Frank Talk

America’s Infrastructure Needs Some Love, but Will Rising Rates Check Spending?

Date Posted: March 5, 2021

Read time: 47 min

Every four years, the American Society of Civil Engineers (ASCE) releases its report card on the condition of America's infrastructure. In 2017, the group gave the U.S. a dismal D+, writing that crumbling infrastructure "is impeding our ability to compete in the thriving global economy."

By Frank Holmes

CEO and Chief Investment Officer

U.S. Global Investors

Every four years, the American Society of Civil Engineers (ASCE) releases its report card on the condition of America’s infrastructure. In 2017, the group gave the U.S. a dismal D+, writing that crumbling infrastructure “is impeding our ability to compete in the thriving global economy.”

The 2021 report demonstrates slight progress from four years ago. America’s infrastructure scored a C-, the first time in 20 years that our “GPA” is out of the D range.

But as those of you with kids and grandkids know, a C- is nothing to celebrate. Much work still remains to bring our roads, bridges, sea ports, electric grids and more up to satisfactory standards.

That means there may be some incredible opportunities for investors in companies that produce the metals, minerals and other raw materials that will be needed with an increase in spending.

According to the ASCE, the U.S. faces a $2.6 trillion investment gap over the next 10 years. Among the most critical is the nation’s 4 million miles of public roadways, 40% of which is now considered to be in “poor” or “mediocre” condition. Deteriorating, congested roads and highways cost U.S. motorists a combined $130 billion every year in wasted time and fuel, not to mention vehicle repair.

The U.S. has been underfunding its roadways for years, resulting in a $786 billion backlog of road and bridge capital needs, the ASCE says.

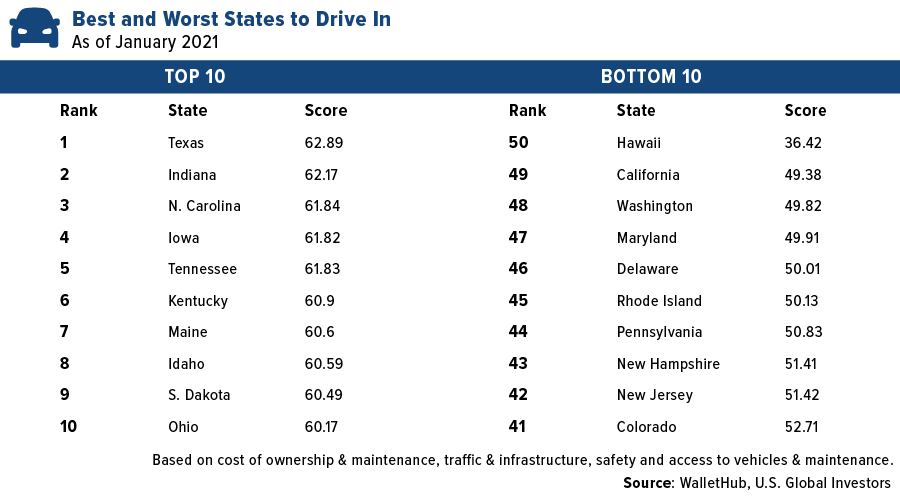

Not all roads are made equal, though. I’m pleased to report that our home state of Texas topped the list of best states to drive in, based on four factors including traffic and infrastructure, according to WalletHub. Indiana, North Carolina, Iowa and Tennessee rounded out the top five. Hawaii was found to be the state with the worst commuting conditions, followed by California, Washington, Maryland and Delaware.

Energy Experts to Texas: Winterize Your Power Plants or Connect with the Rest of the U.S.

The quality of Texas roads was one of the 11 reasons why I think people enjoy living in the Lone Star State.

The state’s power grid, on the other hand, needs some serious attention. As you know, an unusual winter storm last month caused days-long power outages throughout most of the state, leaving millions without electricity, water and heating.

This week, top energy “experts” recommended that Texas either winterize its electric generation plants—including not just wind turbines but also coal and natural gas plants—or consider connecting its grid with neighboring states, according to reporting by Reuters. Texas is the only U.S. state to operate its own power grid, which is managed by the dubiously named Electric Reliability Council of Texas (ERCOT).

ERCOT’s president and CEO, Bill Magness, was fired this week after as many as seven board members resigned in the wake of the power failures. Magness reportedly turned down an $800,000 severance package.

As I pointed out a couple of weeks ago, Texas is the ninth largest economy in the world. Winterizing its aging power grid will be a massive undertaking, requiring biblical amounts of raw materials. Investors take note.

…But Borrowing Costs Are Climbing

Like his last two predecessors, President Joe Biden has put infrastructure at the top of his list of priorities. Can he succeed where former presidents Barack Obama and Donald Trump failed?

Reuters reports that the White House has added transportation and manufacturing specialists to its ranks of advisors as the Biden administration prepares to lobby Congress for an infrastructure bill, possibly once the pandemic relief bill is signed. Also this week, the president and Transportation Secretary Pete Buttigieg met with House lawmakers to discuss such a plan.

The commitment is there, but rising borrowing costs could put a hamper on things.

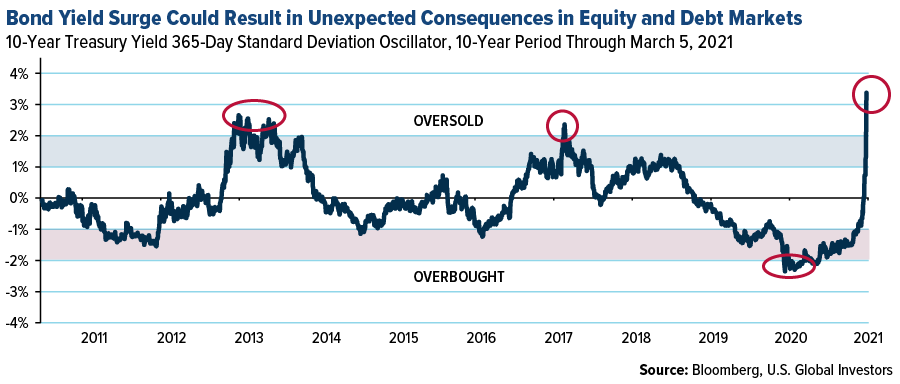

The bond selloff continued this week after a mostly positive jobs report, sending the yield on the 10-year Treasury as high as 1.6% today. Bond yields rise when prices fall. To put this in perspective, the yield was trading below 1% in December.

This represents a significant 3 standard deviation (or sigma) move for the 60-day trading period, suggesting the selloff is overdone.

When we look at the 365-day trading period for the past 10 years, the move is even more dramatic. The probability for mean reversion is very high, but in the meantime, this vertical surge in yields will likely cause unexpected consequences in both equity and debt markets

Watch my video on how to trade gold using standard deviation by clicking here.

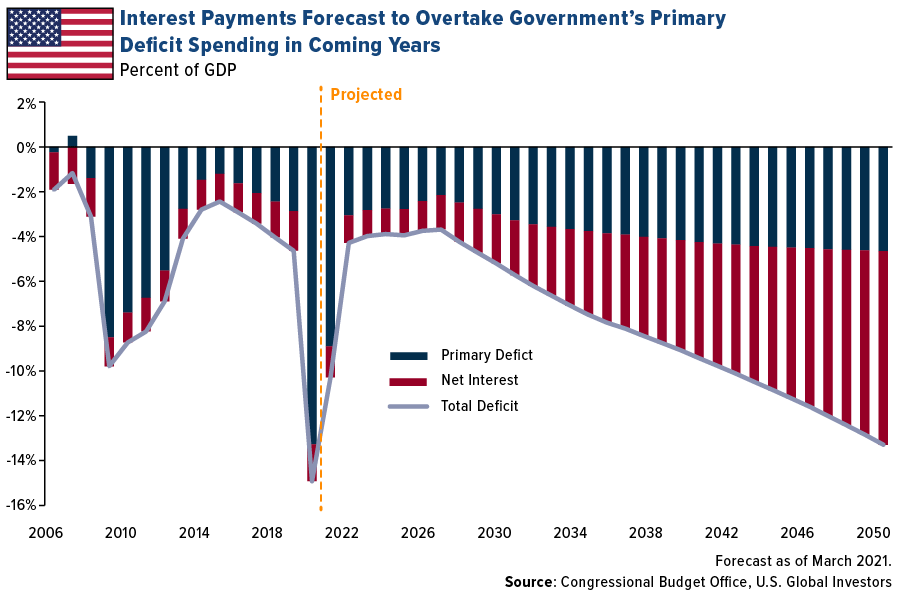

The rise in borrowing costs could very well check some lawmakers’ appetite for a large infrastructure spending bill at a time when the deficit is already at or near record levels as a percent of GDP. In its just-released budget outlook, the Congressional Budget Office (CBO) expects the U.S. deficit to improve following the pandemic, but then sharply expand as interest payments eventually overtake all other forms of government spending, leaving less for investment in necessities like infrastructure.

Gold Under Pressure, Signaling an Attractive Buying Opportunity

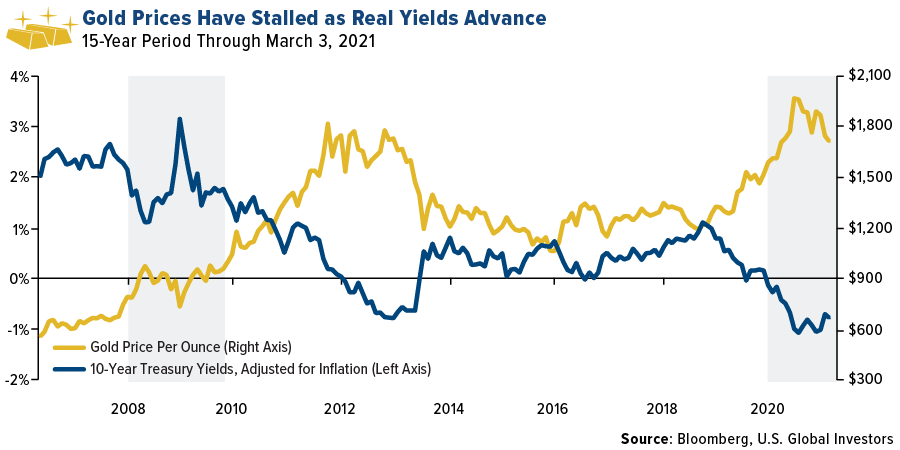

An expected consequence of higher yields? Gold prices are under pressure, having recorded their fourth straight week of losses. Gold and bond yields share an inverse relationship, as you can see below, but again, it’s real yields you want to be paying attention to. When adjusted for inflation, yields remain below zero, making the yellow metal all the more attractive.

Rising expectations for inflation are also strengthening gold’s investment case. This week, Federal Reserve Chair Jerome Powell rattled markets by saying inflation could pick up temporarily as the economy reopens from pandemic lockdowns.

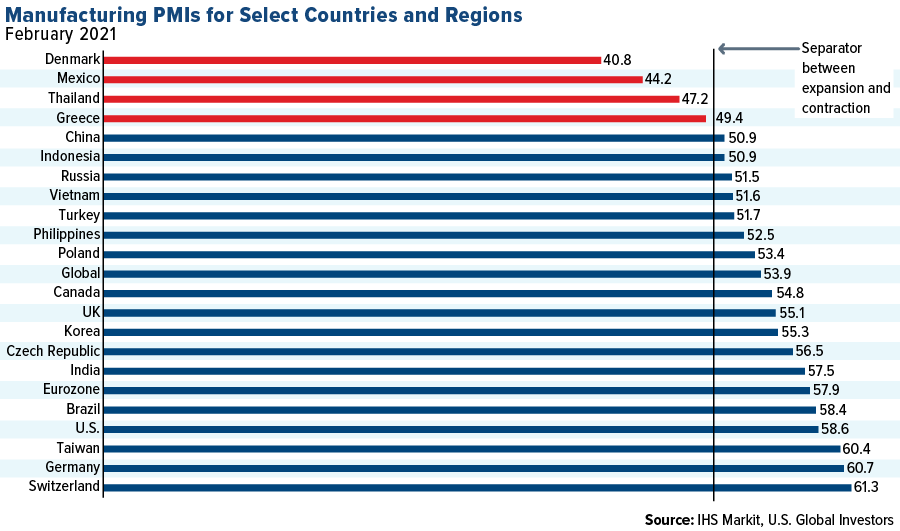

Indeed, prices for industrial metals and materials have been climbing as manufacturers around the world expand operations and the number of new orders rises. Of the 29 nations IHS Markit monitors, 23 of them, or 80%, had manufacturing PMIs above the magic 50.0 mark in February, indicating a synchronized economic recovery. The country with the lowest PMI, at 27.7, was Myanmar (Burma), which is currently mired in a violent coup.

On the service industry side, the U.S. led the world with a blistering PMI of 59.8 in February, the highest reading since July 2014.

Mark your calendar for Wednesday of next week! I’ll be participating in our next webcast, on gold and cryptos. Joining me will be HIVE Blockchain’s CFO Darcy Daubaras and Bloomberg’s Mike McGlone. I hope you can join us! To register for free, click here.

Gold Market

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Feb-28 | Caixin China PMI Mfg | 51.4 | 50.9 | 51.5 |

| Mar-1 | Germany CPI YoY | 1.2% | 1.3% | 1.0% |

| Mar-1 | ISM Manufacturing | 58.9 | 60.8 | 58.7 |

| Mar-2 | Eurozone CPI Core YoY | 1.1% | 1.1% | 1.4% |

| Mar-3 | ADP Employment Change | 250k | 117k | 195k |

| Mar-4 | Initial Jobless Claims | 750k | 745k | 736k |

| Mar-4 | Durable Goods Orders | 3.4% | 3.4% | 3.4% |

| Mar-5 | Change in Nonfarm Payrolls | 200k | 379k | 166k |

| Mar-10 | CPI YoY | 1.7% | — | 1.4% |

| Mar-11 | ECB Main Refinancing Rate | 0.000% | — | 0.000% |

| Mar-11 | Initial Jobless Claims | 725k | — | 745k |

| Mar-12 | Germany CPI YoY | 1.3% | — | 1.3% |

| Mar-12 | PPI Final Demand YoY | 2.7% | — | 1.7% |

Strengths

- The best performing precious metal for the week was palladium, up 0.60% as auto sales are expected to rise with the vaccination rollout. Silver ETFs caught a bid this week despite massive gold outflows. ETFs added 1.02 million troy ounces of silver on Thursday, bringing total net purchases to 66.7 million ounces.

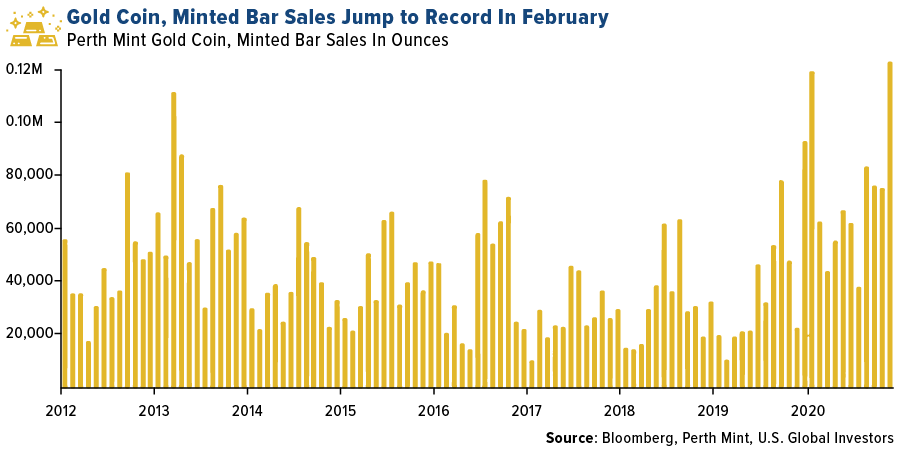

- The Perth Mint reported gold coin and minted bar sales rose 441% year-over-year in February to 124,104 ounces as investors took advantage of lower gold prices. Spot gold fell 6.2% in February, and Perth Mint saw gold product sales 63% higher than in January. The U.S. Mint also reported strong sales in February. Sales of American Eagle silver coins totaled 3.19 million ounces last month and gold coin sales rose to 125,000 ounces.

- The Perth Mint reported gold coin and minted bar sales rose 441% year-over-year in February to 124,104 ounces as investors took advantage of lower gold prices. Spot gold fell 6.2% in February, and Perth Mint saw gold product sales 63% higher than in January. The U.S. Mint also reported strong sales in February. Sales of American Eagle silver coins totaled 3.19 million ounces last month and gold coin sales rose to 125,000 ounces.

Weaknesses

- The worst performing precious metal for the week was silver, down 5.33% which followed gold lower this week. Gold fell to a nine-month low below $1,700 an ounce as rising U.S. Treasury yields remain a headwind, along with optimism of an economic recovery. Bullion is now down 11% so far in 2021.

- According to Bloomberg data, holdings in gold-backed ETFs fell more than 14 metric tons on Monday, the most in three months. Thursday was the 14th straight session of outflows – the longest streak since December 2016. “Gold’s reputation appears to have been tarnished considerably by the heavy losses of recent weeks, as evidenced by the ongoing outflows from gold ETFs,” said Commerzbank AG analyst Carsten Fritsche in a note.

- Rhodium’s surge to 27,000 an ounce is driving a surge in thefts of catalytic converters, reports Bloomberg. The byproduct of platinum and palladium production, rhodium is known for its ability to remove the most toxic pollutants from vehicle exhaust. Lara Smith, founder of mining market research group Core Consultant, says "there are certain metals that don’t follow fundamental supply and demand dynamics because nobody is going to set up a mine just for the rhodium. Rhodium will always be mined or not mined because of the platinum."

Opportunities

- One opportunity thanks to lower bullion prices: stronger retail purchases. Benchmark gold futures in India are down 20% from a record in August last year, and imports rose 412% in February from a year earlier to the highest since November 2019. “The festival and wedding season looks good,” said Ashish Pethe, chairman of the All India Gem & Jewellery Domestic

Council. India is the world’s second largest consumer of the precious metal and demand historically picks up ahead of holidays and celebrations. - Analysts at Goldman Sachs led by Jeffrey Currie said now is the beginning of a structural bull market in commodities driven by demand. "Lockdowns have driven a wedge between the consumption of services and goods, generating additional demand from both households and governments looking to stimulate activity while minimizing the virus spread.” The report continued to say “commodities are the crucial link between growing demand, a weaker

dollar and inflation, which is why they have been statistically the best hedge

against inflation.” This boost the case for investing in physical precious metals. - Citigroup head of commodities research Ed Morse said in a Bloomberg TV interview that gold could get a boost from emerging market central bank purchases. “We expect Emerging Markets central banks will buy more gold in part because of increasing concerns about where the dollar

goes.” Citigroup expects gold to hit a bottom and be supported by traditional buyers due to the change in the macro environment.

Threats

- The VanEck Vectors Junior Gold Miners (GDXJ) exchange-traded fund relative to the SPDR S&P

500 ETF Trust has broken below four Fibonacci support levels, write Bloomberg Intelligence’s Anthony Feld and Mike McGlone. This is a bearish signal and shows gold stocks aren’t acting like the inflation hedge that they’ve historically served. Like the rapid sell off with the nationwide lockdowns back in March of 2020, risk parity trades had to be unwound. Gold is often held alongside these trading strategies but when markets are stressed, gold positions also get liquidated as the risk parity trade is taken off. Gold rallied very strongly out of the market bottom, finishing the year strongly. - Gold’s biggest threat remains rising bond yields. The 10-year Treasury yield continues to surge, hitting 1.6% Friday morning after a stronger-than-expected jobs report. Gold and bond yields historically share a strong inverse relationship.

- U.S. oil futures rose above $65 a barrel on Friday and Brent rose toward $70. Higher oil prices are a headwind for precious metal miners who use the fuel at operations. Oil has recovered globally as producer work to keep supply limited while demand increases post-lockdown.

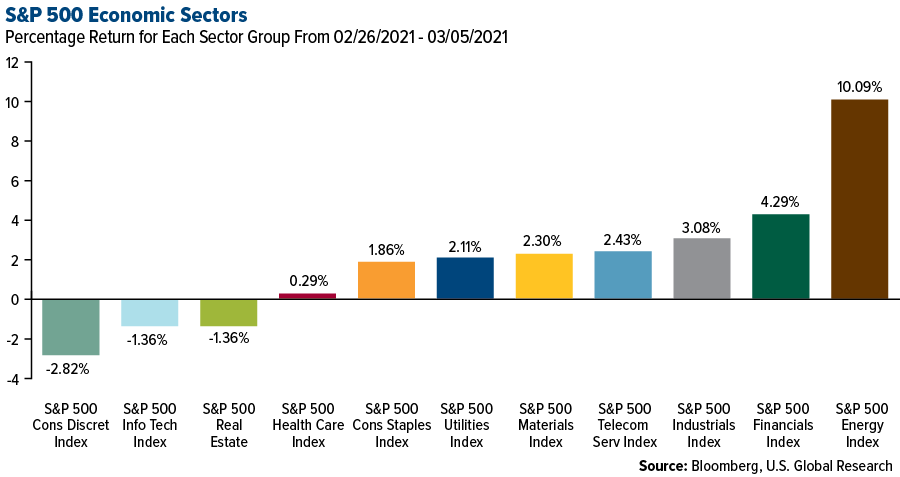

Index Summary

- The major market indices finished mixed this week. The Dow Jones Industrial Average gained 1.82%. The S&P 500 Stock Index rose 0.80%, while the Nasdaq Composite fell 2.06%. The Russell 2000 small capitalization index lost 0.40% this week.

- The Hang Seng Composite lost 0.66% this week; while Taiwan was down 0.62% and the KOSPI rose 0.44%.

- The 10-year Treasury bond yield rose 16 basis points to 1.567%.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performer for the week was Chiliz, rising 109.89%.

- Good Works Acquisition, a special purpose acquisition company (SPAC), is merging with Cipher Mining Technologies, a unit of the BitFury Group. The combined company’s enterprise value is said to be $2 billion and Cipher expects to reach mining capacity of 745 megawatts by the end of 2025 and industry leading cost of energy of approximately 2.7c/kWh. BitFury, which makes hardware for Bitcoin mining and provides blockchain software and services, is positioned to improve Cipher’s access to relevant hardware, maintenance, and management. The combined company is set to receive proceeds of $595 million when the deal closes in the second quarter of 2021.

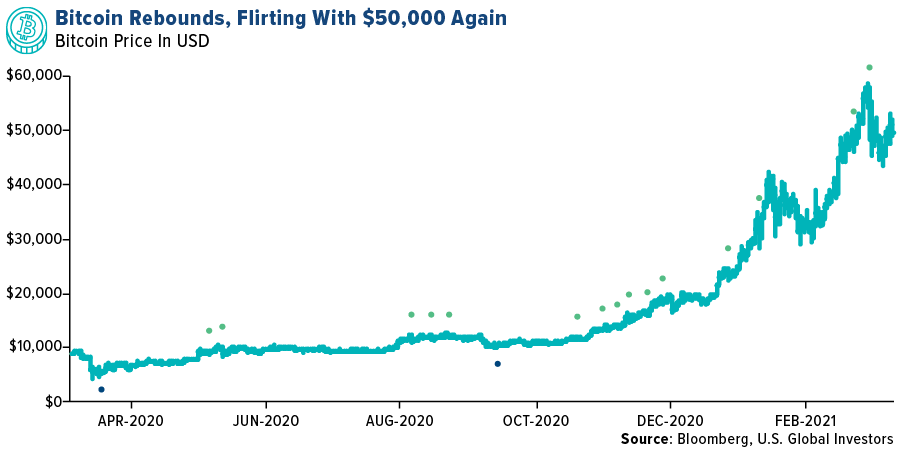

- As Bitcoin is finding a new base, bulls believe that Grayscale Bitcoin Trust’s (GBTC) premium flipping negative is a signal of continuation of the bull cycle. GBTC shares are trading at a discount to their net asset value and this “negative premium” was also observed in March 2020, the start of the bull cycle that has brought BTC/USD from $3,600 to $58,300. With an increase in investment products designed to provide exposure to the cryptocurrency, market sentiment seems set to drive Bitcoin higher.

click to enlarge

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week was 1inch, down 25.45%.

- According to a recent survey done by JPMorgan, a large majority of institutional investors do not plan on investing in or trading cryptocurrencies. 78% of the survey respondents said that it was unlikely that their firm will invest in or offer trading services for digital assets. Around 58% of the respondents do believe that cryptocurrencies are here to stay while 21% believe that they are a “temporary fad.” The survey included 3,400 investors representing 1,500 different institutions.

- Binance is mulling new marketplace controls after a single large order triggered a flash crash in Polkadot trading contracts. The world’s biggest cryptocurrency exchange reported that prices of the quarterly perpetual-futures contracts on Polkadot tumbled 99.2% in less than a minute. Within that time, around $18 million contracts were traded on the exchange. According to Binance, this flash crash was caused by an individual who had put a stop market order on their large position that exceeded the total available bids in the market.

Opportunities

- Crypto.com, the Hong Kong based cryptocurrency exchange, announced that it is launching a $200 million venture arm dedicated to investing in crypto startups. Crypto.com Capital, the venture arm, will invest in startups and projects at seed and Series A stages. They are planning on leading funding rounds with investments of between $100,000 and $3 million at seed stage and between $3 million and $10 million at Series A. The firm believes that crypto startups will rely on Crypto.com Capital to move fast and provide both capital and access to a global user base.

- Mark Cuban announced that his NBA team, the Dallas Mavericks, will be accepting Dogecoin as payment for tickets and merchandise as part of an agreement with crypto payment services provider BitPay, as the provider begins to offer the cryptocurrency as a form of payment to its customers.

- BitMEX, the cryptocurrency exchange, is planning on adding spot trading, brokerage, and custody services to its offerings. The company’s new CEO, Alexander Höptner, joined in December and he is working to transform BitMEX by amending relationships with regulators and expanding business operations. As the company battles charges regarding unregistered trading, Höptner’s experience working for a German exchange will be crucial to amend the wrongdoings of BitMEX’s former CEO.

Threats

- The Ministry of Finance of Vietnam has warned the public about the risks of cryptocurrency investments and stated that the country has not adopted any legislation related to the issuance, trading, and exchange of digital currencies and assets. These warnings come amidst reports of growing skepticism regarding Pi Network, a new cryptocurrency platform that is becoming increasingly popular in the region, which has some worried that it could be a pyramid scheme.

- The Biden administration will have to decide the fate of last-minute rules proposed by the former Trump administration that would require financial services firms to record the identities of cryptocurrency holders. If adopted, these measures could lead to a plummet in cryptocurrency prices. The rules were proposed to suppress attempts of using the digital assets for money laundering and illegal activities.

- Ethereum’s network is scheduled to have an upgrade in July 2021, which may result in the cryptocurrency becoming a deflationary asset. The EIP-1559 fee market overhaul will transition Ethereum’s fee structure away from a bidding system that allows miners to prioritize the highest bids. After the implementation of EIP-1559, the network will dynamically adjust fees so users only pay the lowest bid for each block. This might reduce the revenue and margins earned by Ethereum miners and will certainly have an impact on share prices of publicly traded cryptocurrency mining companies.

Domestic Economy and Equities

Strengths

- Hiring surged in February as economic activity picked up with Covid-19 cases steadily dropping and vaccine rollouts providing hope for more growth. The Labor Department reported Friday that nonfarm payrolls jumped by 379,000 for the month and the unemployment rate fell to 6.2%.

- Manufacturing output in February headed up from January on the way to its highest level in a year, according to data from the Institute for Supply Management (ISM). In its monthly Manufacturing Report on Business, ISM said that the report’s key metric, the PMI, was 60.8, which was 2.1% higher than January’s 58.7.

- Fox Corp was the best performing S&P 500 stock for the week, increasing 23.96%. The stock rose to its highest in two years as BofA boosted its price target to a Street-high $54 from $39, touting “hidden assets” like its online betting opportunity. Analyst Jessica Reif Ehrlich said Fox has exposure to online betting through its 2.5% equity stake in Flutter Entertainment, an 18.5% equity option in FanDuel Group and an option to own 50% of Stars Group’s U.S. operations.

Weaknesses

- Climate change and revenue sources are set to be some of the key divisions between Republicans and Democrats as they start discussions on a bipartisan infrastructure package. Members of the GOP are calling for a modest package that’s limited to traditional infrastructure and includes funding offsets.

- Record imports pushed the U.S. trade deficit to $68.2 billion in January, up from a revised $67 billion in December.

- Enphase Energy Inc was the worst performing S&P 500 stock for the week, decreasing 18.47%. The stock fell as growth sectors such as clean energy got embroiled in the equity selloff spurred by rising bond yields.

Opportunities

- The European Union and the U.S. agreed to suspend tariffs on billions of dollars of each other’s products, easing a 17-year transatlantic dispute over illegal aid to the world’s biggest aircraft makers. President Joe Biden and European Commission President Ursula von der Leyen agreed to the move on a call Friday, the commission said in a statement. Some of the companies affected by the tariffs — among the largest approved by the WTO to date — include European luxury brand owners such as LVMH Moet Hennessy Louis Vuitton SE that owns Givenchy and Fendi, alcoholic-beverage maker Bacardi Ltd., Caterpillar Inc. and Microsoft Corp.

- Yields on 10-year benchmark tax-exempt bonds edged lower Friday by about one basis point to 1.07%, a 4 basis-point drop since the end of last week, according to Bloomberg’s BVAL indexes. Yet those on comparable Treasuries have jumped about 14 basis points to 1.55% over that time. The result: municipal bonds have eked out a small gain this month while Treasuries and corporate debt have lost 0.81% and 1.26%, respectively.

- Roku was upgraded by KeyBanc analyst Justin Patterson to overweight from sector weight with a $518 price target. The analyst said the streaming platform "is becoming a key enabler of the direct-to-consumer video ecosystem."

Threats

- Stocks sharply sold off alongside spiking 10-year Treasury yields on Thursday after Fed Chair Jerome Powell refrained from outlining specific steps to rein in what he described as "disorderly" markets.

- After bond market liquidity dramatically disappeared a year ago, the Fed let banks stop factoring in Treasuries to their so-called supplemental liquidity ratios — letting them stockpile U.S. debt without breaking regulations. That exemption expires March 31, and central bankers have given no indication it’ll get authorized for longer. The impending expiration, some say, is a reason why Treasuries just suddenly got so volatile.

- Lockheed Martin Corp.’s F-35 Joint Strike Fighter program—the costliest U.S. weapons system—will be in the crosshairs this year as Congress works on the fiscal 2022 defense budget, the leader of the House Armed Services Committee said. Rep. Adam Smith (D-Wash.) said Friday that he’s looking for the most “cost-effective” mix of fighter aircraft. “I want to stop throwing money down that particular rathole,” Smith said of the F-35 program, speaking at an event hosted by the Brookings Institution.

Energy and Natural Resources Market

Strengths

- The best performing commodity for the week was crude oil, up 7.80%. Oil prices rallied in part due to an agreement amongst OPEC+ nations retain supply curbs on production until they see global oil demand rising.

- OPEC+ has agreed to a production increase this week as it seeks to cool the rapid rally in crude prices. The cartel has a consensus that the global markets can absorb additional barrels and that all members are ready to increase production. This news resulted in an eventual increase of more than 10% in oil prices. OPEC’s Secretary General said that the global economic outlook and oil markets continue to show signs of improvement and that the uncertainties which shocked and disrupted the market in 2020 continue to abate. OPEC is set to debate whether the cartel will proceed with a 500,000 barrel-a-day collective output hike in April and how Saudi Arabia will phase out the extra supply reduction of 1 million barrels-a-day it has been making voluntarily in February and March.

- China is set to offer new capital for the development of nuclear power as a key tool in its drive to cut carbon emissions. The country is planning on constructing coastal nuclear power plants and aims to have 70 gigawatts of generation capacity by 2025, up from about 50 gigawatts reported at the end of 2020. This decision comes on the back of China’s goal to lift the share of non-fossil fuel energy sources to 20% by 2025. China is expected to surpass France and then the U.S. to become the world’s biggest nuclear generator this decade, as government researchers in China believe that the nation’s nuclear capacity could rise to more than 130 gigawatts by 2030.

Weaknesses

- The worst performing commodity for the week was nickel, down 13.19%. Nickel slumped in part by a rise in inventories, tracked by the London Metal Exchange, and the announcement by China’s Tsingshan Holding Group Co. to increase the metal’s supply.

- Potomac Economics, an independent market monitor hired by the state of Texas to assess the Electric Reliability Council of Texas’ (ERCOT) performance following failure of the power grid in February, stated that ERCOT’s decision to set the price of electricity at $9,000 per megawatt hour for multiple days was a mistake and an unnecessary move. In a letter to the state regulators, Potomac recommended that the pricing should be corrected retroactively and that $16 billion in charges be reversed. This price hike brought massive power bills to firms, one of them being Brazos Electric Power Cooperative which was charged $2.1 billion and has filed for bankruptcy.

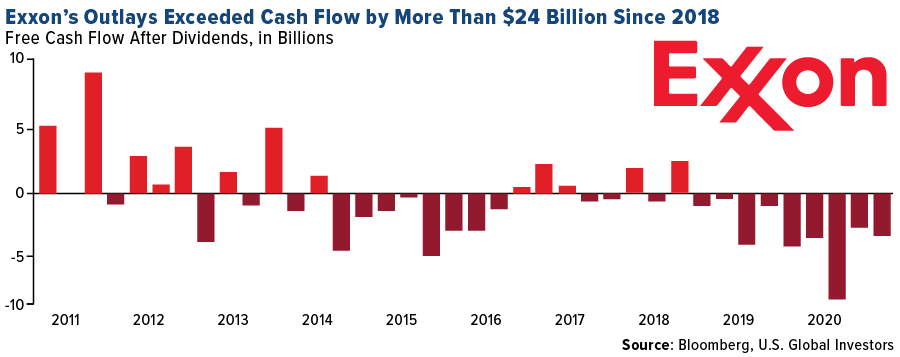

- Exxon Mobil is planning on targeting returns of at least 30% on new projects after reducing its capital spending plans. The oil giant was hit hard by the pandemic as its stock plunged 41% and CEO Darren Woods moved to cut costs and reduce long-term capital spending in a bid to boost near-term returns. Exxon still faces challenges as the company has burned through more than $24 billion of cash in the past three years, as low oil prices hit at a time when it was in the middle of a high-spend investment plan, and must deal with record debt of $70 billion, which has nearly doubled since 2018.

Opportunities

- Stelco Holdings Inc.’s CEO, Alan Kestenbaum, believes that there is going to be a historic rebound in global economies that will drive a surge in steel demand. He credits the company’s revised optimism on better visibility of upcoming U.S. car sales and pickup in oil drilling. The Steel Price Index reached the highest levels since March 2019 this week.

- Saudi Aramco has made a deal with South Korea to ship gas to the island nation. The liquefied petroleum gas will be converted into hydrogen, by Hyundai OilBank Co., to be used at desulfurization facilities and power vehicles. Carbon dioxide, a by-product of the conversion process, will be transported back to Saudi Arabia where it will be used by Aramco to pump more oil out of the ground in a process known as enhanced oil recovery. This deal banks on the idea that shipping LPG to South Korea and carbon dioxide back to Saudi Arabia will be cheaper than directly shipping hydrogen to South Korea.

- John Kerry, the U.S. Presidential Climate Envoy, said that the U.S. oil and gas industry should embrace opportunities in producing and transporting hydrogen, with the goal to use the energy source to fuel long-haul trucks and supply power globally. As hydrogen is currently extracted from gas, there is a push to use renewable energy to make hydrogen from water to reduce carbon emissions. Kerry also mentioned that the Biden administration will push China, which accounts for 30% of the world’s total emissions, on the issue of climate change and that climate change will be dealt as a compartmentalized issue. He believes that there will be about $6 trillion a year of economic transfer taking place in the clean energy technology sector.

Threats

- Over half of U.S. farmers, whose livelihoods depend on producing the nation’s meat, expect plant-based faux meat to command as much as 10% of the total protein market by 2025. U.S. farmers’ worries about substitutes comes at a time when there are expectations of more stringent environmental regulations and potentially higher taxes under President Biden’s administration. Faux meat, which made up about 1.5% of total meat sales at retail by the end of 2020, has not yet taken a significant market share but remains an issue for thousands of farmers in the country.

- Companies and trade associations in the electronics manufacturing and distribution sectors are pleading the Environmental Protection Agency (EPA) for a regulatory reprieve so that companies can ship parts and make products while seeking alternatives for a chemical largely banned as of March 8. Known as PBTs, these chemicals persist in the environment, build up in the food chain, and are toxic. PBTs were recognized as hazardous as part of the 2016 Toxic Substances Control Act. The companies are concerned as there are no guidelines regarding orders that were placed months ago and are now arriving at the docks, which could bring additional costs and potentially disrupt the supply chains of thousands of companies.

- European companies are getting increasingly concerned about the surging costs of carbon emissions, saying that these costs will hurt their competitiveness. Price of carbon has jumped about 30% in the past six months, in part due to the speculation by hedge funds. The pace of gains and expectations by hedge funds that the price might double this year has led to discussions whether the EU should intervene and propose measures to limit speculation. Former senior climate officials at the European Commission have voiced their concern on such measures, saying that the European carbon market has never been more important as an instrument to secure emission reductions cost effectively and that a higher carbon price is crucial to drive change and innovation.

Airline Sector

Strengths

- The best performing airline stock for the week was International Consolidated Airlines, up 14.2%. Global demand for air cargo services is back at pre-pandemic levels, according to the International Air Transport Association. Demand in January rose 3% from December and was 1.1% higher than in January 2019 – a rare sign of hope for carriers. IAG said 2020 was a record year for cargo revenue.

- The Boeing 737 MAX is picking up steam once again. United Airlines increased its orders from 155 to 180. United already has 30 MAX in its fleet and expects to receive another 24 this year.

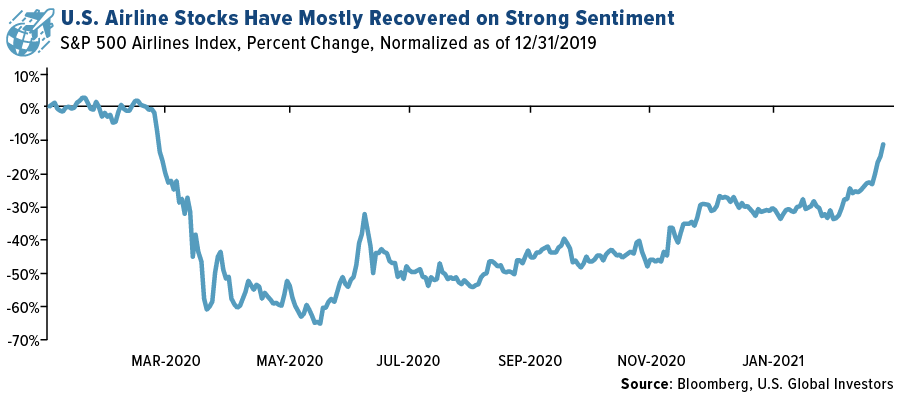

- Weekly airline traffic was most recently up 35%. Flight schedules will be at 85% of 2019 levels by April. The percentage of parked aircraft is now 32%, as opposed to 65% at the peak of the pandemic. Airline stocks are recovering on strong sentiment surrounding vaccine distribution.

Weaknesses

- The worst performing airline stock for the week was GOL, down 15.3%. European Airlines have been cutting back flight schedules, down to just 1,500 flights per day, which is 20% below recent weeks’ levels. SAS, for example, in February reported an 89% drop in traffic. The load factor dropped 40.6%, to 25.9%. Lufthansa has been cutting back long-haul routes. Finn Air in February reported traffic down 96% and a 50% drop in load factor, to 26.6%.

- Thai Air is seeking a capital infusion of $1.65 billion to keep afloat along with a debt restructuring and 50% layoffs. It must be presented to the bankruptcy court. The country’s finance ministry, who is also the largest shareholder, has expressed some support for the plan.

- The FBI confirmed that it is aware of a long cylindrical object that had a close encounter with an American Airlines flight at 36,000 feet above the northeast corner of New Mexico. The plane was travelling at 460 miles per hour when an object they described as a “cruise missile” passed over them.

Opportunities

- Delta Air Lines CEO Ed Bastian said on Bloomberg TV he expects summer travel in the U.S will be robust. “We know that consumers in the U.S. have a considerable amount of pent-up demand.” Although traffic is still below pre-pandemic levels, positive sentiment is growing as more Americans obtain the COVID vaccine and feel safe traveling again. Many airlines are adding flights to travel hubs and emphasizing leisure routes.

- Qantas is selling $577 mystery flights to unknown destinations between March and May. These are one day trips and two-hour flights and limited to 120 passengers. Qantas has been one of the more creative carriers in incentivizing passengers to fly.

- Air Canada is transferring its entire Air Canada Express fleet of E175 to Jazz. The carrier expects to realize C$400 million lower costs over the next 15 years.

Threats

- Czech Airlines, which is nearly insolvent, has asked a Prague court to allow a restructuring related to a drop in travel demand, but the state has refused to participate.

- Singapore Air is still burning through cash. Nearly $8.2 billion was burned out of the $8.8 Singapore rights issue that recently occurred. The company still has $2.1 billion Singapore dollars’ worth of credit lines if needed.

- The industry is still facing “Karen” issues. A Frontier Airlines flight from Miami to New York was cancelled due to several adult passengers refusing to wear masks. Federal mandates are in place requiring the use of masks.

Emerging Markets

Strengths

- The best performing country in emerging Europe for the week was Turkey, gaining 4.8%. The best performing country in Asia this week was Thailand, gaining 3.2%.

- The Russian ruble was the best performing currency in emerging Europe this week, gaining 41 basis points. The Pakistani rupee was the best performing currency in Asia this week, gaining 1.3%.

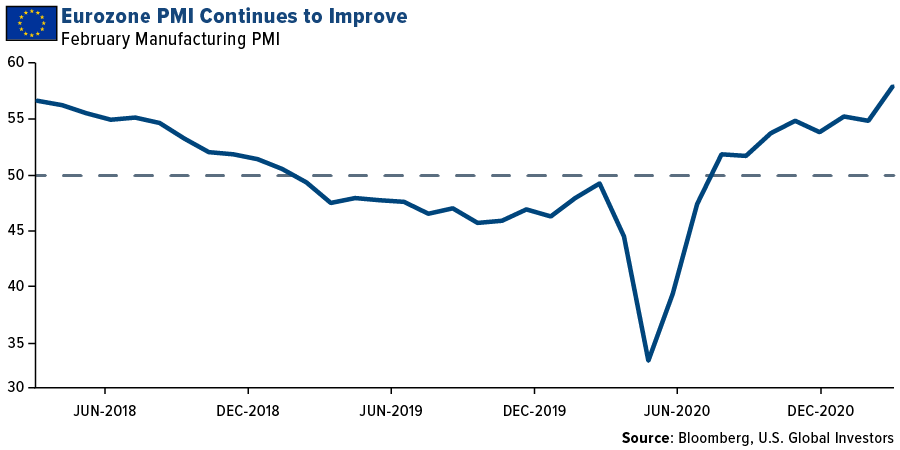

- Eurozone Manufacturing PMI increased to 57.9 in February from 54.8 in January. Output and new orders were up sharply as the export trade strengthened. Germany Manufacturing PMI hit a 37-month high at 60.7. The Netherland’s rose to a 29-month high at 59.6. Austria rose to a 36-month high at 58.9. Italy rose to a 37-month high at 56.9. France rose to a 37-month high at 56.1. However, Greece and Hungary dropped to 49.4, below the 50 level that separates growth from contraction.

Weaknesses

- The worst performing country in emerging Europe for the week was Hungary, losing 1.1%. The worst performing country in Asia this week was Taiwan, losing 62 basis points.

- The Polish zloty was the worst performing currency in emerging Europe this week, losing 2.9%. The Malaysian ringgit was the worst performing currency in Asia, losing 60 basis points.

- China Manufacturing PMI declined to 50.6 in February from 51.3 in January, below the expected reading of 51.0. China Non-Manufacturing PMI dropped to 51.4 from 52.1, below the expected reading of 52.0.

Opportunities

- China is preparing to launch a large investment into domestic technology and innovation as it looks to become less dependent on the Unites States and its allies. China’s new policy to shift away from the Unites States is likely to increase China’s imports from countries other than the U.S. providing opportunities for countries like Germany and South Korea who specialize in production of technology and electronic equipment.

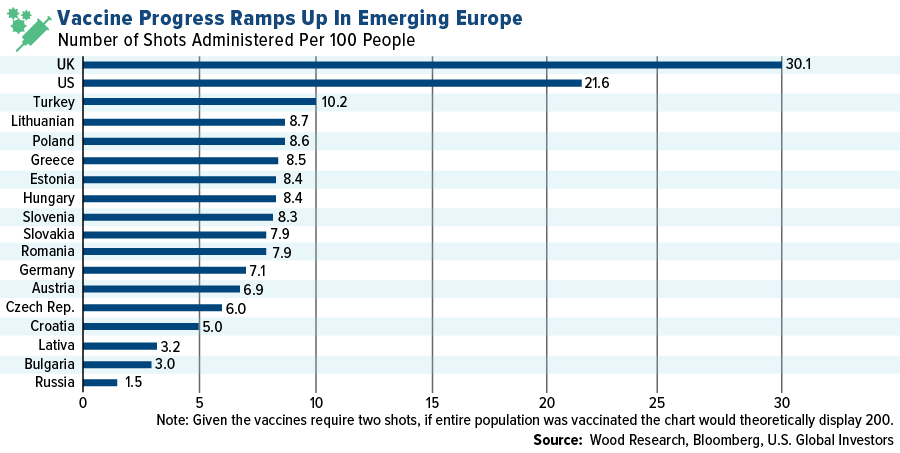

- According to Wood & Company research team, the United Kingdom is the most efficient at distributing the coronavirus vaccine, administering 30.1 shots per 100 people, followed by the United States. Within central emerging Europe, Turkey is the most efficient with 10.2 shots, followed by Lithuania. Russia is the biggest laggard, administering only 1.5 shots per 100 people.

- China set its 2021 growth target at 6% and announced its plan to create 11 million jobs for cities. The 6% growth target announced by the government is conservative as most economists’ project the Chinese economy to grow more than 8% this year.

Threats

- The U.S. Treasury yields are moving higher, and during the period of rising rates equities usually underperform. Also, the dollar may continue to strengthen, devaluating emerging market currencies. The rising price of Brent will increase energy bills for many emerging market countries who depend on energy imports. The Turkish lira is especially vulnerable to rising oil prices.

- The number of coronavirus infections keeps rising in many countries. The Czech Republic and Hungary announced a spike in infections. Hungary imposed a nationwide lockdown this week, shutting down businesses and restricting people from travel. The Athens area in Greece, home to 4 million people, is running out of intensive care beds and the medical sector is running close to its full capacity.

- The Eurozone and the United States imposed sanctions on Russian individuals, and more than a dozen businesses, related to the poisoning and jailing of opposition leader Alexei Novalny. Regardless of the actions taken by the West to punish Russia, the Moscow Stock Exchange moved higher and the Russian ruble was little change in the past five days. However, the United Kingdom and Biden’s Administration may be preparing a new set of sanctions targeting Russia’s financial market next.

Leaders and Laggards

| Index | Close | Weekly Change($) |

Weekly Change(%) |

|---|---|---|---|

| 10-Yr Treasury Bond | 1.57 | +0.16 | +11.37% |

| Oil Futures | 66.30 | +4.80 | +7.80% |

| Hang Seng Composite Index | 4,554.96 | -30.36 | -0.66% |

| S&P Basic Materials | 471.73 | +10.62 | +2.30% |

| Korean KOSPI Index | 3,026.26 | +13.31 | +0.44% |

| S&P Energy | 396.54 | +36.35 | +10.09% |

| Nasdaq | 12,920.15 | -272.20 | -2.06% |

| DJIA | 31,496.30 | +563.93 | +1.82% |

| Russell 2000 | 2,192.21 | -8.84 | -0.40% |

| S&P 500 | 3,841.78 | +30.63 | +0.80% |

| Gold Futures | 1,696.50 | -32.30 | -1.87% |

| XAU | 133.58 | +2.79 | +2.13% |

| S&P/TSX VENTURE COMP IDX | 918.36 | -100.14 | -9.83% |

| S&P/TSX Global Gold Index | 280.10 | +10.68 | +3.96% |

| Natural Gas Futures | 2.70 | -0.07 | -2.45% |

| Index | Close | Monthly Change($) |

Monthly Change(%) |

|---|---|---|---|

| Korean KOSPI Index | 3,026.26 | -103.42 | -3.30% |

| 10-Yr Treasury Bond | 1.57 | +0.43 | +37.58% |

| Gold Futures | 1,696.50 | -138.60 | -7.55% |

| S&P Basic Materials | 471.73 | +14.94 | +3.27% |

| S&P 500 | 3,841.78 | +11.61 | +0.30% |

| DJIA | 31,496.30 | +772.70 | +2.52% |

| Nasdaq | 12,920.15 | -690.39 | -5.07% |

| Oil Futures | 66.30 | +10.61 | +19.05% |

| Hang Seng Composite Index | 4,554.96 | -190.94 | -4.02% |

| S&P/TSX Global Gold Index | 280.10 | -25.15 | -8.24% |

| XAU | 133.58 | -6.05 | -4.33% |

| Russell 2000 | 2,192.21 | +32.51 | +1.51% |

| S&P Energy | 396.54 | +81.79 | +25.99% |

| S&P/TSX VENTURE COMP IDX | 918.36 | -60.58 | -6.19% |

| Natural Gas Futures | 2.70 | -0.09 | -3.08% |

| Index | Close | Quarterly Change($) |

Quarterly Change(%) |

|---|---|---|---|

| XAU | 133.58 | -6.02 | -4.31% |

| S&P/TSX Global Gold Index | 280.10 | -36.65 | -11.57% |

| Gold Futures | 1,696.50 | -148.20 | -8.03% |

| DJIA | 31,496.30 | +1,526.78 | +5.09% |

| S&P 500 | 3,841.78 | +175.06 | +4.77% |

| Nasdaq | 12,920.15 | +542.97 | +4.39% |

| Korean KOSPI Index | 3,026.26 | +330.04 | +12.24% |

| Natural Gas Futures | 2.70 | +0.20 | +7.82% |

| S&P Basic Materials | 471.73 | +30.97 | +7.03% |

| Russell 2000 | 2,192.21 | +343.51 | +18.58% |

| Oil Futures | 66.30 | +20.66 | +45.27% |

| Hang Seng Composite Index | 4,554.96 | +375.92 | +9.00% |

| S&P/TSX VENTURE COMP IDX | 918.36 | +149.06 | +19.38% |

| S&P Energy | 396.54 | +109.20 | +38.00% |

| 10-Yr Treasury Bond | 1.57 | +0.66 | +72.77% |

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission ("SEC"). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (12/31/2020):

United Airlines Holdings Inc

American Airlines Group Inc

Delta Air Lines Inc

Qantas Airways Ltd

Air Canada

Singapore Airlines Ltd

LVMH

Microsoft Corp

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment. The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index. The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges. The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

To help drivers identify the states that provide the best commuting conditions, WalletHub compared the 50 states across four key dimensions: 1) Cost of Ownership & Maintenance, 2) Traffic & Infrastructure, 3) Safety and 4) Access to Vehicles & Maintenance. WalletHub then evaluated those dimensions using 31 relevant metrics, with each metric graded on a 100-point scale. Standard deviation, also known as sigma, is a measure of the dispersion of a set of data from its mean. The more spread apart the data, the higher the deviation. Standard deviation is also known as historical volatility.