Frank Talk

How Lower Rates and Central Bank Demand Are Fueling the Gold Rally

Date Posted: March 25, 2024

Read time: 5 min

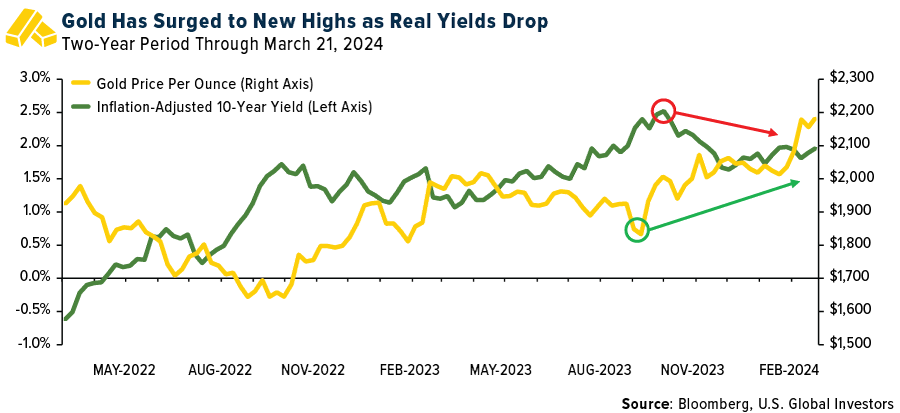

Gold staged a blinding comeback last week, surging to fresh all-time highs above $2,200 an ounce. The rally, which has added around 10% to gold’s value since mid-February, caught many market watchers off-guard. But for those of us who’ve stuck with the yellow metal through its ups and downs, the price action is the vindicating result of several powerful forces aligning in bullion’s favor.

At the heart of gold’s resurgence is the Federal Reserve’s signal that it may be ready to throw in the towel. Fed Chair Jerome Powell has made it clear that the central bank is on course to cut rates as many as three times in 2024, fueling hopes that the tight monetary policy of the past 18 months is nearing an end.

With rate cuts on the horizon, real yields have cooled, increasing the relative attractiveness of non-interest-bearing gold.

Traders have wasted little time pricing in the Fed’s dovish stance. Futures markets now see a 72% chance of a rate cut as soon as June, up from 65% before the Fed meeting. Against this backdrop, gold’s surge is, I believe, textbook price action.

Central Banks’ Insatiable Appetite for Gold Fueling the Rally

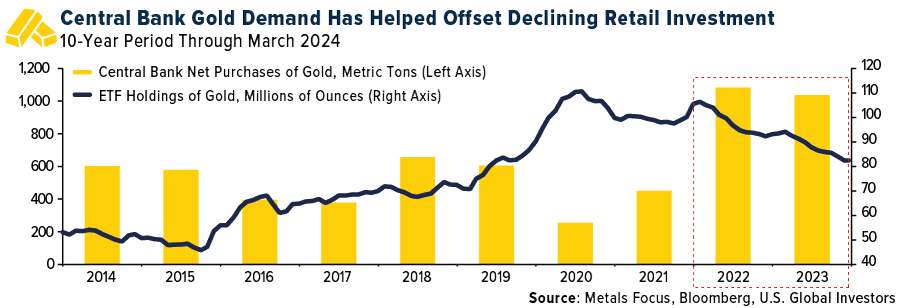

There’s more to the rally than just lower rates and a weaker U.S. dollar. As many of you are aware, central bank demand for gold has been a powerful driver as more and more developing countries join the de-dollarization movement in response to Western sanctions on Russia.

China has led the charge here, consistently adding large amounts of gold to its reserves for the past 16 months straight. Overall central bank buying reached record highs in 2022 and has shown no signs of slowing, helping to offset the selling pressure caused by gold-backed ETFs.

Soaring Gold Prices Tarnish Luxury Jewelry Demand

Higher gold prices have significant implications for the luxury goods market, where the precious metal is a key input cost for jewelry and watch manufacturers. Specifically, the 14% surge in gold prices since last fall appears to be crimping demand.

In China, the world’s largest buyer of gold jewelry, retail sales in the luxury category rose just 5% year-over-year in the first two months of 2024 despite the reopening boom, according to Bloomberg Intelligence. This could be worrying for luxury conglomerates like Richemont and LVMH, which were counting on a strong Chinese bounce-back to drive sales higher.

The pressure is particularly intense for retailers like Chow Tai Fook, the world’s second-largest jewelry chain after Richemont-owned Cartier. In its latest quarterly report, Chow Tai Fook said non-gold jewelry sales at its stores in mainland China slid 2% compared to last year due to “weak sentiment,” write Bloomberg Intelligence’s Catherine Lim and Trini Tan. With gold trading near 30-year highs in yuan terms, the outlook for jewelry demand in China appears challenging unless prices moderate.

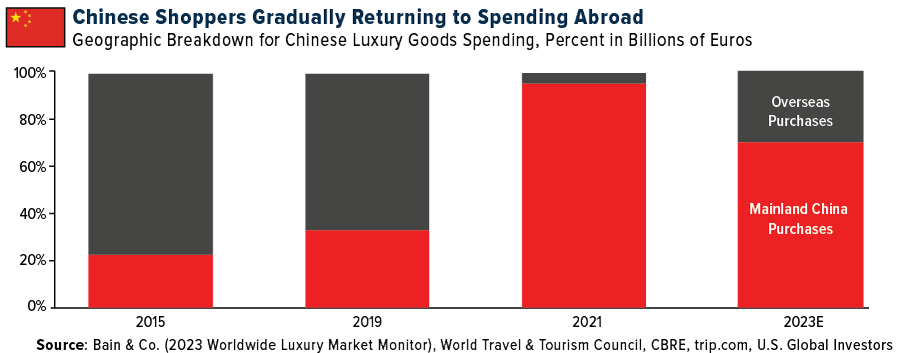

Wealthy Chinese Back to Spending Abroad, With Room for Improvement

The picture isn’t all bleak for luxury brands. While the appetite for gold trinkets may be suppressed right now due to high metal prices, overall luxury spending by Chinese consumers rebounded strongly in 2023 as the country emerged from Covid lockdowns. According to research firm Bain & Company, Chinese luxury purchases within mainland China recovered to an estimated 70% of pre-pandemic levels last year, with tourism spending in Europe and Asia also witnessing a comeback.

Looking ahead, Bain projects mid-single-digit growth for China’s luxury market in 2024, supported by the nation’s still-robust fundamentals for high-end consumption. A lot will depend on how issues like China’s property sector crisis and consumer confidence play out in the coming months.

Regardless of any near-term volatility, China’s increasingly wealthy middle class will continue driving demand for luxury goods and services.

For investors, I believe the recipe is clear: Consider allocating 10% of your portfolio to physical gold and high-quality gold mining stocks. The same fundamentals that have revived gold’s current bull market—lower real rates, central bank buying, safe-haven appeal—could remain in place in the months and years ahead.

Watch our latest video on gold’s love trade by clicking here!

Past performance does not guarantee future results. All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor. By clicking the link(s) above, you will be directed to a third-party website(s). U.S. Global Investors does not endorse all information supplied by this/these website(s) and is not responsible for its/their content.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (12/31/2023): Cie Financiere Richemont SA, LVMH Moet Hennessy Louis Vuitton SA.