknown number of Chinese soldiers killed.

- The EU imposed sanctions on China over its treatment of Hong Kong security laws. The sanctions include limiting exports of equipment China could use for repression and reassessing extradition arrangements, the Wall Street Journal reports. A spokesman for the Chinese mission to the EU told the bloc to “stop meddling in Hong Kong affairs and China’s internal affairs in any way.”

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended July 31 was Spendcoin, up 711.50 percent.

- At the start of the week the price of bitcoin pushed through the $11,000 level in a high-volume surge, reports CoinTelegraph, which saw the price reach a new 2020 high at $11,394.

- On Thursday, the dollar dropped to its lowest level since May 2018 as the Federal Reserve said it plans to keep interest rates close to zero, and inflation hedges continue to show strength, writes CoinTelegraph. As the dollar weakens, however, both gold and bitcoin appear to be soaring. Bitcoin had been stuck in a tight trading range for over two months, but as mentioned above, broke above $11,400 on Tuesday, following the rally in precious metals.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week ended July 31 was Seele-N, down 86.99 percent.

- Wirecard, a controversial German payments processor and issuer of several crypto debit cards, has been implicated in a new report on alleged criminal activities by a Mastercard executive operating at the troubled FBME bank in Cyprus, writes CoinTelegraph. In the latest chapter of the saga at FBME, the unnamed Mastercard exec. Has been accused of a money laundering cover-up using a system of “phantom transactions” designed to thwart detection by Visa and Mastercard’s anti-fraud and money-laundering checks.

- Bitcoin could very well register its best July price performance for eight years, writes CoinDesk, confirming a major bullish breakout in the process. The popular digital currency is up nearly 22 percent this month, and just needs to hold above $11,145 until today’s close to confirm the biggest gain since July 2012, when prices rallied by 40 percent.

Opportunities

- Max Keiser of the Keiser Report says that bitcoin will not stop rising until it hits $28,000, reports CoinTelegraph, as the largest cryptocurrency gains over 20 percent in a week. In a series of tweets on July 27, Keiser forecast that BTC/USD is heading for six figures after a correction period near $30,000.

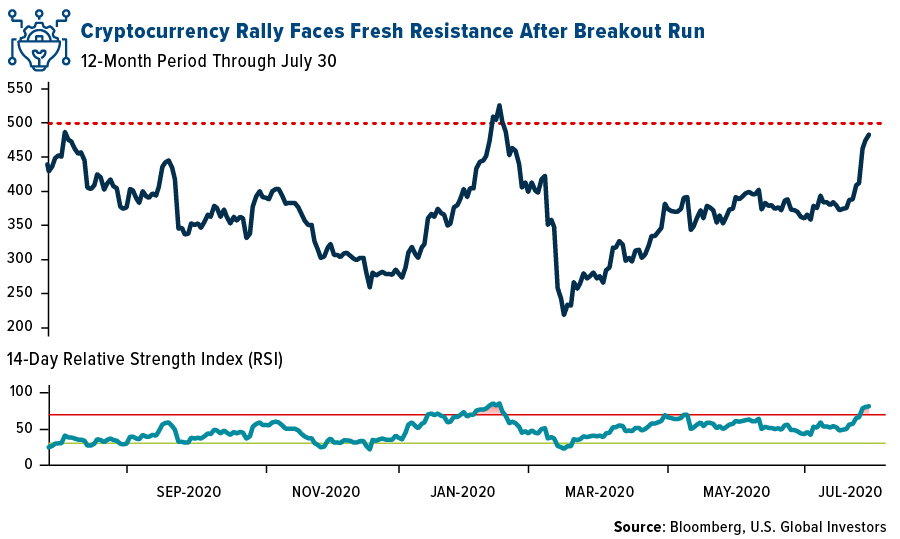

- An index of the top cryptocurrencies is set to reface a psychologically important resistance level that’s checked its rise in the past. The Bloomberg Galaxy Crypto Index, which measures the largest digital coins that trade in U.S. dollars, has surged close to 35 percent in July alone, as of the 30th, and is roughly 15 index points away from meeting resistance at the 500 level. The 14-day relative strength index (RSI) appears overextended. If the group can exceed the 500 threshold, the next test may be 600.

- Iran has announced that it will now allow industrial-scale power plants in the country to operate as bitcoin miners, reports CoinTelegraph, provided they don’t use subsidized fuel and as long as they “comply with approved tariffs.”

Threats

- A state-backed blockchain infrastructure project from China hopes to be the dominant internet services provider for decentralized applications (dapps), writes CoinDesk. Even though the first-mover advantage is significant, geopolitical risks are real, particularly as U.S.-China relations become increasingly tense. The project called the Blockchain-based Service Network (BSN) is a Chinese state-sanctioned blockchain project, but few may realize the network is supported by U.S. technology companies.

- The Security Service of Ukraine (SSU) detained terrorists who demanded bitcoin in return for not blowing up buildings in the country’s capital, writes CoinDesk. A post on SSU’s Facebook profile detailed two 60-year-old men who posted a paper note on an apartment building in Kyiv threatening to blow up that building or another one if they did not receive 50 BTC to their bitcoin address. The alleged terrorists even detonated a small bomb near a subway station to prove they were serious.

- One of the largest scams in the cryptocurrency industry known as PlusToken is taking another twist as dozens of major suspects have been arrested, reports CoinTelegraph. According to a July 30 report by local industry publication ChainNews, as many as 27 core PlusToken team members have been arrested by Chinese police. The total amount of losses in the scam is estimated at 40 billion Chinese yuan, or $5.7 billion.

Leaders and Laggards

| Index | Close | Weekly Change($) |

Weekly Change(%) |

|---|---|---|---|

| 10-Yr Treasury Bond | 0.54 | -0.04 | -6.91% |

| Oil Futures | 40.43 | -0.64 | -1.56% |

| Hang Seng Composite Index | 3,725.70 | -83.55 | -2.19% |

| S&P Basic Materials | 379.77 | -8.25 | -2.13% |

| Korean KOSPI Index | 2,249.37 | +33.18 | +1.50% |

| S&P Energy | 272.09 | -13.70 | -4.79% |

| Nasdaq | 10,745.27 | +283.85 | +2.71% |

| DJIA | 26,428.32 | -224.01 | -0.84% |

| Russell 2000 | 1,478.07 | -12.13 | -0.81% |

| S&P 500 | 3,265.80 | +30.14 | +0.93% |

| Gold Futures | 1,992.40 | +75.00 | +3.91% |

| XAU | 154.53 | +8.05 | +5.50% |

| S&P/TSX VENTURE COMP IDX | 721.66 | +41.46 | +6.10% |

| S&P/TSX Global Gold Index | 397.30 | +21.80 | +5.81% |

| Natural Gas Futures | 1.80 | +0.02 | +1.06% |

| Index | Close | Monthly Change($) |

Monthly Change(%) |

|---|---|---|---|

| Korean KOSPI Index | 2,249.37 | +142.67 | +6.77% |

| 10-Yr Treasury Bond | 0.54 | -0.14 | -20.38% |

| Gold Futures | 1,992.40 | +190.50 | +10.57% |

| S&P Basic Materials | 379.77 | +24.25 | +6.82% |

| S&P 500 | 3,265.80 | +149.94 | +4.81% |

| DJIA | 26,428.32 | +693.35 | +2.69% |

| Nasdaq | 10,745.27 | +590.64 | +5.82% |

| Oil Futures | 40.43 | +0.61 | +1.53% |

| Hang Seng Composite Index | 3,725.70 | +164.83 | +4.63% |

| S&P/TSX Global Gold Index | 397.30 | +51.35 | +14.84% |

| XAU | 154.53 | +25.85 | +20.09% |

| Russell 2000 | 1,478.07 | +50.76 | +3.56% |

| S&P Energy | 272.09 | -8.21 | -2.93% |

| S&P/TSX VENTURE COMP IDX | 721.66 | +101.53 | +16.37% |

| Natural Gas Futures | 1.80 | +0.13 | +7.96% |

| Index | Close | Quarterly Change($) |

Quarterly Change(%) |

|---|---|---|---|

| XAU | 154.53 | +40.85 | +35.93% |

| S&P/TSX Global Gold Index | 397.30 | +70.39 | +21.53% |

| Gold Futures | 1,992.40 | +287.50 | +16.86% |

| DJIA | 26,428.32 | +2,082.60 | +8.55% |

| S&P 500 | 3,265.80 | +353.37 | +12.13% |

| Nasdaq | 10,745.27 | +1,855.72 | +20.88% |

| Korean KOSPI Index | 2,249.37 | +301.81 | +15.50% |

| Natural Gas Futures | 1.80 | -0.15 | -7.44% |

| S&P Basic Materials | 379.77 | +53.22 | +16.30% |

| Russell 2000 | 1,478.07 | +167.41 | +12.77% |

| Oil Futures | 40.43 | +21.59 | +114.60% |

| Hang Seng Composite Index | 3,725.70 | +277.11 | +8.04% |

| S&P/TSX VENTURE COMP IDX | 721.66 | +249.92 | +52.98% |

| S&P Energy | 272.09 | -17.56 | -6.06% |

| 10-Yr Treasury Bond | 0.54 | -0.10 | -15.78% |

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission ("SEC"). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (06/30/2020):

Sberbank

Polyus

TOTAL SA

Barrick Gold Corp

AngloGold Ashanti Ltd

Amazon.com Inc.

BHP Group Ltd

Yamana Gold Inc

Sandstorm Gold Ltd

Dundee Precious Metals Inc

Franco-Nevada Corp

Ivanhoe Mines Ltd

K92 Mining

MMC Norilsk Nickel PJSC

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment. The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index. The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges. The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The Shanghai Stock Exchange Composite Index is a capitalization-weighted index. The index tracks the daily price performance of all A-shares and B-shares listed on the Shanghai Stock Exchange. The CSI 300 is a capitalization-weighted stock market index designed to replicate the performance of the top 300 stocks traded on the Shanghai Stock Exchange and the Shenzhen Stock Exchange. The MSCI ACWI Index, MSCI’s flagship global equity index, is designed to represent performance of the full opportunity set of large- and mid-cap stocks across 23 developed and 26 emerging markets. The WilderHill New Energy Global Innovation Index (NEX) captures solutions to climate change and is composed of companies worldwide whose innovative technologies focus on clean energy, low CO2 renewables, conservation and efficiency. The NYSE Arca Gold BUGS Index is a modified equal dollar weighted index of companies involved in gold mining. BUGS stands for Basket of Unhedged Gold Stocks. It is also referred to by its ticker symbol "HUI". The Solactive Global Silver Miners Index includes international companies active in exploration, mining and/or refining of silver. The index includes a minimum of 20 and a maximum of 40 members which are weighted according to freefloat market capitalization. The calculation is done in USD as a total return index. Index adjustments are carried out semi-annually. The Bloomberg Billionaires Index is a daily ranking of the world’s 500 richest people. The figures are updated at the close of every trading day in New York. The Solactive Global Copper Miners Index includes international companies active in exploration, mining and/or refining of copper. The index includes a minimum of 20 and a maximum of 40 members. The IBD 50 Index tracks the performance of stocks listed in the IBD 50, a proprietary list of the 50 top-ranked companies updated and published daily in Investor’s Business Daily. Companies are ranked based on superior earnings, strong price performance, and leadership within their respective industries.