Investor Alert

Gold Has Been One of the Few Bright Spots in 2022 (So Far)

Date Posted: June 17, 2022

Read time: 42 min

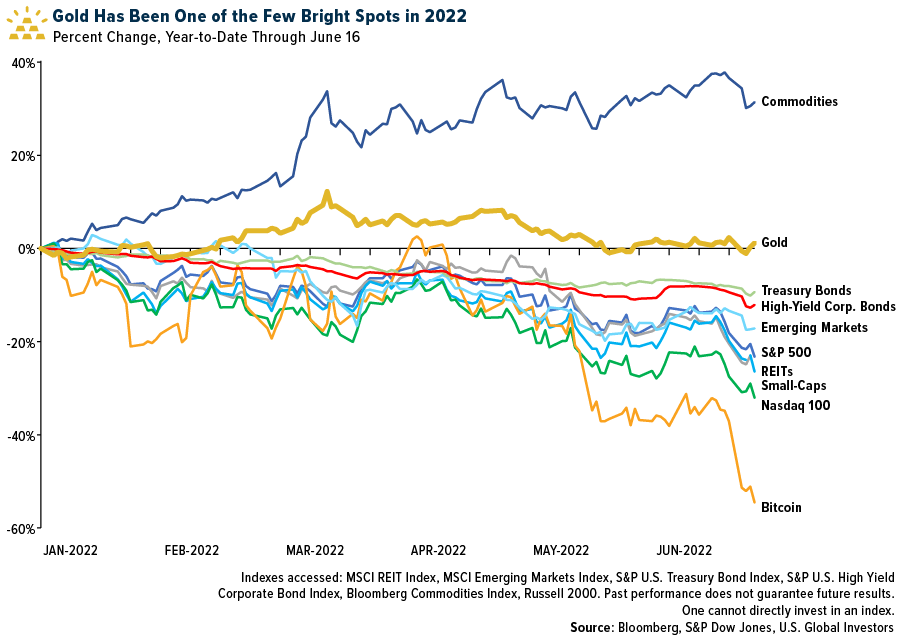

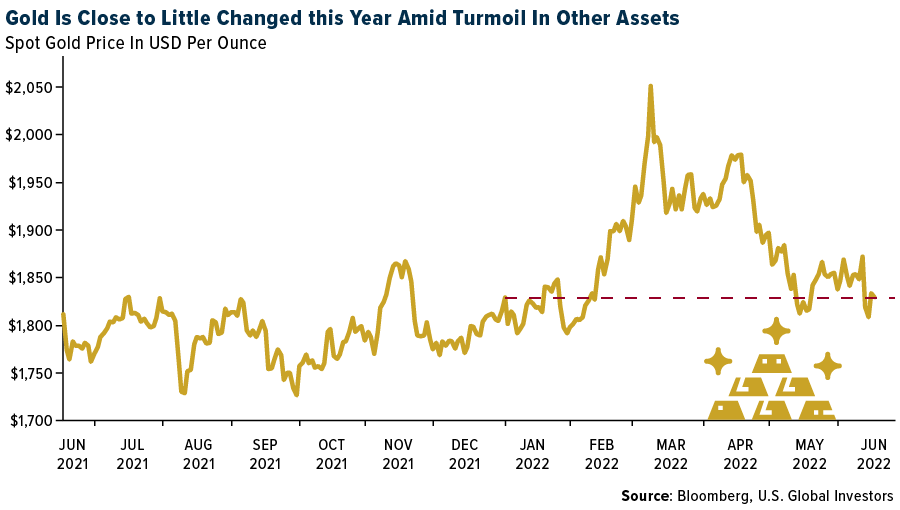

We’re almost halfway through 2022, and so far gold has been the big winner after oil, coal and other commodities.

We’re almost halfway through 2022, and so far gold has been the big winner after oil, coal and other commodities. The yellow metal has managed to stay positive since the start of the year, skirting pressure from surging yields and a strong U.S. dollar. Meanwhile, nearly every other asset class—from large-cap and small-cap equities to bonds, from real estate investment trusts (REITs) to cryptocurrencies—has fallen into either correction or bear market territory.

I believe this shows that gold has retained its perceived role as a store of value during times of decades-high inflation and economic and geopolitical uncertainty. As I often say, investing in gold won’t make you a billionaire, but it could help stabilize your portfolio when everything else is crashing.

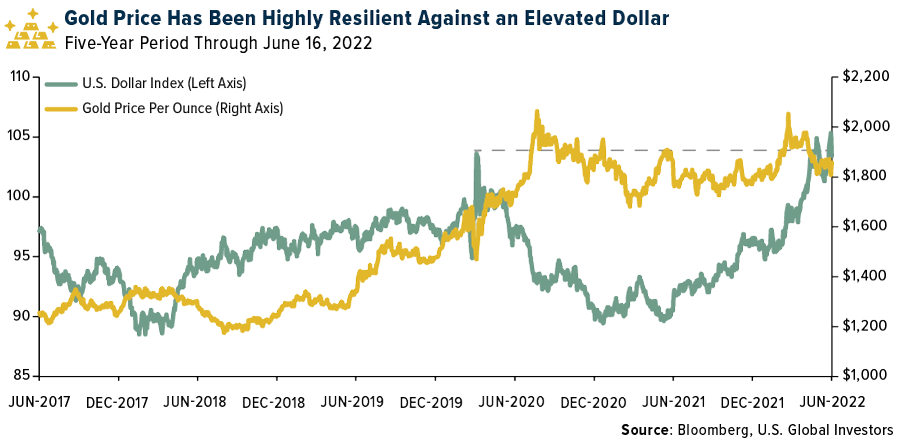

Dollar at 20-Year Highs

I’m most impressed that gold has stayed afloat even as the U.S. dollar has strengthened to 20-year highs against a basket of other major currencies. Since gold is priced in dollars, the two assets have historically shared an inverse relationship, with one falling when the other rises, and vice versa. At the beginning of the pandemic, the dollar spiked as investors sought a safe haven, which put pressure on gold. The value of the dollar is now highly elevated on the back of interest rate hikes, and yet the yellow metal has continued to trade above $1,800 an ounce.

It’s for this reason, among others, that I agree with Newmont CEO Tom Palmer, who said this week that gold’s floor price has likely increased from previous support of around $1,200 to between $1,500 and $1,600 currently.

While I’m on this topic, a stronger dollar is mixed news. On the one hand, it can help limit the effects of inflation by offsetting the price of imports. On the other hand, it makes U.S. exports more expensive to overseas buyers. We’ll likely see lower fourth-quarter earnings for companies with international exposure as a result. Earlier this month, Microsoft joined Coca-Cola, Procter & Gamble and a host of other multinational U.S. companies in cutting forecasts for the remainder of the year due to a stronger greenback.

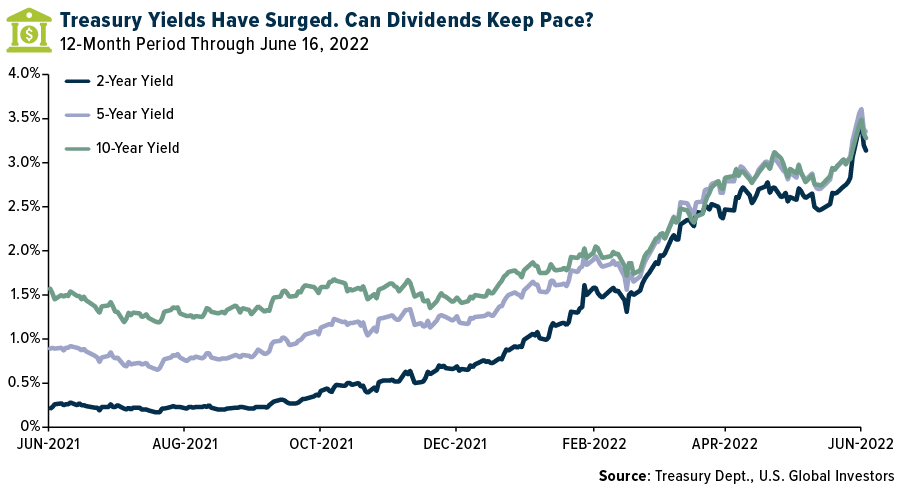

Will S&P 500 Companies Raise Their Dividends to Compete with Treasury Yields?

As I mentioned earlier, government bonds have steadily sold off this year, pushing yields to multiyear highs. The two-year yield was trading as high as 3.45% this week, a substantial increase from 0.78% at the start of the year.

This may attract yield-seeking investors, but I urge them to keep in mind that inflation is running at an annual rate of 8.6%. That means they’re effectively paying the government for the privilege of holding its debt.

At the same time, dividend investors may have a hard time selecting stocks that pay out at a competitive rate. As of this month, the S&P 500 has a dividend yield of only 1.68%, up slightly from the beginning of 2022 but down from June 2020, when it was closer to 2.0%.

It’s well known that gold doesn’t pay any income, but with stocks and bonds out of favor, the metal may be a better bet to potentially keep ahead of inflation right now.

Want to learn more about gold and inflation? Watch our YouTube video by clicking here!

Index Summary

- The major market indices finished down this week. The Dow Jones Industrial Average lost 4.79%. The S&P 500 Stock Index fell 5.70%, while the Nasdaq Composite fell 4.78%. The Russell 2000 small capitalization index lost 7.44% this week.

- The Hang Seng Composite lost 3.48% this week; while Taiwan was down 14.15% and the KOSPI fell 18.02%.

- The 10-year Treasury bond yield rose 7 basis points to 3.23%.

Airline Sector

Strengths

- The best performing airline stock for the week was Boeing, up 8.2%. Evercore ISI has been tracking traffic to airline websites since May of 2020 as a proxy for demand recovery in the industry. May monthly web traffic for U.S. airlines was up 51% versus 2019 baseline and versus up 46% in April and higher by 48% in March. For the week, U.S. airline industry web traffic was 41% higher year-over-year versus a 44% increase last week.

- The International Air Transport Association (IATA) this week released passenger data for April 2022 highlighting the continuing recovery in air travel driven by international demand. In April, international travel was down 43% year-over-year versus 2019.

- The Evercore ISI Airlines Survey moved up for a second straight week, increasing from 66.3 to 67.5. The survey has steadily climbed, rising in 17 of the past 21 weeks, and is currently at its highest level since July 2012.

Weaknesses

- The worst performing airline stock for the week was Air France, down 21.0%. Wizz Air expects operating losses to continue in the first fiscal quarter of 2023 (June-end) driven by higher fuel costs and operational disruptions. Shares were down by 10% at market close, potentially from the disappointing guidance and concerns around a capital raise. Consensus may move down following the guidance.

- Cancellation rates have sharply increased at Air Canada but remain subdued at WestJet, reflecting labor constraints in Toronto (to which Air Canada has greater exposure). In Europe, cancellation rates are sharply increasing at easyJet, Air France-KLM, Lufthansa, and Wizz Air, while rates at Ryanair and IAG remain subdued.

- Passengers faced severe delays and flight cancellations over the holidays, especially in the U.K. Staff shortages at airlines, airports and ground-handling companies in the U.K. have contributed to 500 flight cancellations over the Jubilee weekend, as per media reports. The CEO of Heathrow Airport thinks it could take 18 months for operational capacity to return.

Opportunities

- According to Cowen, pre-departure testing is being eliminated as of Sunday, June 12. Cowen expects demand for international travel to pick up as the uncertainty for U.S. citizens is removed. In January, U.S. citizen international visitor departures increased 69% versus January 2021 but was down 38% compared to January 2019. February outbound volume was up 112% versus February 2021 but was down 33% versus February 2019. March 2022 international outbound travel volume was up 98% versus March of the year prior but was down 30% when compared to March 2019.

- Wizz Air has reinstated its jet fuel hedging policy, reversing a decision last year to move toward “no hedging.” This removes some of the uncertainty that has surrounded Wizz recently, and should be taken positively for two reasons: 1) The new jet fuel price caps put in place for the second half of the year through March 2023 estimates, will limit the exposure to further volatility in the oil price and provide some protection against any near-term spikes, and 2) Putting hedging in place from year end through March 2024 estimates to align itself more closely with peers “levels the playing field” looking out, and removes the issue of fuel as a differentiator versus peers.

- JPMorgan believes a merger outcome between Spirit Airlines and JetBlue is a growing probability and may overtake the likelihood of a Frontier deal. More importantly, Spirit shares are trading in line with the proposed Frontier offer, and – owing to the break fee – slightly below what Spirit shareholders would receive if the DOJ were to block the transaction today, holding current share prices constant. In their mind, this largely insulates Spirit shares from any material downside owing to fundamentals, at least in the near term.

Threats

- Starting July 1, airline passengers departing Hungary will be subject to a new tax levy worth Euro10-25 per passenger. Passenger surcharges are not a new phenomenon and are common across the aviation sector; the main threat to airlines is through a potential destruction of consumer demand. With LCC average ticket fares at Euro 30-40 per passenger, the surcharge could add up to 25% to ticket prices.

- U.S. airlines’ trailing seven-day website visits decelerated this week to up 10% versus 2019, compared to up 14% last week. American Airlines’ website visits stepped back to +23% versus 2019 from +28% last week. Southwest’s website traffic also decelerated to up 6% versus 2019 (from up 12% last week), but the carrier recently announced its fall sale, which runs from June 7 to June 9, meaning visitation will likely jump next week.

- According to Cowen, published fares (not selling fares, which are demand based and lower) are up 32.9% year-over-year but down 3.1% this week to $333. Passenger demand is down 13% versus 2019 in June month-to-date, per TSA throughput, which is resulting in slightly erratic fare trends. From a macro perspective, however, travelers continue to fly.

Emerging Markets

Strengths

- The best performing country in emerging Europe for the week was Russia, gaining 3.0% The best performing country in Asia this week was China, via the Shanghai Stock Exchange, gaining 0.3%.

- The Russian ruble was the best performing currency in emerging Europe this week, gaining 2.3%. The Indian rupee was the best performing currency in Asia this week, gaining 0.3%.

- China´s industrial production rose mildly to 0.70% in May from a year ago, and from -2.90% in April. The consensus was -0.90%. Despite the improvement in economic numbers, China’s National Bureau of Statics warned that difficulties and challenges still remain, reports CNBC.

Weaknesses

- The worst performing country in emerging Europe for the week was Poland, losing 3.1%. The worst performing country in Asia this week was South Korea, losing 6.9%.

- The Polish zloty was the worst performing currency in emerging Europe this week, losing 1.7%. The Pakistani rupee was the worst performing currency in Asia this week, losing 3.2%.

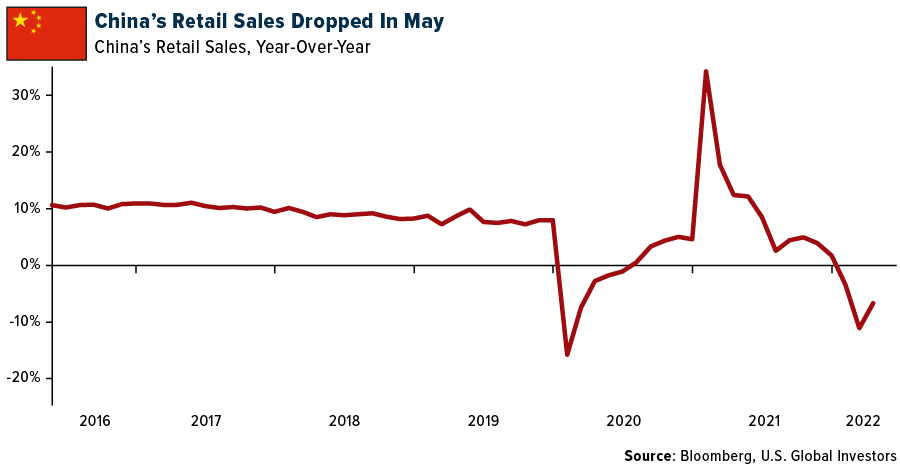

- China’s retail sales in May fell less than expected, down by 6.70% versus the consensus of a 7.10% drop. Even though the data came in better than forecast, it remains in negative territory.

Opportunities

- In a note to clients this week, analysts at Goldman Sachs told investors to keep an eye on emerging markets. “Weak U.S. dollar cycles tend to bode positively for emerging-market assets,” the note reads. The analysts also explained the appeal of the MSCI China Index and early cycle emerging markets in Southeast Asia, reports ETF Database. Goldman strategist Zach Pandl added that he sees the yen outperforming as well, as U.S. recession risks rise.

- According to FactSet, despite rising inflation, the People’s Bank of China (PBOC) decided to leave rates unchanged at 2.85%. This indicates that inflation in the Asian nation is not as bad as across other emerging markets and is an excellent way to stimulate the economy. Historically, people will consume more because their buyer power is not impacted.

- According to Reuters, China and the U.S. have made an important step to improve their bilateral relationship, that is now more crucial than ever. In a meeting between U.S. Defense Chief Lloyd Austin and Chinese Defense Minister Wei Fenghe, the two defined clear lines of communication while respecting one another’s internal affairs. The representatives also discussed instability in the Taiwan Strait, with the U.S. making its support of Taiwan clear. This approach will surely impact the market, fostering a feeling of security for investors.

Threats

- According to FactSet and an article from the Wall Street Journal, U.S. Congress is working on new legislation to limit U.S. investment in China. The project would provide new powers to the government to restrict transactions in countries like China considered adversaries, rebuild critical supply chains, and remain competitive in global markets. The new legislation could be seen by China and other key players as a threat, potentially generating tensions that would be reflected across markets.

- Based on a survey by the American Chamber of Commerce, only 31% of the 130 U.S. manufacturing and services companies operating in the region are now operating at 100% capacity following the end of the Shanghai lockdowns. Many local workers reportedly find it difficult to get to work. Since China is one of the world’s leading producers, this could represent a slowdown in the global economy, with additional shortages and delays in the supply chain.

- When it comes to the global economy, new lockdowns could prove detrimental to worldwide supply chains, also reflected in higher inflation levels. According to FactSet, Hong Kong reported an elevated number of positive Covid cases for the first time in two months. This represents a considerable risk that China, based on its Zero-Covid policy, could lock down the country again.

Energy & Natural Resources

Strengths

- The best performing commodity for the week was lumber, up 4.86%, on what could be a bear market rally. Against that backdrop, housing starts dropped 14.4% in May and the average 30-year fixed rate mortgage has now climbed to 5.65%, the highest since 2008. Lumber is down 60% since March.

- According to Baker Hughes, the U.S. rig count increased by six this week to 733, with the land rig count up by seven to 718. The offshore rig count came down by one to 15.

- India’s fuel consumption has increased by 24% year-over-year to 18.269 million tons in May 2022. According to data from the Indian oil ministry’s Petroleum Planning and Analysis group, the increase is due in part to a relatively lower base in 2021 amid a high count of Covid cases. Last month was the biggest year-on-year jump since April of 2021.

Weaknesses

- The worst performing commodity for the week was natural gas, down 20.58%. Freeport LNG, one of the largest U.S. operators of LNG export terminals, on Tuesday said that damage from last week’s fire at its Texas plant would keep it fully offline until September, reports Reuters, with only partial operation through year end. Natural gas prices slumped in the United States and soared in Europe on news of an extended shutdown.

- Tin suffered a second day of heavy selling in London as surging inflation and the rising risk of recession in major economies threatens to put an end to a long-running boom in demand from the electronics sector. Prices for the soldering metal fell as much as 7.6% on the London Metal Exchange, extending Monday’s 6.7% drop.

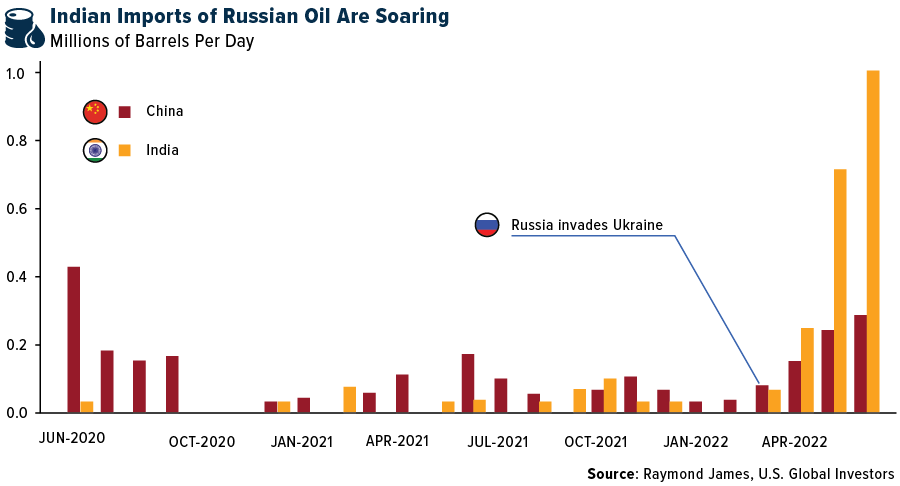

- European gas prices surged 50% this week as Moscow tightened its squeeze on crucial gas flows to the continent, forcing Europe to pull gas from winter storage to confront the prospect of keeping their economies running without Russian gas. On a related note, the Biden administration’s leading international energy adviser has called on India to not go “too far” when increasing imports of discounted Russian crude that has lost buyers in Europe. Indian purchases of seaborne Russian oil have surged as exporters slash prices for Urals, the country’s main crude export stream, after European refineries began shunning the cargoes and the EU moved to end its dependence on Russian energy following the invasion of Ukraine.

Opportunities

- JPMorgan expects that tight stocks and low inventories will be a recipe for higher commodity prices. Oil could top $150 per barrel in the short-term, while other crops such as corn could top $13 a bushel. Both Russia and China have reduced refining capacity while the active Atlantic hurricane season could threaten Gulf of Mexico refiners. Diesel fuel remains in tight supply with the transportation sector making a comeback.

- After a yearslong deadlock, Ecuador and Chile have resumed negotiations over a partnership to develop a major copper deposit, reports Bloomberg, just as demand for the wiring metal is set to surge in a nascent clean-energy transition. Chile’s state copper producer Codelco agreed to a request by its Ecuadorian counterpart Enami to suspend two arbitration processes over the Llurimagua copper-molybdenum exploration project in the Andean region of Imbabura, Ecuador Energy and Mines Minister Xavier Vera said. “That suspension generated positive conditions for talks,” Vera commented.

- A top Brazilian mining official expects his country to attract a wave of investment in copper, nickel and lithium in the coming years as streamlined rules and practices improve access to rich deposits of the battery metals. Brazil, the biggest iron ore producer after Australia, is looking to lure more exploration and development in minerals key to the clean energy transformation. In order to do that, the government is overhauling geological information, opening inactive areas, and working on indigenous consultation processes, said Pedro Paulo Dias Mesquita, secretary of geology, mining and mineral transformation at Brazil’s Ministry of Mines and Energy.

Threats

- According to UBS, iron ore prices have recovered from a low of $87 per ton in November 2021 to trade in a range of $120-160 per ton in 2022. The recovery is driven by improving fundamentals with iron ore demand, supply struggling and inventories falling. This is supported by an expectation that China steel demand will pick up post-lockdown supported by stimulus. UBS expects prices to fall back in 2023-24 to the 90th percentile of the value-in-use curve or $70-80 per ton as supply normalizes and demand moderates. UBS also expects the iron ore market to be broadly balanced in 2022 and move into a growing surplus in 2024.

- The Energy Information Administration (EIA) forecasts U.S. refinery utilization to average 94% in the third quarter of 2022 given high wholesale product margins, at or near their highest levels in the past five years. However, operable refinery capacity is 900 million barrels per day lower than the end of 2019, suggesting that total refinery output of products is unlikely to reach its highest level in the past five years, although still impactful in helping moderate wholesale margins down from record levels.

- Goldman made headlines when it warned that a searing rally in lithium will go into reverse this year as supply from unconventional new sources overwhelms demand. Credit Suisse Group AG also joined in predicting a correction. However, other specialists including London-based Benchmark Mineral Intelligence are loudly pushing back.

Luxury Goods

Strengths

- Over the past 15 years, Estee Lauder has outperformed the market by 10.76% on an annualized basis, reports Benzinga, producing an average annual return of 17.19%. The American multinational cosmetics company has a market cap of just over $89 billion. If an investor had bought $100 of Estee Lauder stock 15 years ago, it would now be worth $1,083.05 (based on a price of $249.44 for the stock at the time of Benzinga’s analysis).

- The hotel group Ritz-Carlton will launch its first million-dollar luxury mega-yacht in August, after facing years-long delays amid COVID and reports of budgeting issues. The cruise liner will have 149 suites and offer food prepared by a Michelin Star chef. This kind of project reflects that despite high levels of inflation worldwide, companies continue to offer their customers new ways to spend while enjoying unique experiences after two years of lockdowns.

- NIO, a Chinese electric car maker and distributor, was the best performing S&P Global Luxury stock for the week, gaining 14.5%. The American depositary receipts (ADRs) of NIO gained 16% on Tuesday, after the company announced a product launch event happening the very next day.

Weaknesses

- According to Bloomberg, Goldman Sachs downgraded Prada because of low consumer confidence, cutting forecasts for the company. The bank said the risk/reward profile of the stock was no longer attractive as it was before. Hermès International and Salvatore were among the luxury names also downgraded, as a consequence of lockdowns in China as well as supply chain issues.

- Cosmetics company Revlon filed for Chapter 11 bankruptcy protection this week, reports CNBC, as it grappled with a cumbersome debt load and a snarled supply chain. The company expects to receive $575 million in debtor-in-possession financing from its existing lender base, the article continues, which will help to support its day-to-day operations.

- Royal Caribbean Cruises was the worst performing S&P Global Luxury stock for the week, losing 18.47%. Cruise line equites sold off on fears of an economic downturn.

Opportunities

- Luxury brands continue accepting cryptocurrencies as payment to stay attractive to their younger consumer base – many of which who have made money investing in the digital asset space (and can now afford to purchase expensive goods). Following Gucci, Burberry, Prada, and Versace, which already accepted payments in crypto, Farfetch, a luxury goods online marketplace, announced that its VIP clients would soon be able to use cryptocurrencies to make purchases.

- Harlem’s Fashion Row (HFR), the first agency to create a connection between brands and designers of color through collaborations, announced its new partnership with Louis Vuitton (LVMH), reports Bloomberg, looking for a more diverse, equitable, and inclusive fashion industry. LVMH committed its support to discover, mentor, and support new talents, offering multiple platforms and increased visibility.

- Italian automaker Lamborghini launched the luxury limited-edition Aventador LP 780-4 Ultimae Roadster this week in the Indian market. According to a senior company official, Lamborghini expects the super-luxury car segment in India to reach the high levels seen in 2018 and 2019. In India, the current waiting time to get a Lamborghini is between 10-12 months.

Threats

- Despite record high gas prices and a baby formula shortage, TheWeek.com reports that it might be tough for the average American to even think about spending money on something frivolous like a luxury dress or purse. Believe it or not, however, many luxury goods retailers are raising prices in order to protect their brands – making the exclusive items even more exclusive. Despite the everyday consumer being pushed further away from affordability, business owners argue that those who are able to afford such goods are also most likely to be in a position to stomach these higher prices.

- The Federal Reserve hiked interest rates by 0.75%, increasing the borrowing cost as a response to record high inflation levels. As interest rates increase, buying certain goods or services, such as cars and luxury items, becomes even more costly than before.

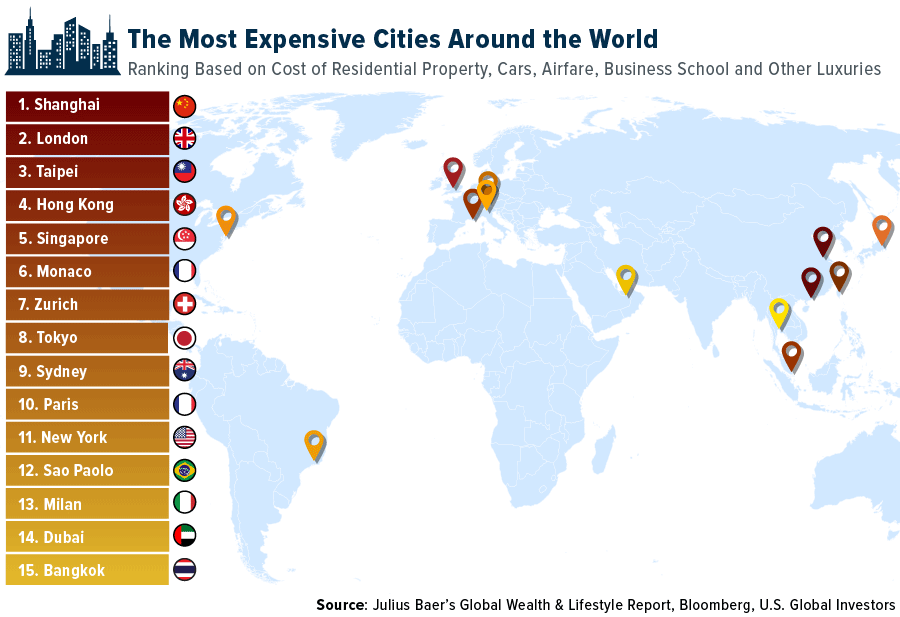

- As a result of high inflation levels globally, 8.6% in the U.S. and 9% in the U.K., (both of which are primary luxury goods markets in addition to China), consumers are losing their purchasing power considerably. Designer clothes, for example, have increased in price by 7.5% globally, according to Bloomberg. Such an increase discourages consumers from buying. The graphic below highlights the most expensive cities to live in currently, based on the cost of residential property, cars, airfare, and other luxuries. With exception of London, many cities in Asia top the list.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performer for the week was Sirin Labs, rising 906.53%.

- The United Kingdom’s digital minister reiterated the government’s ambition to make Britain a global cryptocurrency hub while simultaneously sounding a cautious note about the potential criminal uses of digital assets. “We do intend for the United Kingdom and London to be crypto centers,” Chris Philp said in an interview with Bloomberg Radio on Wednesday.

- The Bank of Israel is working with the Hong Kong Monetary Authority on a trial which will test a new digital currency, including against cyber security risks, the Bank of Israel said. The joint project will start in the third quarter, will use a two-tier central bank digital currency (CBDC), and will be issued by the central bank and then distributed by financial intermediaries like banks, reports Bloomberg.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week was Etherstones, down 100%.

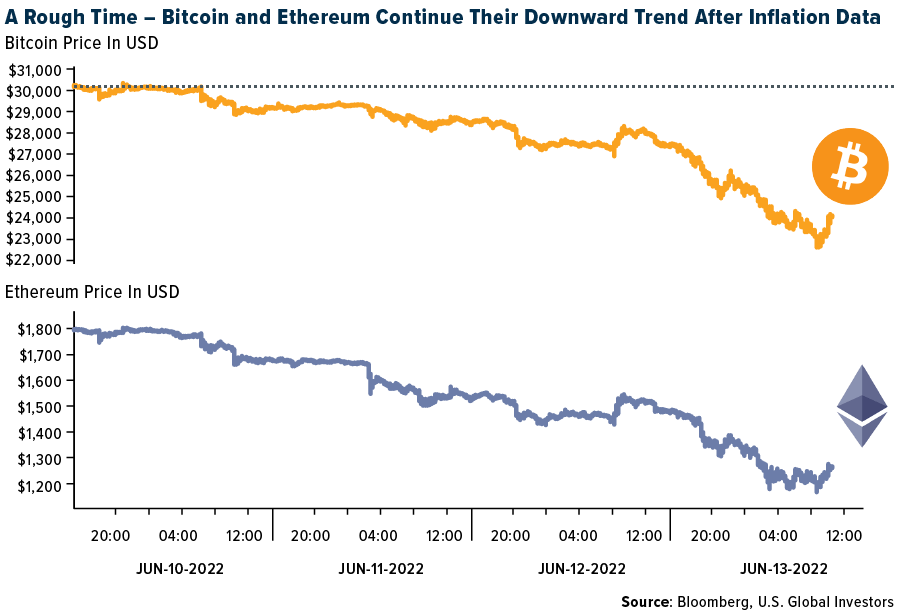

- Bitcoin plunged to the lowest level in about 18 months in Asia trading on Monday as the impact of Friday’s U.S. inflation data continued to reverberate through global risk assets. Traders are boosting bets for a more aggressive pace of Federal Reserve tightening after data on Friday showed U.S. inflation jumped to a fresh 40-year high in May, writes Bloomberg.

- Business intelligence company MicroStrategy Inc., which over the last two years has amassed more than 129,000 Bitcoin tokens, has plunged as much as 23% as the crypto markets fall lower. Cryptocurrency stocks including Marathon Digital Holdings, Riot Blockchain and Coinbase Global Inc. also saw outsized declines of at least 14% each. The MVIS CryptoCompare Digital Assets 100 Index, which measures the 100 largest digital assets, sank as much as 14% this week.

Opportunities

- Changpeng Zhao, co-founder and CEO of Binance, thinks the crypto winter is a great time to increase investment in both talent and acquisitions. “We have a very healthy war chest, we in fact are expanding hiring right now,” Zhao said in a virtual interview during last week’s Consensus 2022 conference. Binance is also looking to increase its investment in other companies, building on efforts such as its $200 million investment in Forbes, which Zhao explains is a strategic move to help drive the adoption of blockchain technology into more sectors, writes Bloomberg.

- Circle Internet Financial is launching a euro-based version of its popular USDC stablecoin, which has been gaining traction after its closest rival Tether has come under increased scrutiny. Euro coin will be available June 30 to institutional customers as a regulated euro-backed stablecoin issued under the same full-reserve model as USDC, reports Bloomberg.

- Goldman Sachs Group has started to trade a type of derivative tied to Ether, as Wall Street investors look for ways to bet on the world’s second-largest cryptocurrency. The bank successfully executed its first trade of Ethereum non-deliverable forwards, a derivative that pays out in cash based on the price of Ether, according to Bloomberg.

Threats

- Celsius Network paused withdrawals, swaps, and transfers after weeks of speculation over the sustainability of the outsized returns being offered by the DeFi lending platform, fueling a broad cryptocurrency selloff, reports Bloomberg. Crypto markets tumbled after the Celsius announcement, with Bitcoin dropping as much as 14% to the lowest level since December 2020 and other major tokens like Ether also falling sharply, the article explains.

- Coinbase Global Inc. announced Tuesday it will lay off 18% of its workforce in another sign of a worsening crypto downturn that’s shaved off hundreds of millions of the total cryptocurrency market value. The biggest crypto exchange in the U.S. is following in the footsteps of other cryptocurrency-related businesses that have recently cut staff, including rival exchange Gemini Trust Co. and lender BlockFi, writes Bloomberg.

- Bitcoin tumbled again this week, driving the token to the brink of $20,000, as evidence of deepening stress within the crypto industry keeps pilling up. There’s a growing sense of anxiety about the stability of crypto projects large and small. Bitcoin fell as much as 8.6% mid-week, resulting in nine straight days of loses, writes Bloomberg.

Gold Market

This week gold futures closed at $1,840.10, down $35.40 per ounce, or 1.89%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 5.80%. The S&P/TSX Venture Index came in off 9.13%. The U.S. Trade-Weighted Dollar rose 0.50%.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Jun-14 | Germany CPI YoY | 7.9% | 7.9% | 7.9% |

| Jun-14 | Germany ZEW Survey Expectations | -26.8 | -28.0 | -34.3 |

| Jun-14 | Germany ZEW Survey Current Situation | -31.5 | -27.6 | -36.5 |

| Jun-14 | PPI Final Demand YoY | 10.9% | 10.8% | 10.9% |

| Jun-14 | China Retail Sales YoY | -7.1% | -6.7% | -11.1% |

| Jun-15 | FOMC Rate Decision (Upper Bound) | 1.50% | 1.75% | 1.00% |

| Jun-16 | Housing Starts | 1,693k | 1,549k | 1,810k |

| Jun-16 | Initial Jobless Claims | 217k | 229k | 232k |

| Jun-17 | Eurozone CPI Core YoY | 3.8% | 3.8% | 3.8% |

| Jun-23 | Initial Jobless Claims | 232k | — | 229k |

| Jun-24 | New Home Sales | 595k | — | 591k |

Strengths

- The best performing precious metal for the week was silver, but still down 1.45%. Tom Palmer, CEO of Newmont Mining, the biggest gold producer, sees a higher floor forming under the gold market as years of stimulus devolve into a fight to contain inflation. Gold has held up much better than cryptocurrencies as the broader markets have pulled back. This week we saw several major crypto firms freeze customer withdrawals.

- Awalé Resources closed a private placement with Newmont Ventures, a wholly-owned subsidiary of Newmont Corporation. Awalé projects are in Côte d’Ivoire and Glen Parson is the CEO. Odienné is the main project and the agreement is staged such that Newmont could earn up to 75% of the project.

- Streaming transactions totaled $1.7 billion in 2021, the strongest year since 2015. The sector has booked $487 million year-to-date compared to $455 million by this time last year. Wheaton Precious Metals has again been the most active with $366 million in streams, followed by Osisko Gold Royalties with $110 million.

Weaknesses

- The worst performing precious metal for the week was palladium, down 6.06%. Sibanye-Stillwater said it has suspended operations at its Montana-based palladium and platinum mines after the area was hit by flooding that washed away access roads and bridges. The Johannesburg-based precious metals producer was forced to evacuate some workers from the Stillwater and East Boulder mines and will wait for the waters to subside before conducting an assessment, spokesman James Wellsted said by phone.

- Gold futures continue to consolidate in a bearish pattern as the precious metal is caught between a broad risk-off and strong dollar flow. There may be an eventual resumption of the medium-term downtrend if the market continues to trade below $1,889-$1,899 and $1,917-$1,927 resistance layers. Broader range support remains near $1,700.

- Cost inflation continues to be a key theme for precious metals producers, and against that backdrop, the royalty names as a group outperformed in 2021, (down 4% on average versus the producers down 13% and gold 4%). So far in 2022, the royalty sector is down 2% on average against a flat gold price (up 1%), and while slightly lagging the senior producers they are outperforming the intermediate and junior gold producers, down 12% and 19%, respectively.

Opportunities

- Gold held much of its biggest gain in more than three months, reports Bloomberg, as shifting expectations of the speed of the Federal Reserve tightening helps the yellow metal rediscover its role as the ultimate haven asset. The resilience of bullion as the Fed announced its biggest interest-rate increase since 1994 is reminding investors of gold’s appeal, the article continues.

- Gold Fields has agreed to acquire Canada’s Yamana Gold for around $7 billion, reports Bloomberg. The deal provides greater geographic diversification but material EPS dilution. Under the terms of the agreed offer, 100% of Yamana outstanding shares will be purchased at a ratio of 0.6 of an ordinary Gold Fields share, valuing Yamana at $6.7 billion. The transaction is expected to close in the second half of the year. Yamana’s board has agreed to back the deal, which will require approval from both sets of shareholders.

- Orla Mining will acquire all of the issued and outstanding shares of Gold Standard by way of a court-approved plan of arrangement. Gold Standard’s key asset is the 100%-owned South Railroad Project, a feasibility-stage, open-pit, heap leach project located on the prolific Carlin trend in Nevada. In February 2022, Gold Standard completed a robust feasibility study and permitting activities are currently underway. Gold Standard also owns the Lewis Project, a large, strategically located, prospective land package on the Battle Mountain trend in Nevada.

Threats

- Firmer inflation is historically bullish for gold prices. Now, however, it is being quickly counteracted by more aggressive pricing for a policy response from the Federal Reserve and other central banks. As such, there needs to be more signs that economic growth is cracking under the strain of higher inflation and tighter financial conditions, which would, in turn, support sustained safe-haven inflows into the precious metals sector.

- Dacian Gold announced it was suspending operations at Mt. Morgan, and open pit operations at Jupiter are to be suspended at the end of June. Over the past six months, Dacian noted it has seen a rapid change in the environment with significant inflationary cost pressures. Dacian will process existing stockpiles of ore and focus on exploration drilling below the Jupiter Pit.

- Renowned billionaire hedge fund manager Stanley Druckenmiller says that in an inflationary bull market, he wants to own Bitcoin more than gold “for sure.” However, he explained that in a bear market, he would prefer to own the yellow metal.

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission (“SEC”). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product. Certain materials in this commentary may contain dated information. The information provided was current at the time of publication. Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content. All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (03/31/2022):

Wizz Air Holdings

Air Canada

easyJet PLC

Air France-KLM

Deutsche Lufthansa AG

Ryanair Holdings PLC

JetBlue Airways Corp.

Spirit Airlines Inc.

American Airlines

Wheaton Precious Metals

Osisko Gold Royalties Ltd.

Estee Lauder

Hermes International

Newmont Corp.

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The MVIS CryptoCompare Digital Assets 100 Index (MVDA) is a market cap-weighted index which tracks the performance of the 100 largest digital assets. The index serves as benchmark and universe for the other MVIS CryptoCompare Digital Assets Indices.

The MSCI China A Index measures large and mid-cap representation across China securities listed on the Shanghai and Shenzhen exchanges. The index covers only those securities that are accessible through “Stock Connect”.

The MSCI US REIT Index is a free float-adjusted market capitalization weighted index that is comprised of equity Real Estate Investment Trusts (REITs).

The MSCI Emerging Markets Index is a selection of stocks that is designed to track the financial performance of key companies in fast-growing nations.

The S&P U.S. Treasury Bond Index is a broad, comprehensive, market-value weighted index that seeks to measure the performance of the U.S. Treasury Bond market.

The S&P U.S. High Yield Corporate Bond Index is designed to track the performance of U.S. dollar-denominated, high-yield corporate bonds issued by companies whose country of risk use official G-10 currencies, excluding those countries that are members of the United Nations Eastern European Group (EEG).

The Bloomberg Commodity Index is a broadly diversified commodity price index distributed by Bloomberg Index Services Limited.

There is no guarantee that the issuers