We’re on the Cusp of Mass Crypto Acceptance

Date Posted: April 1, 2021

Read time: 49 min

The acceptance of digital currencies as a form of payment expanded greatly this week, foreshadowing the increasingly important role cryptos such as Bitcoin and Ether will play in our lives going forward.

By Frank Holmes

CEO and Chief Investment Officer

U.S. Global Investors

It’s happening.

The acceptance of digital currencies as a form of payment expanded greatly this week, foreshadowing the increasingly important role cryptos such as Bitcoin and Ether will play in our lives going forward.

Both Visa and PayPal announced they will begin allowing the use of cryptocurrencies to settle transactions. This comes a week after Tesla said it will now accept Bitcoin as a method of payment, and a month after Mastercard signaled it would start supporting cryptos sometime this year.

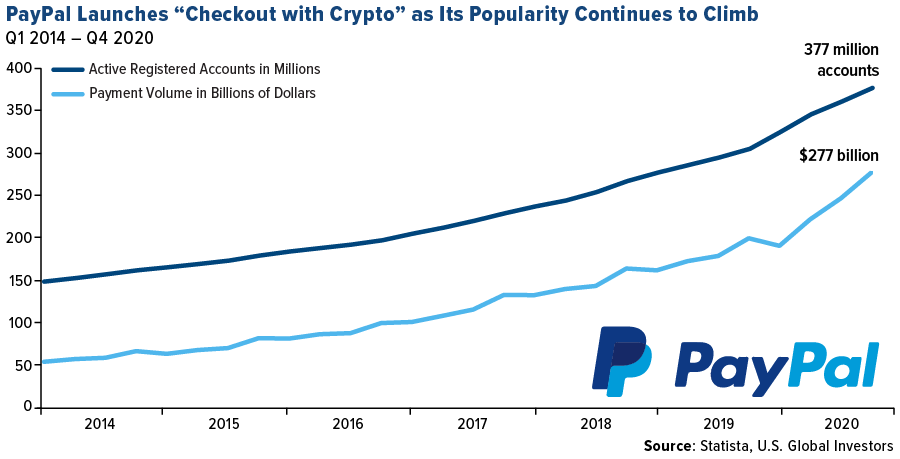

PayPal’s Checkout with Crypto, made available to select U.S. users yesterday, gives consumers the ability to purchase goods and services at as many as 29 million merchants using Bitcoin, Bitcoin Cash, Ether or Litecoin.

What’s more, there’s no additional transaction fee.

Founded in 1998 by Peter Thiel and Elon Musk, among others, PayPal has become a trusted household name. 2020 was a record year for the online payment service as people were stuck at home and companies digitized their operations. Total payment volume was a massive $277 billion, a 39% increase from the previous year, while the platform added 16 million new accounts, for a total of 377 million registered accounts.

Very soon, every one of these users will be able to use popular digital currencies to buy nearly everything, from a cup of coffee to a new car. This represents a huge leap forward for the still-emerging technology.

Visa announced this week that it became the first payment processing company to settle a transaction with USD Coin (USDC), an open-source stablecoin backed by the U.S. dollar. According to the coin’s website, USDC “is issued by regulated financial institutions, backed by fully reserved assets” and “redeemable on a 1:1 basis for U.S. dollars.” As of March 28, there were 11.3 billion USDC in circulation.

Not only will Visa users be able to make purchases with USDC, but Visa said it would also one day support new central bank digital currencies (CBDC) as they become available. According to the company, some 80% of central banks are strongly considering or in the process of launching its own national digital currency.

Mastercard is reportedly doing the same, announcing in February that it’s engaging with “several major central banks around the world” as they develop CBDCs. At the moment there’s no word on when Mastercard customers can expect to start paying with cryptos, or even which cryptos will be supported, but it seems likely we’ll hear something soon now that Visa has taken the first step.

Tesla Now Accepting Bitcoin

|

Those of you in the market for a Tesla may have noticed that you can already select Bitcoin at checkout, only a week after Elon Musk tweeted the news.

Currently the sixth largest U.S. company by market cap, having surpassed Visa and Berkshire Hathaway, Tesla has been ramping up its accumulation of Bitcoin.

If you recall, the company disclosed that it bought $1.5 billion worth of the digital currency as part of a corporate policy that allows the electric vehicle (EV) maker to invest in alternative reserve assets, including not just cryptocurrencies but also gold bullion and gold ETFs.

Musk often tweets about cryptos to his nearly 50 million Twitter followers, which can trigger incredible price swings. Dogecoin surged more than 1,000%, from $0.007 to $0.080, in as little as 12 days in January and February after the Tesla “Technoking” tweeted about it.

Someone recently developed a bot, in fact, that automatically buys Bitcoin whenever Musk mentions it in a tweet. This reminds me of the Trump & Dump Bot, which used artificial intelligence (AI) to identify publicly traded companies whenever they appeared in one of the former president’s tweets. The bot then shorted the stock and donated the proceeds to charity. Trump’s Twitter account was permanently suspended on January 8.

Gold Off to Its Worst Start in Almost 40 Years. Buy the Dip?

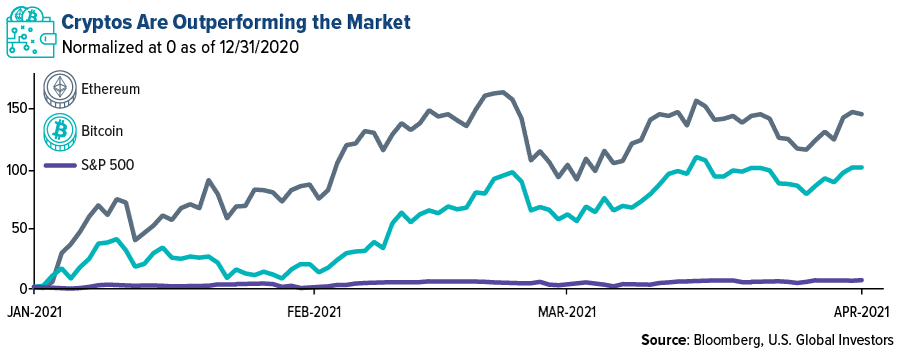

The price of Bitcoin has more than doubled so far this year and today came close to cracking the $60,000 resistance level. Ether, meanwhile, is up 150% since the start of the year.

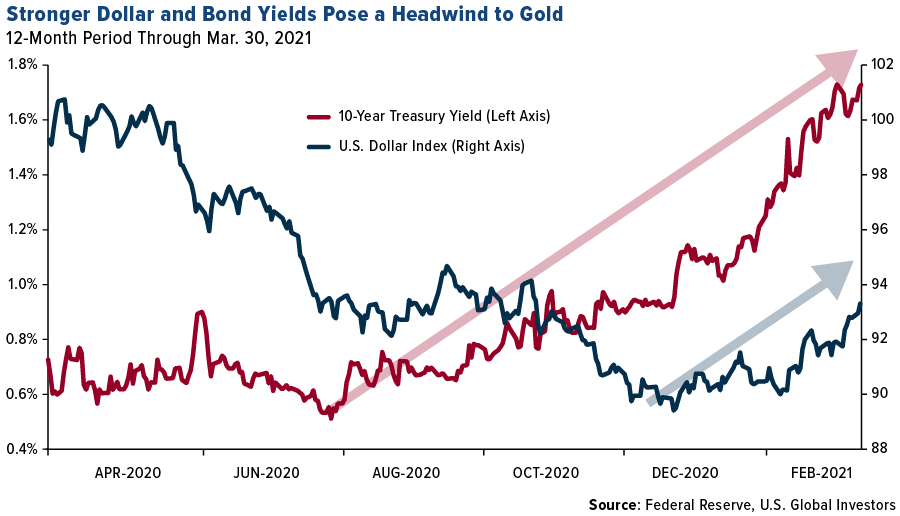

Not every inflation hedge has been a winner, though. Gold is having its worst start to the year since 1982, losing close to 12% for the three-month period, even as concerns over inflation are intensifying.

Since touching its all-time high of around $2,070 per ounce at the beginning of last August, gold has been under pressure from steadily rising bond yields. The yield on the 10-year Treasury traded at nearly 1.75% on Wednesday, the highest since January 2020, as investors dumped bonds in favor of risk assets. Bond yields rise as prices fall. The U.S. Dollar Index, meanwhile, rose above 93 this week, which also dampened the yellow metal’s appeal.

I think it’s important to point out that gold’s investment case right now remains as strong as ever, and investors would be wise to consider using this price dip as a buying opportunity. Money-printing remains at a record clip, and the debt continues to be piled on. On Wednesday, President Joe Biden outlined his $2 trillion package to rebuild U.S. infrastructure, a plan that will reportedly be paid for over time with tax hikes on corporations and wealthy Americans. This legislation, if passed, would follow the $1.9 trillion coronavirus relief package, signed into law last month.

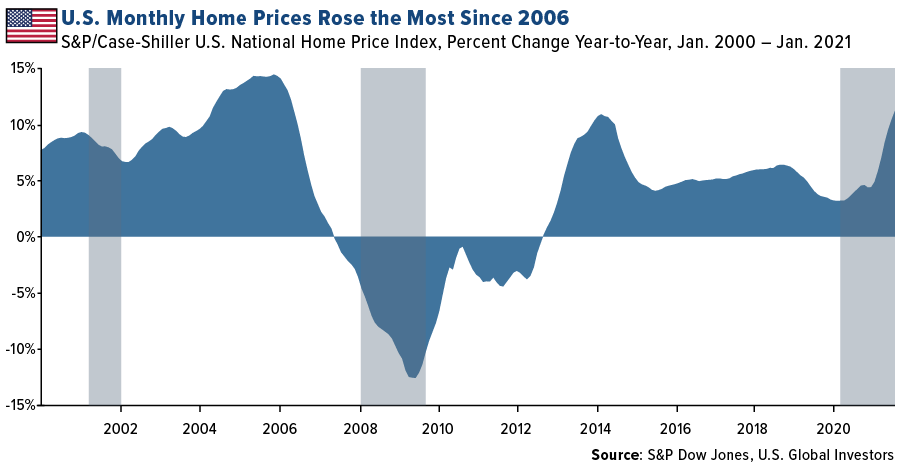

No Inflation? Home Prices Surge the Most in 15 Years

More economic data was released this week suggesting that inflation is running a lot hotter than what the Bureau of Labor Statistics (BLS) is reporting. Home prices in the U.S. rose 11.2% year-over-year in January, marking the fastest rate since February 2006. The median price for a new single-family home in the U.S. increased to $336,000 in 2020, up from $321,500 a year earlier, according to Census Bureau data.

At issue is rising commodity prices, particularly lumber, which has stalled construction of new homes. According to the National Association of Home Builders (NAHB), soaring lumber costs have added more than $24,000 to the price of a new home.

As a result, only a little over 1 million new and existing homes were available for sale in the U.S. in February, the lowest level ever in data going back to 1982, the National Association of Realtors (NAR) says.

Homeownership has historically been one of the key ways Americans build wealth. But with prices on the rise, buying a home may be out of reach for many families.

The good news is that Americans appear to be getting back to work. In March, private-sector employment increased by 517,000, the most since September. The industry with the biggest share of new jobs was leisure and hospitality, which might not seem positive at first glance since such positions tend to be low-paying, but I see it as a further positive sign that the economy is opening back up.

To learn more about inflation, check out this Frank Talk post.

Gold Market

This week spot gold closed the week at $1,729.31, down $3.21 per ounce, or 0.19%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 2.38%. The S&P/TSX Venture Index came in up 1.86%. The U.S. Trade-Weighted Dollar rose 0.14%.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Mar-30 | Germany CPI YoY | 1.7% | 1.7% | 1.3% |

| Mar-30 | Conf. Board Consumer Confidence | 96.9 | 109.7 | 90.4 |

| Mar-31 | Eurozone CPI Core YoY | 1.1% | 0.9% | 1.1% |

| Mar-31 | ADP Employment Change | 550k | 517k | 176k |

| Mar-31 | Caixin China PMI Mfg | 51.4 | 50.6 | 50.9 |

| Apr-1 | Initial Jobless Claims | 675k | 719k | 658k |

| Apr-1 | ISM Manufacturing | 61.5 | 64.7 | 60.8 |

| Apr-2 | Change in Nonfarm Payrolls | 650k | — | 379k |

| Apr-5 | Durable Goods Orders | -1.1% | — | -1.1% |

| Apr-8 | Initial Jobless Claims | — | — | 719k |

| Apr-9 | PPI Final Demand YoY | 3.8% | — | 2.8% |

Strengths

- The best performing precious metal for the holiday-shortened week was platinum, up 2.08%. The metal is expected to remain in deficit for 2021 as South African supplies will remain at risk of electricity disruptions and the growing use of fuel cells creates a new market where diesel fueled engines decline in the future.

- Gold rebounded from a nine-month low on Friday as investors weighed the impact of President Biden’s $2.25 trillion stimulus plan that would be paid for by a corporate tax increase. “The tax increase implications taking a bit of pressure off yields makes sense, and so it’s net positive for gold, at the margin short-term,” said Marcus Garvey, head of metals and bulk and commodity strategy at Macquarie Group Ltd.

- Gold held onto its gain this weekend even as the U.S. manufacturing sector saw a significant rise in sentiment in March. ISM said its manufacturing index hit 64.7 last month, up from 60.8 in February.

Weaknesses

- The worst performing precious metal for the week was silver, drifting down 0.36% on little price moving news. Gold extended declines on Thursday as the U.S. vaccine rollout and plans for more stimulus boosted both bond yields and the dollar. The yellow metal fell below $1,700 an ounce. Bullion had its first quarterly drop in more than two years and is having its worst start to the year since 1982, down 11%.

- Due to a weakening market, Russia’s GV Gold is putting its IPO on hold. The Blackrock-backed miner had hoped for a $1.5 billion valuation.

- Norilsk Nickel, the world’s largest producer of palladium and refined nickel, said it will resume full production of metals after stopping water inflows at a key mine. Bloomberg notes palladium prices fell as much as 4.4% after the announcement, while platinum dropped 1.8%.

Opportunities

- The Public Investment Corp, which manages South African government worker pensions, said it has invested more than $7.4 billion in mining companies including Sibanye Stillwater, Anglo American Platinum and Impala Platinum Holdings, reports Bloomberg. Portfolio manager Mdu Bhulose said the platinum miner bet has brought “great” returns over the last three years. “The supply and demand dynamics are quite solid, and they are talking to a tightening market which should be supportive of prices.”

- Calibre Mining updated its mineral reserves and mineral resources at its mining complexes in Nicaragua, reports Kitco News. The miner said its mineral reserves were up 202% to 864,000 ounces of gold since year-end 2019 and after 2020 depletion. Andean Precious Metals, a silver producer focused on Bolivia, began trading on the Toronto Venture Exchange. The miner produced 5.9 million ounces of silver last year with all-in-sustaining costs of $15 per ounce.

- Aberdeen Standard Investments is optimistic that gold can still rise to $2,000 an ounce, despite recent headwinds of a stronger dollar and rising bond yields. Steve Dunn, head of exchange-traded products, told Kitco News in a phone interview that the fundamental stories for gold are still in place. Dunn said that their base-case scenario is for gold to trade between $1,900 and $2,000 an ounce by the end of the year.

Threats

- Bloomberg Intelligence senior commodity strategist Mike McGlone says the gold bull market has stalled. "The gold bull market has clearly stalled, and we believe it’s transitioning toward a long-slog, range-bound market …Unless the higher price discovery process in Bitcoin reverses, the crypto represents a top gold headwind." Bullion could remain stuck in the trading range of $1,600 to $1,900 an ounce as the metal has lost support of ETF inflows and as investors focus more on Bitcoin and cryptocurrencies.

- South African labor group National Union of Mineworkers is demanding a 15% to 20% salary increase. Workers are asking for a minimum of 15,000 rand a month and want to address wage disparity and housing allowances, reports Bloomberg.

- Evolution Mining said it will focus exclusively on operations in Australia and Canada as the growth of China’s influence and resource nationalism makes it increasingly difficult to develop projects in emerging countries, reports Bloomberg. CEO Jake Klein said, “they have cheap access to capital, and they have a government that has a strategic capacity to influence the national government because they’re lending at a sovereign level.” Klein said it will be more difficult for miners to get into Africa, citing Resolute Mining’s recent termination of a mining lease in Ghana.

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 0.24%. The S&P 500 Stock Index rose 1.14%, while the Nasdaq Composite climbed 2.60%. The Russell 2000 small capitalization index gained 1.46% this week.

- The Hang Seng Composite gained 2.80% this week; while Taiwan was up 1.63% and the KOSPI rose 1.53%.

- The 10-year Treasury bond yield fell 1 basis point to 1.673%.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performer for the week was Filecoin, rising 159.07%.

- Bitcoin had its best first quarter since 2013, buoyed by the rising inflation expectations. Rising more than 100% since the start of the year, Bitcoin hit the all-time high of approximately $61,000 mid-March and has stayed above $50,000 since. Ethereum also had a good start to the year, gaining more than 150% and hitting all-time high of more than $2,000. The chart below shows the performance of these top two cryptocurrencies against the S&P 500 Index.

- BlackRock, the biggest asset manager in the world, has started trading Bitcoin futures, according to a regulatory filing published this week. The company held $6.5 million in CME Bitcoin futures contracts and those contracts had appreciated $360,457 on reporting day. However, the holdings represent only 0.03% of BlackRock’s massive Global Allocation Fund, and the gains represent just 0.0014%. Additionally, BlackRock had given two of its funds the approval to trade Bitcoin futures in January.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week was BTMX, down 21.15%.

- Bank of Korea Governor Lee Ju-yeol believes that central bank digital currencies (CBDCs) will erode the demand for existing cryptocurrencies like Bitcoin. He added that Bitcoin and other crypto assets have high price volatility and that limits to how well they can function as a means of payment or as a store of value. Bank of Korea is planning to pilot its CBDC later this year, along with China, Russia, Turkey, and Jamaica. In South Korea’s pilot, the bank is testing the CBDC for fund transfers, payments, issuance, distribution, and redemption.

- Canada is seeing a dramatic growth in Bitcoin adoption, but the rate of cryptocurrency fraud is also increasing at a rapid pace. Between 2017 to 2020, digital currency-related fraud in Canada rose by about 400%. These frauds have happened in the form of extortion scams or attracting victims with fake schemes promising high abnormal returns. From January to August 2020, Canadians lost over $8.7 million in crypto-asset frauds and in the first week of March 2021, Vancouver residents lost more than $2 million through scams.

Opportunities

- The Chicago Mercantile Exchange (CME) is launching smaller-sized Bitcoin future contracts in May in a bid to expand the number of people who can bet on the future price of the leading cryptocurrency. CME said that the new contracts, sized at one-tenth of one Bitcoin, will be available for trading starting May 3 and will be settled in cash. These new futures contracts come as a result of widespread demand from a broad array of CME clients, according to the company’s press release. The micro futures will offer the same features and benefits as CME’s standard Bitcoin futures, which were launched in 2017.

- Goldman Sachs is reportedly close to offering crypto to its private wealth management clients and has appointed a new global head, Mary Rich, to manage the segments. Rich said that the bank is planning on offering a full spectrum of investments in Bitcoin and other digital assets, whether that is through the physical Bitcoin, derivatives, or traditional investment vehicles. This news comes a few weeks after Goldman Sachs relaunched its cryptocurrency trading desk after three years, with plans to support Bitcoin futures trading.

- Visa reported that it had processed a cryptocurrency payment directly on the Ethereum blockchain as part of a new service it plans to introduce to its partners this year. According to the press release, Crypto.com, Visa’s crypto debit card partner, sent a USDC stablecoin transaction on Ethereum to an account at Anchorage custody under Visa’s name. Before this functionality, Crypto.com had to sell cryptocurrencies to cover its obligations to Visa in cash. Visa also said that it plans on fleshing out its crypto-native services by supporting reconciliation and currency conversion for stablecoins and creating settlement reports with blockchain wallet addresses to verify transactions.

Threats

- After Indian lawmakers proposed a potential ban on all “private” cryptocurrencies, crypto exchanges in the country are planning to present the government and central bank with their vision of a productive regulatory regime. The exchanges have compiled a package of detailed documents, explaining the current state of the crypto industry in India and possible ways to regulate it. Currently, India has more than 10 million crypto users, over half-a-million day-traders and more than 3,000 people employed in the crypto industry.

- Bolster, a deep learning-powered fraud prevention platform, reported the five areas of scams or frauds that are booming along with the NFT bubble. These include replica NFT stores, fake NFT stores, counterfeit or fraud NFTs, fake airdrops and NFT giveaways, and social media scams. In March, Bolster found that the number of suspicious-looking domain registrations with names of NFT stores like ‘rarible’, ‘opensea’, and ‘audius’ have increased nearly 300%. The company expects the scams to keep increasing as more people participate in the current NFT craze and is advising people to be wary of these scams.

- Boris Schlossberg, Managing Director of FX strategy at BK Asset Management, said that CME Group’s announcement of introducing micro-Bitcoin futures could be a sign that the market is at the top. He added that an asset, like Bitcoin, which has a volatility of 20% per week can not act as a currency at this point and that transactions occurring in Bitcoin are going to remain infinitesimally small relative to regular currency. Additionally, he is predicting that crypto-assets might be close to an intermediate-term top and that a correction is certainly due at this point.

Domestic Economy and Equities

Strengths

- Consumer confidence rose in March to its highest level since the pandemic started a year ago, with Americans expressing more optimism about business and labor-market conditions in the coming months. The Conference Board said its consumer confidence index increased to 109.7 in March from 90.4 in February. The reading marked the third-consecutive monthly increase.

- Manufacturing activity in Texas expanded at a markedly faster pace in March than in the previous month, reaching the highest reading in the 17 year of history of the Texas Manufacturing Outlook Survey. The production index of the Texas Manufacturing Outlook Survey, a key measure of state manufacturing conditions, came in at 48.0 in March, up from 19.9 in February and indicative of a sharp acceleration in output growth.

- Applied Materials was the best performing S&P 500 stock for the week, increasing 9.9%. The shares jumped on news that Taiwan Semiconductor will spend $100 billion over the next three years to expand capacity. Nearly 18% of Applied Materials’ sales are to Taiwan Semiconductor.

Weaknesses

- Pending home sales, a leading indicator of the health of the housing market, plunged in February across all regions in the U.S. The National Association of Realtors’ (NAR) Pending Home Sales Index, which tracks the number of homes that are under contract to be sold, fell 10.6% in February from a month earlier — falling for the second straight month.

- Initial jobless claims increased more than expected, and continued jobless claims decreased less than expected. Initial claims were 719,000 for the week ending March 27. Continuing claims were 3.79 million, versus a consensus of 3.75 million. The largest increases were seen in Virginia, Kentucky and Georgia.

- Carmax was the worst performing S&P 500 stock for the week, decreasing 7.7%. The company reported same store sales down 2% year-over-year, with a 2.3% drop in used car sales.

Opportunities

- Texas Instruments was upgraded to overweight from sector weight at KeyBanc Capital Markets, which wrote that the chipmaker has strong long-term growth prospects. The company is “well positioned near term to service demand,” and its decision to not increase pricing and capacity “is driving incremental share gains that should lead to outperformance over the next several years,” analyst John Vinh wrote.

- Apple was upgraded to buy from neutral at UBS, which cited a more stable long-term iPhone demand backdrop and the option value of the company’s likely entry into the auto market. Analyst David Vogt expects iPhone demand in FY21 and FY22 to be “relatively stable in-line with historic demand trends,” based on analysis of procurement, upgrade rates and customer retention, specifically outside of China.

- Hess Corp. was upgraded to buy from neutral at Mizuho Securities, which cited a more positive view for the energy company’s cash-flow growth. Sustaining capital requirements are lower for exploration and production companies with an offshore presence, and “this means higher sustaining free cash-flow yield and likely higher capacity for cash return as projects come online and balance sheets normalize,” the firm wrote.

Threats

- CNO Financials’ prospects for outperformance look limited with claims utilization tailwinds from the pandemic during 2020 now expected to recede, Piper Sandler wrote in note as it cut to neutral from overweight. Analyst John Barnidge says CNO may struggle to grow earnings in 2021 and sees a challenged backdrop for EPS.

- Brookfield Asset Management was downgraded to neutral from outperform at Credit Suisse, which sees headwinds that will limit near-term outperformance. Analyst Andrew Kuske said in a note those include dynamics around BAM’s bid to buy Brookfield Property Partners as well as negative impacts from rising rates.

- Credit rating agencies have downgraded their outlooks for Nomura and Credit Suisse, citing concerns over risk management as the banks confront multibillion dollar losses from the Archegos Capital Management debacle. Nomura and Credit Suisse were among banks that allowed Archegos, a New York-based family office run by former hedge fund manager Bill Hwang, to amass billions of dollars of exposure to equities through swap contracts. The trades imploded last week, leaving the banks scrambling to sell shares.

Energy and Natural Resources Market

Strengths

- The best performing commodity for the week was lumber, up 6.38%. Lumber’s rally this year is attributed to lean product inventories, and an inability of the industry to surge capacity as Covid-related labor disruptions weigh on productivity. The S&P/TSX Forest Products Index rose 46% last year and is up 12% this year.

- Trafigura Group agreed on a five-year deal with Enterprise Generale du Cobalt, a Democratic Republic of Congo state-owned company with monopoly rights to the purchase and sale of the country’s hand-mined cobalt, which started operations this week. Congo is the world’s largest producer of cobalt, which is used in lithium-ion batteries that power electric vehicles. Trafigura will help finance the creation and control of the mining zones, ore purchasing and all costs related to buying, transforming and delivering cobalt hydroxide to end buyers.

- OPEC+ has agreed to increase oil production gradually from May to July, as both internal and external pressure to supply more crude to the recovering global economy drove the decision. Saudi Arabia is set to phase out its voluntary extra 1 million barrels-a-day supply cut by July, adding 350,000 barrels-a-day in both May and June and another 440,000 barrels a day by July. Analysts believe that increasing production by 1 million barrels a day in the next three months when product demand is expected to rise by about 3 million barrels a day over the same period is not bearish but a conservative anticipation as demand from U.S. and Asian economies is increasing while additional lockdowns in Europe might hinder the continent’s demand for oil.

Weaknesses

- The worst performing commodity for the week was coffee, down 5.37%. Coffee is facing a worldwide supply shortage as Brazil Covid-19 cases are increasing, causing a drop in production, and a recent drought affected the harvest. Meanwhile, Colombia is facing torrential rain which can severely affect the harvest.

- Exxon Mobil Corp. is reportedly expecting its earnings to take a hit of as much as $800 million from the deep freeze that affected Texas’ electric grid. The Texas freeze wreaked havoc on gas and power markets, with electricity retailers including Just Energy Group Inc. and Griddy Energy LLC declaring bankruptcy.

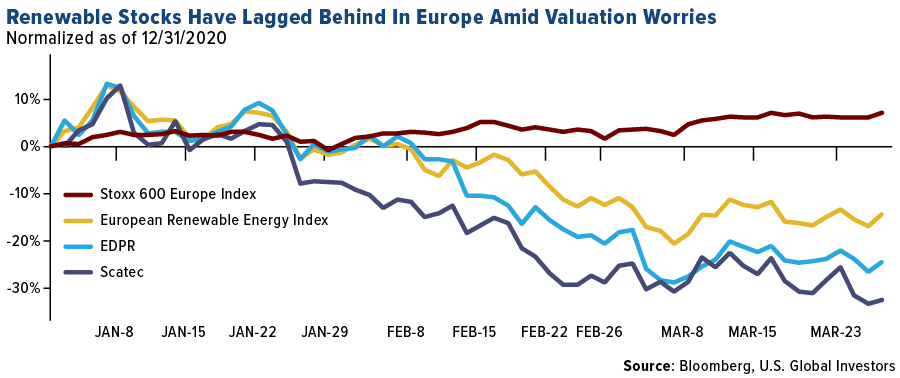

- Renewable energy stocks have been lagging in Europe since the beginning of the year, with the European Renewable Energy Index down 12%. During the first quarter, companies like Norway’s solar firm Scatec ASA and Portugal’s EDP Renovaveis SA dropped more than 20%. One of the reasons for a laggard start to the year was that equity valuations were already too expensive after a stellar 2020.

Opportunities

- President Joe Biden unveiled his $2.25 trillion infrastructure proposal this week, allotting $115 billion for roads and bridges and $16 billion to put laid-off oilfield laborers to work plugging abandoned wells and mines across the nation. Additionally, investments in electric vehicles and renewable power have been given importance.

- South Korea is planning on spending $42.8 billion over the next decade to build the biggest offshore wind farm in the world. The proposed wind farm would generate up to 8.2 gigawatts of power and is one of the grand projects that the government wants to roll out with private sector backing to meet its ambition of becoming carbon neutral by 2050.

- Citigroup Inc. is combining its energy, power and chemicals investment-banking groups into a new natural resources and clean energy transition group. The proposed unit will work alongside other coverage areas, including industrials and technology. The bank expects energy transition and structural changes underway in global energy systems to drive towards low and zero carbon solutions to accelerate over the next decade and that their energy, power, and chemicals clients, ranging from multinational corporations to fast growing alternative and clean energy companies, are at the heart of this transition.

Threats

- The market for higher-end coffee is facing supply shortages amidst an expected increase in consumption as Covid-19 restrictions are easing and vaccinations are encouraging people to increase spending. Arabica beans, used in espressos and lattes, are already short in supply because of a drought in Brazil this year, the biggest producer. Now, torrential rains are threatening crops in Colombia, the second-biggest producer. Global coffee deficit could climb to 10.7 million bags this year and premiums for Colombian coffee in the cash market are near the highest in a decade.

- Militants in Mozambique attacked the town of Palma, close to France’s Total SE’s $20 billion liquefied natural gas project. The Paris-based company suspended plans to resume construction as the attack is the latest in a series of incidents that are undermining the southern African country’s hopes of developing some of the continent’s biggest private investment projects.

- As President Joe Biden unveiled his $2.25 trillion infrastructure plan, analysts started paying attention to the commodities that the U.S. will be needing to meet the expectations of the plan and figured out one problem in the plan: China. As the rest of the world went into lockdown and commodity prices plunged in March and April 2020, Chinese manufacturers, traders and the government went on a shopping spree. China imported 6.7 million tons of unwrought copper, a third more than the previous year, and the year-over-year increase alone is equivalent in scale to the entire annual copper consumption of the U.S. Additionally, China is the world’s largest producer of rare Earth metals and dominates the processing of raw materials needed to make lithium-ion batteries – lithium, cobalt, nickel, and graphite. If the U.S. wants to reach its infrastructure goals, it will have to rely on China for its commodity needs.

Airline Sector

Strengths

- The best performing airline stock for the week was Norwegian Air Shuttle, up 25.2%. The airline secured approval of its restructuring plans from an Irish judge, paving the way for the discount carrier to exit insolvency. The company also plans to raise new capital in May, as well as restructure to focus on short-haul routes only.

- U.S. booking trends continue to accelerate and are now at 70-80% of 2019 levels. This should continue to help revenue and cash flow performance for U.S. airlines, especially moving into the summer season. Business travel, which has remained subdued, has the potential to increase in the second half of the year. Cancellations and re-bookings have been stable, implying that booking trends represent real improvement.

- Fares for U.S. airlines are improving, although they are still 20% below 2019 levels. JetBlue, Spirit and United Airlines have been the most aggressive in pushing up fares off recent lows. This may help revenue performance for these carriers, especially going into the summer travel season.

Weaknesses

- The worst performing airline stock for the week was TAV Havalimanlari, down 6.3%. Virus cases continue to increase in parts of the world, which could derail the industry’s recovery. European airlines are decreasing seats by as much as 80% as only 5% of citizens are fully vaccinated.

- The Latin American airline market remains negatively impacted by COVID-19. The Brazilian airline market is struggling due to worsening infection numbers and deaths. Peru has also had issues due to lockdowns with short notice, making scheduling difficult.

- United and American have recently extended expiration dates for flight credits. At the beginning of the pandemic, airlines were faced with enormous requests for refunds, and as a measure to save cash, issued flight credits and travel vouchers. Right now, about 11% of all open, unused tickets are set to expire this year. Extending the deadline beyond the 12-month limit extends the air travel liability on the airlines’ balance sheets.

Opportunities

- Southwest announced a large order of 100 Boeing 737 Max 7 jets. In addition, the company indicated that they may purchase an additional 155. The carrier also switched 70 orders it had for the Boeing 737 Max 8 to the Boeing 737 Max 7 jet. The 100-plane order is valued at $10 billion.

- Boeing delivered its first 787 Dreamliner in months, going to United Airlines. This is the first aircraft in this series that has been delivered in five months. United is expected to take another 10 deliveries of this aircraft model this year.

- European airline stocks are poised to outperform. Vaccinations in Europe are expected to pick up in April, with economies reopening by May or June. This should lead to higher load factors, and ultimately higher profits.

Threats

- The French government is close to finalizing a recapitalization plan for Air France, but it will come at a high cost. Coveted landing rights at both Paris-Orly and Amsterdam airports will be surrendered to receive the aid. It is estimated that up to 7% of slots at each airport will be surrendered.

- Airlines have begun their frequent flier programs as collateral for loans. United, Delta and American have raised more than $25 billion through debt deals backed by the traveler loyalty program. Spirit and Hawaiian Holdings have raised an additional $2 billion by leveraging their frequent flier programs. Unfortunately, leveraging these assets for bond holders hurts equity holders, who previously had prime rights to these programs.

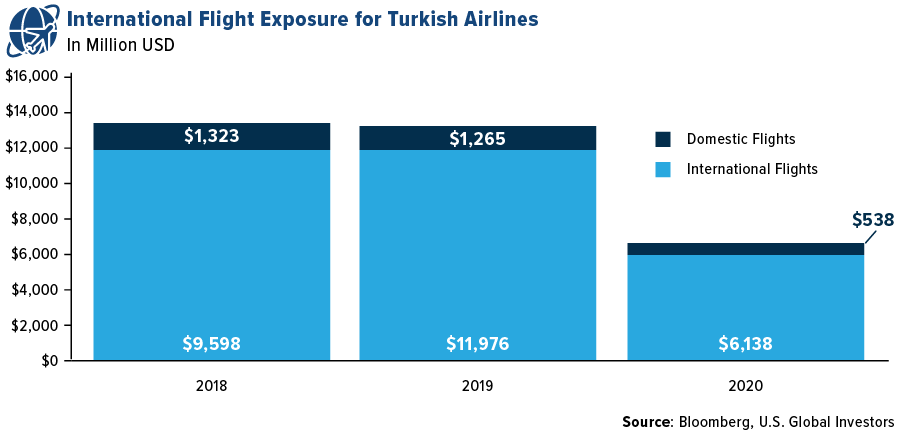

- It will take Turkish Airlines much longer than other airlines to recover. Capacity now is 62% below year-ago levels. For the airline to fully recover, it must relaunch most of its fleet, including its fleet for international flights. International passengers are 49% of traffic and 90% of revenue for the airline. Traffic is subdued due to various COVID-related restrictions.

Emerging Markets

Strengths

- The best performing country in emerging Europe for the week was Romania, gaining 3.41%. The best performing country in Asia this week was Vietnam, gaining 4.64%.

- The Polish zloty was the best performing currency in emerging Europe this week, gaining 102 basis points. The Pakistani rupee was the best performing currency in Asia this week, gaining 162 basis points.

- The European Commission’s economic sentiment indicator (ESI) for the eurozone jumped in March, taking it slightly above its long-term average for the first time since the outbreak of COVID-19. The headline index increased 7.6 points to 101.0, compared with consensus 96.0 and prior 93.4.

Weaknesses

- The worst performing country in emerging Europe for the week was the Czech Republic, losing 0.23%. The worst performing country in Asia this week was Indonesia, losing 2.97%.

- The Russian ruble was the worst performing currency in emerging Europe this week, losing 80 basis points. The Indian rupee was the worst performing currencies in Asia, losing 96 basis points.

- Brazil’s industrial production took a hit in February with major cities imposing restrictions on commerce and movement to curb a second wave of COVID-19 cases. Industrial output in the nation decreased by 0.7% month-over-month, well below the median estimate of a 0.5% gain. The drag is accredited to vehicle production, down 7.2%, and extractive industries, down 4.7%.

Opportunities

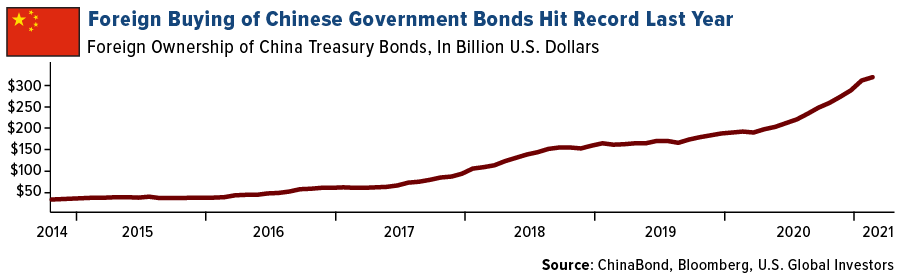

- Index provider FTSE Russell approved Chinese sovereign bonds inclusion into its indices. Chinse sovereign bonds will have the sixth-largest weighting in FTSE Russell’s World Government Bond Index, but it will take three years to increase the weight to the desired level. Global funds have been already buying Chinese debt given its yield advantage. The head of China macro research at Standard Chartered Plc., Becky Liu, said that China may see inflows into Chinese bonds of $130 billion to $156 billion from the inclusion.

- Goldman Sachs’ analysts recommend buying Russian and South African equities as they tend to outperform their emerging market peers when both U.S. real yields and commodity prices are high. Analysts are saying that valuations are attractive in both nations and this should offer money managers the opportunity to get ahead of a rebound in risky assets as vaccine distribution ramps up and leads to a comeback in economic growth.

- Brasilprev Seguros, one of Brazil’s largest pension funds, is planning on an expansion this year as low interest rates continue to drive savers to higher-yielding investments. The private pension fund, which oversees $55 billion and holds a 30% market share in the country’s private pension system, expects to increase its assets by as much as 7% this year. The fund’s customer base grew 7.5% in the 12 months ended in January 2021, while Brazil’s unemployment rate soared to a record 14.6% in November.

Threats

- Parts of Eastern Europe are currently the world’s deadliest for COVID-19. The Czech Republic is battling the opposition about prolonging a state of emergency. Hungary, which has the highest mortality rate globally during the past week, will shorten its night-time curfew and allow all stores to reopen a few days after Easter.

- Chile is set to close its borders for the month of April in a bid to curb its worst COVID-19 outbreak to date. Chilean citizens and foreign residents will not be allowed to enter or leave the country starting April 5, and truck drivers will be required to present a negative PCR test carried out in the 72 hours before entering the country.

- Rising inflation, interest rates and debt in Latin America provides a bleak outlook for the bond market. A combination of loose monetary policy and a resurgence of the pandemic, fueled inflation and debt concerns in March, as swap curves show that traders expect policy makers to raise interest rates in response. While the 10-year U.S. Treasury yield rose 31 basis points in March, their local-currency counterparts climbed between 59 points (Mexico) and 94 points (Colombia). This jump in yields is due to the concerns that the impact of COVID-19 is going to be felt for many years as increased spending and low economic activity push up debt-to-GDP levels.

Leaders and Laggards

| Index | Close | Weekly Change($) |

Weekly Change(%) |

|---|---|---|---|

| 10-Yr Treasury Bond | 1.67 | -0.00 | -0.30% |

| Oil Futures | 61.28 | +0.31 | +0.51% |

| Hang Seng Composite Index | 4,560.88 | +124.18 | +2.80% |

| S&P Basic Materials | 499.30 | -1.25 | -0.25% |

| Korean KOSPI Index | 3,087.40 | +46.39 | +1.53% |

| S&P Energy | 379.71 | -1.47 | -0.39% |

| Nasdaq | 13,480.11 | +341.39 | +2.60% |

| DJIA | 33,153.21 | +80.33 | +0.24% |

| Russell 2000 | 2,253.90 | +32.42 | +1.46% |

| S&P 500 | 4,019.87 | +45.33 | +1.14% |

| Gold Futures | 1,730.10 | -4.60 | -0.27% |

| XAU | 139.93 | +4.06 | +2.99% |

| S&P/TSX VENTURE COMP IDX | 960.84 | +17.55 | +1.86% |

| S&P/TSX Global Gold Index | 295.20 | +8.73 | +3.05% |

| Natural Gas Futures | 2.63 | +0.07 | +2.85% |

| Index | Close | Monthly Change($) |

Monthly Change(%) |

|---|---|---|---|

| Korean KOSPI Index | 3,087.40 | +43.53 | +1.43% |

| 10-Yr Treasury Bond | 1.67 | +0.28 | +20.10% |

| Gold Futures | 1,730.10 | -6.40 | -0.37% |

| S&P Basic Materials | 499.30 | +23.75 | +4.99% |

| S&P 500 | 4,019.87 | +149.58 | +3.86% |

| DJIA | 33,153.21 | +1,761.69 | +5.61% |

| Nasdaq | 13,480.11 | +121.31 | +0.91% |

| Oil Futures | 61.28 | +1.53 | +2.56% |

| Hang Seng Composite Index | 4,560.88 | -76.28 | -1.64% |

| S&P/TSX Global Gold Index | 295.20 | +15.82 | +5.66% |

| XAU | 139.93 | +5.09 | +3.77% |

| Russell 2000 | 2,253.90 | +22.39 | +1.00% |

| S&P Energy | 379.71 | +12.40 | +3.38% |

| S&P/TSX VENTURE COMP IDX | 960.84 | -66.91 | -6.51% |

| Natural Gas Futures | 2.63 | -0.21 | -7.36% |

| Index | Close | Quarterly Change($) |

Quarterly Change(%) |

|---|---|---|---|

| XAU | 139.93 | -7.21 | -4.90% |

| S&P/TSX Global Gold Index | 295.20 | -26.99 | -8.38% |

| Gold Futures | 1,730.10 | -170.90 | -8.99% |

| DJIA | 33,153.21 | +2,743.65 | +9.02% |

| S&P 500 | 4,019.87 | +287.83 | +7.71% |

| Nasdaq | 13,480.11 | +610.11 | +4.74% |

| Korean KOSPI Index | 3,087.40 | +213.93 | +7.45% |

| Natural Gas Futures | 2.63 | +0.21 | +8.59% |

| S&P Basic Materials | 499.30 | +45.42 | +10.01% |

| Russell 2000 | 2,253.90 | +273.91 | +13.83% |

| Oil Futures | 61.28 | +12.88 | +26.61% |

| Hang Seng Composite Index | 4,560.88 | +296.40 | +6.95% |

| S&P/TSX VENTURE COMP IDX | 960.84 | +95.58 | +11.05% |

| S&P Energy | 379.71 | +91.23 | +31.62% |

| 10-Yr Treasury Bond | 1.67 | +0.75 | +80.86% |

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission ("SEC"). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (12/31/2020):

Visa Inc.

Tesla Inc.

MMC Norilsk Nickel PJSC

Sibanye Stillwater Ltd

Anglo American Plc

Impala Platinum Holdings Ltd

Calibre Mining Corp

Evolution Mining Ltd

Delta Air Lines

American Airlines

Southwest Airlines

JetBlue Airways Corp

United Airlines Holdings

Apple Inc

Total SE

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment. The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index. The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges. The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The U.S. dollar index (USDX) is a measure of the value of the U.S. dollar relative to the value of a basket of currencies of the majority of the U.S.’s most significant trading partners. The S&P CoreLogic Case–Shiller U.S. National Home Price Index is a composite of single-family home price indices for the nine U.S. Census divisions. The Consumer Confidence Index (CCI) is a survey, administered by The Conference Board, that measures how optimistic or pessimistic consumers are regarding their expected financial situation. The CCI is based on the premise that if consumers are optimistic, they will spend more and stimulate the economy but if they are pessimistic then their spending patterns could lead to a recession. The Dallas Fed conducts the Texas Manufacturing Outlook Survey monthly to obtain a timely assessment of the state’s factory activity. Firms are asked whether output, employment, orders, prices and other indicators increased, decreased or remained unchanged over the previous month. Responses are aggregated into balance indexes where positive values generally indicate growth while negative values generally indicate contraction. The Pending Home Sales Index (PHS), a leading indicator of housing activity, measures housing contract activity, and is based on signed real estate contracts for existing single-family homes, condos, and co-ops. Because a home goes under contract a month or two before it is sold, the Pending Home Sales Index generally leads Existing-Home Sales by a month or two. FTSE Russell’s flagship global fixed income index, the FTSE World Government Bond Index (WGBI), measures the performance of fixed-rate, local currency investment-grade sovereign bonds. The European Renewable Energy Index tracks the performance of European renewable energy companies that are active in either or several of the following six investment clusters: biofuels, geothermal, marine, solar, water, and wind. The S&P Global Timber & Forestry Index is comprised of 25 of the largest publicly traded companies engaged in the ownership, management or the upstream supply chain of forests and timberlands.