Investor Alert

Decrypting Bitcoin and Gold

Date Posted: August 13, 2021

Read time: 43 min

As I discussed in a Frank Talk last week, the Senate just approved a $1 trillion infrastructure bill that’s now the business of the House.

As I discussed in a Frank Talk this week, the Senate just approved a $1 trillion infrastructure bill that’s now the business of the House. Among the parts of the bill that I seriously hope lawmakers will consider amending is the part that creates new tax reporting requirements for the cryptocurrency industry.

Specifically, the bill would require crypto “brokers” to provide the names and addresses of their clients. At issue is the vague way in which the bill’s authors define a crypto broker, which would unintentionally include not just brokers such as Coinbase but also crypto miners, software developers and more. These types of companies do not keep track of who owns the Bitcoin, Ether or other cryptos they may have mined. Doing so, in fact, would be impossible.

This legislation is a prime example of what happens when lawmakers try to regulate something they don’t fully understand.

A video of Ted Cruz went viral on Reddit this week after the Texas senator made a full-throated defense of his amendment, which would strike all language related to cryptos from the bill. “There aren’t five senators within this body with any real understanding of how cryptocurrency operates,” Cruz said, and yet lawmakers were willing to “obliterate” this “new and exciting,” “fast moving” industry. We would be destroying billions of dollars in value and sending countless jobs overseas, he argued.

Cruz can be a polarizing figure, and I may not always agree with him or his methods, but here he’s 100% correct. I hope his words can convince House members to amend the bill’s language or remove it altogether.

That said, I believe most leaders in the crypto industry would invite some level of regulation, so long as it’s reasonable and drafted from a place of understanding.

You can watch Ted Cruz’s full speech by clicking here.

Both Bitcoin and Gold Are Money

It’s not just lawmakers who aren’t fully versed in Bitcoin, of course. I’ve received many questions over the past few days regarding the differences between the crypto and gold. With that in mind, below are six reasons why both Bitcoin and gold can be considered money.

1. Durability

Ideally, money should be able to withstand basic wear and tear, one of the main reasons why many currencies have historically been made of metal, shells and other hardy materials. A few years ago, I shared with you why we can single gold out among the 118 elements as the best possible candidate to be money. It’s chemically inert, for one, meaning it doesn’t rust or tarnish. You can bend it, break it and melt it down, but it’s virtually impossible to destroy. Since humans started mining the metal between 5,000 and 7,000 years ago, we’ve dug up close to 200,000 tonnes, nearly all of it still around in one form or another.

We can also call Bitcoin a durable asset, capable of withstanding the test of time. BTC exists only in digital space, on a highly encrypted, decentralized peer-to-peer network.

2. Portability

In order for money to be a convenient medium of exchange, it needs to be portable. This is why land, although inherently valuable and durable, cannot be considered money.

In order for money to be a convenient medium of exchange, it needs to be portable. This is why land, although inherently valuable and durable, cannot be considered money.

Granted, not every form of gold is “portable.” A bar of the stuff, for instance, weighs about 27.5 pounds, making it impractical to carry around with you during a shopping spree. Gold coins, on the other hand, can be carried in a pocket or purse. And remember that not too long ago, U.S. bank notes, which are light and can fit in a wallet, were fully backed by and convertible into gold.

BTC is extremely portable because, well, it has no physical form. So long as you have a smartphone with access to the internet, you can carry as many or as few bitcoins around with you.

3. Divisibility

Money must be divisible into smaller denominations; otherwise, you’re throwing a lot of it away if you don’t use exact change. Because of its softness and malleability, gold is easily divided into smaller denominations, including 1/2, 1/4, 1/10 and even 1/20 of an ounce.

As I write this, one bitcoin is valued at around $46,000. Fortunately for those who may not have that kind of cash on hand, BTC can be purchased in fractions. What’s more, the growing number of companies that accept BTC as a form of payment will provide change.

4. Uniformity

Gold maintains a reliable level of uniformity. Regardless of which country’s mint you might purchase a one-ounce gold coin from, it should have more or less the same value in markets all around the world.

It’s possible that, in the future, traders may be interested in paying a premium on bitcoins that were mined using only green energy, or on newly minted bitcoins that have no history of being used to launder money or finance illicit activities, but for now, bitcoin equals one bitcoin.

5. Limited supply

Gold is attractive as money because its supply is limited. Indeed, we may very well have reached peak gold. Meanwhile, bank notes continue to be printed at a rapid rate, which has contributed to the higher-than-average inflation we’re witnessing right now.

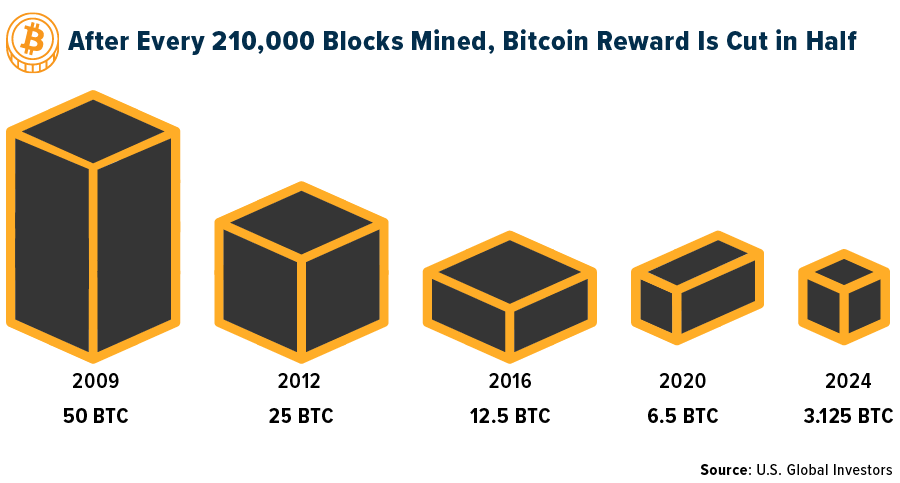

Like gold, Bitcoin has a limited supply baked into it. Only 21 million coins will ever be mined. Supply growth is also restricted by halving events. After every 210,000 blocks are mined, the Bitcoin reward is cut in half.

6. Acceptability

It’s difficult to call an asset money if not everyone agrees that it has value. Using this yardstick, gold is undeniably money. Nearly every central bank on earth holds the precious metal in its reserves, and some countries have used these holdings to pay down their debts.

Not all central banks are totally sold on Bitcoin, of course, and to date, only one country, El Salvador, has adopted Bitcoin as legal tender. Interestingly, that’s one more country than those that use gold as legal tender. Also consider that Bitcoin can be sent anywhere in the world, from peer to peer, and it will still have value.

This Is Your Last Chance!

I’m excited to share with you that the MicroStrategy founder and CEO will join me in my next webcast on gold and Bitcoin, to be held Wednesday, August 18. Most slots have already been taken! To get the link to book your spot for this exclusive conversation, email me at

info@usfunds.com with the subject line “Michael Saylor webcast.” Demand has been higher than even I anticipated, so don’t hesitate to register!

Index Summary

- The major market indices finished mixed this week. The Dow Jones Industrial Average gained 0.87%. The S&P 500 Stock Index rose 0.71%, while the Nasdaq Composite fell 0.09%. The Russell 2000 small capitalization index fell 1.10% this week.

- The Hang Seng Composite rose 1.10% this week; while Taiwan was down 3.10% and the KOSPI fell 3.03%.

- The 10-year Treasury bond yield fell a basis point to 1.283%.

Airline Sector

Strengths

- The best performing airline stock for the week was xxxx, up xx.x%. European airline bookings improved last week, with week-on-week growth in intra-Europe and international flights being boosted by the easing of U.K. travel restrictions. Intra-Europe net sales were up by 4 points to -39% versus 2019 (and compared to -43% in the prior week). The U.K. government updated its country list for travel last week, adding seven countries to the “green list,” including Germany, Austria, and Norway.

- European flight activity increased by 3 points to -29% versus 2019 (and compared to -32% in the prior week). Wizz Air increased the most by 7 points and is now at 99% of 2019 levels. Ryanair was up by 5 points, while most other airlines grew by 2-3 points.

- Azul Brazilian Airlines’ second quarter results were slightly ahead of consensus, driven by strong passenger and cargo revenue performance. Additionally, Azul noted acceleration in the demand recovery over the last several weeks including an increase in fares. Notably, booked leisure and corporate fares are currently all higher than 2019 levels.

Weaknesses

- The worst performing airline stock for the week was xxx, down x.x%. Bank of America says that system net sales decelerated for the second straight week to down 51.9% versus 2019. Travel companies have started calling out the delta variant on earnings calls over the past week. Domestic tickets sold were down 23.6% (versus down 19.0% last week) and international tickets sold slightly stepped back to down -44.3% (versus -43.3% last week). Domestic tickets sold through online channels took a sizable step back to +1.6% versus 2019 (and compared to +9.3% last week).

- GOL Airlines reduced its guidance. The revenue outlook for the third quarter came in below recently lowered expectations as well as consensus, while the implied fourth quarter improvement appears to require a confluence of very favorable developments beyond seasonality. GOL’s third quarter revenue outlook of -51% year-to-year came in below the prior -44% estimate.

- The number of seats being offered by airline carriers in China dropped by the most since early in the pandemic, as rising cases of the delta variant spurred fresh restrictions on movement. Seat capacity plunged 32% in one week, hastening a decline in the country that began at the end of July, based on data from aviation specialist OAG.

Opportunities

- SkyWest announced an agreement with Delta Air Lines to replace 16 CRJ-900s under capacity purchase agreements (CPAs) that are set to expire starting in the second half of 2022 through early 2023, with 16 new E-175s under long term contracts (likely 9-12 years). The E-175s are scheduled for delivery starting in the second quarter of 2022 and expected to be placed into service during year-end 2022.

- Fewer flights in China should translate to 130,000 barrels per day less of jet fuel being consumed. This could lead to lower prices for jet fuel, which is a key cost component for airlines.

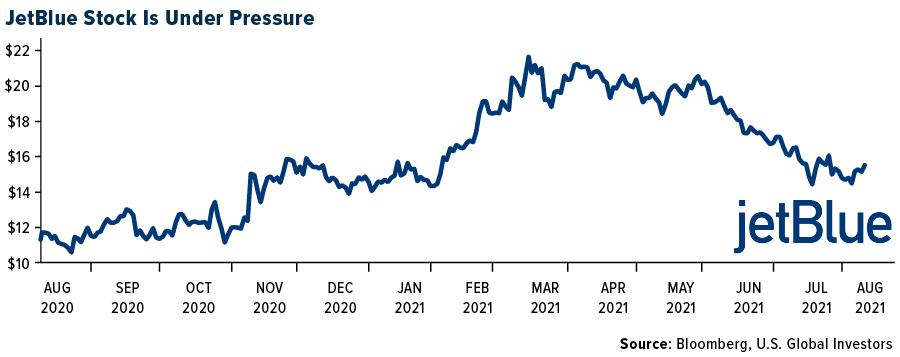

- JetBlue announced its first transatlantic service, by starting flights from New York to London in August for as low as $202 one way. The company secured coveted slots at Heathrow airport during the pandemic. This announcement comes just nine days after the U.K. announced it would allow fully vaccinated Americans to enter the country.

Threats

- Southwest Airlines published an Investor Update calling out a recent decline in close-in bookings and an increase in close-in cancellations due to the rise in the delta variant. This translated into a 3- to 4-point reduction in its third quarter revenue expectations to down 15% to 20% versus 2019

- Goldman says that JetBlue continues to expect third quarter revenue to be down 4% to 9% versus 2019 with the leisure strength observed over the last several months continuing into August. Management, however, is more cautious on the month of September. On the cost side of the ledger, the company continues to expect short-term inflationary pressures with low single-digit unit cost inflation until next year.

- While the Biden administration has been under pressure for months to rescind the travel ban, the White House recently stated there is no plan to ease restrictions anytime soon due to the rising COVID-19 case load and delta variant. The CDC recently lowered its travel advisory for Canada to Level 2, indicating “moderate level of COVID-19,” the same day Canada re-opened its borders to vaccinated Americans. The CDC also raised its travel advisory for both Israel and France to Level 4, the highest level, indicating “very high levels of COVID-19.”

Emerging Markets

Strengths

- The best performing country in emerging Europe for the week was Czech Republic, gaining 3%. The best performing country in Asia this week was India, gaining 2%.

- The Turkish lira was the best performing currency in emerging Europe this week, gaining 1%. The Vietnamese dong was the best performing currency in Asia this week, gaining 0.50%.

- Poland’s economy expanded at its fastest-ever annual pace, rebounding from last year’s coronavirus lockdown. The second quarter gross domestic product soared 10.9% shared with the same period of 2020, above the estimated economic growth increase of 10.7%.

Weaknesses

- The worst relative performing country in emerging Europe for the week was Hungary, gaining 0.40%. The worst performing country in Asia this week was South Korea, losing 4.4%.

- The Russian ruble was the worst performing currency in emerging Europe this week, losing 0.4%. The South Korean won was the worst performing currency in Asia, losing 1.6%.

- The economic data out of China was reported weaker this week. Chinese banks extended 1.08 trillion yuan ($166.5 billion U.S. dollars) in new yuan loans in July, down from June and below analysts’ expectations. Broad M2 money supply grew 8.3% from a year earlier, central bank data showed on Wednesday, below the estimates of 8.7% forecast in a recent Reuters poll.

Oppurtunities

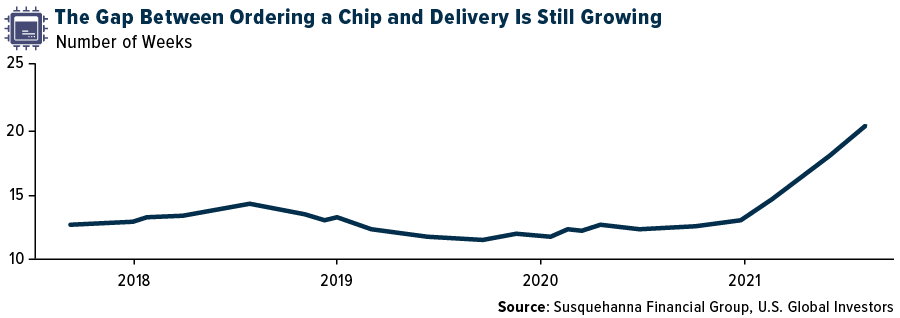

- The amount of time it is taking for chip-starved companies to get orders filled has stretched to more than 20 weeks, indicating the shortages that have held back automakers and computer manufacturers are getting worse. Semiconductor companies should continue to outperform on strong global demand. Taiwan is the current global leader in chip production.

- Ukrainian bonds are likely to outperform its peers thanks to a resilient economy and finances, as well as an increased likelihood of IMF funding in 2021, according to Goldman Sachs credit strategist Mikhail Galkin. His bullish view is not just based on the recent progress with anti-corruption reforms and, hence, IMF. More importantly, Ukrainian macro and credit metrics have been demonstrating impressive resilience to COVID. The hryvnia is one of the world’s best performing currencies this year.

- The central bank in Turkey left its rates on hold this week, defying President Erdogan’s calls for a cut. The decision pushed equities and the Turkish lira higher as the policy makers did not give in to the political pressure and lower borrowing costs despite the deteriorating outlook for inflation. Consumer-price gains accelerated to 18.95% in July. The one-week repo rate was left at 19%. Foreign investors were the net buyer of Turkish equites.

Threats

- Poland’s populist government on Wednesday advanced legislation that would restrict foreign ownership of local broadcasters — a move seen as targeting an independent TV channel controlled by a major U.S. media group. The bill has been widely criticized by foreign observers and is seen as the Polish government’s latest push to control the domestic media.

- Czech inflation exceeded the top of the central bank’s tolerance range in July. Annual consumer-price growth quickened to 3.4%, from 2.8% a month earlier, the Czech Statistics Office said on Tuesday. That is higher than the median analyst estimates for 2.9% and the central bank’s 3% projection. Spiking inflation in central emerging Europe is bolstering arguments for policy makers to continue their campaign of rapid interest-rate increases.

- Eurozone June industrial production fell 0.3% month-over-month versus consensus for 0.2% drop and prior 1.1% fall revised from 1.0% initially reported. It was as second consecutive decline mostly caused by supply chain disruptions. Input shortages and lengthening suppliers’ delivery times may further limit the recovery in manufacturing too.

Energy and Natural Resources Market

Strengths

- Sugar was the best performing commodity, up x.xx% as investors realized frost damaged crops in Brazil are likely to curtail production. Demand for copper remains strong in China. China’s imports of copper ore and concentrates from January to July grew by 6% to reach 13.4 million tons, according to the latest data from China’s General Administration of Customs. As for July, the import total amounted to 1.8 million tons, which was 12.9% higher from June.

- Tin’s scorching rally rolled on as a series of disruptions hindered supply just as demand for electronics surges. This year’s best-performing base metal notched a new high in Shanghai on Wednesday, while prices in London have been hitting record after record highs since mid-July. The market is in the grip of a historic squeeze as a global economic recovery boosts consumption, while logistical issues affect shipping and output curtails production at key Asian suppliers.

- Aluminum continues to do well. AUP Midwest aluminum premium futures curve continues to rally to record highs as imports continue to decline and logistics are still challenging. Aluminum is up about 31% year-to-date (YTD), with LME/SHFE prices holding close to a 10-year high, driven by resilient demand, supply disruption and tight metal availability.

Weaknesses

- Lumber was the worst performing commodity, dropping xx.x%. So far, lumber prices haven’t shown signs of rebounding yet. According to Random Lengths, the Framing Lumber Composite fell by $16 last week to $463, the 11th consecutive weekly drop. Buying demand has been slow to come back. In OSB markets, the Composite fell $137 last week to $586, with distributors holding back orders waiting for the first sign of a bottom to this drop.

- Oil plunged to an 11-week low, extending losses after the worst week since October, as new waves of COVID-19 cases threatened fuel demand. Futures fell below $66 a barrel in New York. China’s biggest oil refiner is scaling back operations as Beijing’s aggressive response to the Delta virus variant saps demand for road and aviation fuel, according to an analyst. Additional comments by the White House that OPEC’s July agreement to boost crude production by 400,000 barrels per day monthly into 2022 is “simply not enough,” citing rising gasoline prices.

- Iron ore prices are falling as China appears to be enforcing its target of steel production being flat in 2021. The 10-day data shows daily pig iron production is down 6% in July versus June, and key steel producers have announced plans to cut production in the second half. This has resulted in mills destocking and iron ore prices falling sharply in a thin spot market.

Opportunities

- Chesapeake Energy Corp., the natural gas producer that emerged from bankruptcy earlier this year, agreed to acquire a rival driller controlled by Blackstone Group Inc. for about $2.2 billion as consolidation accelerates in the U.S. shale patch.

- Daroga Power said its infrastructure fund raised $230 million to install Bloom Energy Corp. fuel cells, betting that demand for reliable clean power will grow as extreme weather strains electric grids. The fund, which is a partnership between Daroga and an unnamed affiliate of Related Cos., will deploy 32.85 megawatts of the fuel cells at sites in California, New York, New Jersey, Connecticut, Massachusetts, and Maryland by the end of 2022.

- By 2060 , China, the world’s second-largest economy, aims to transform its power generation mix from roughly 70% fossil fuels today to 90% renewable sources such as wind, solar, hydro, and nuclear power, according to Bloomberg NEF’s China Policy Bulletin in April 2021.

Threats

- Iron ore dropped for the third consecutive week, now at four-month lows as the spread of the Delta variant increased the risk of a demand slowdown. Additionally, there is lower expected second half steel output in China. China domestic weekly utilization declined for the 3rd consecutive week, down 1.1 points to 85.7%.

- For Rio Tinto, a cost overrun at a Mongolia copper mine was caused by mismanagement and not the unfavorable rock conditions, Dow Jones reports, citing a report commissioned by the owners of the Oyu Tolgoi mine.

- Copper fell to the lowest level in more than two weeks amid concerns that a resurgence in the fast-spreading Delta virus variant may derail demand in top consumer China. Data showed China’s appetite for a range of commodities softened in July even before a surge of the Delta variant, with copper and iron ore imports declining for a fourth straight month.

Domestic Economy and Equities

Strengths

- July inflation of 0.5% matched consensus estimates, down from June’s 0.9% print and currently the lowest growth since February. Annualized inflation was reported at 5.4% above consensus estimates of 5.3%, and unchanged from June’s 5.4% print. July core inflation, excluding food and energy, was reported at 0.3% below consensus of 0.4%, and the lowest growth since March. July annualized core inflation was released at 4.3%, slightly lower than June’s 4.5%.

- U.S. job openings in June surged to 10,073,000, but labor force participation remains below pre-COVID levels. And for the first time since COVID struck, job openings exceed the level of unemployment.

- NuCo Corporation, a steel producer, was the best performing S&P 500 stock for the week, increasing more than 20%. Shares declined after the company reported disappointing results.

Weaknesses

- August preliminary Michigan Consumer Sentiment fell 11 points month-over-month to 70.2, the lowest print since December 2011, and missing estimates for 81.0. The index measuring current economic conditions fell 6.6 points to 77.9. The index measuring consumer expectations fell 13.8 points to 65.2. According to the report, current downside is driven by the spread of the delta variant.

- Prices paid to U.S. producers rose in July by more than expected, suggesting that higher commodity costs are still adding to inflationary pressures for companies. The producer price index (PPI) increased 1% from the prior month and 7.8% from a year earlier, Labor Department data showed on Thursday.

- Perrigo, a pharmaceutical company, was the worst performing S&P 500 stock for the week, losing more than 10%. Shares sold off after the company reported weaker second quarter results. Adjusted earnings per share (EPS) fell from $0.59 to $0.50, below expected $0.62.

Opportunities

- Companies across America are taking advantage of a dip in benchmark Treasury yields last week to tap the debt markets, as borrowing costs are near historic lows. Thirty investment-grade rated borrowers’ priced new deals on Monday and Tuesday, the most for any two-day period since last September, according to Bloomberg data.

- U.S. stocks set another record high. The S&P 500 Index gained in the past five days. An improving job market and good company earnings will likely continue to push equites higher.

- Industrial production will come out next week. Most Bloomberg economists see industrial production increasing by 0.5% in July.

Threats

- The Senate passed a trillion-dollar infrastructure package on Tuesday and the bill now will go to the House for approval. However, the leaders of the Congressional Progressive Caucus, nearly 100 members strong and backed by Ms. Pelosi, say they will not pass any stand-alone infrastructure bill unless and until the Senate approves the left’s priority, all $3.5 trillion of the social policy bill. This would be the largest expansion of the social safety net since the Great Society of the 1960s, the New York Times reported.

- Most Republican senators have signed on to a pledge not to help Democrats raise the debt ceiling. Republicans have tried to tie the debt ceiling to Democrats’ human infrastructure spending plans, though raising the debt limit does not authorize new spending but instead allows the Treasury to issue new debt to cover spending Congress has already authorized.

- The spread of the delta variant is dominating headlines this week and there have now been concerns of the vaccine’s efficiency. The vaccines have been highly effective in protecting against hospitalizations, severe illness, and death amid the spread of the delta variant. A recent study, however, found a big drop in efficacy against infections on the part of the Pfizer vaccine.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performer for the week was Bitrise Token, gaining over 6,000%.

- The cryptocurrency market has continued a solid bullish trend in early August, writes CoinTelegraph, with the total market capitalization nearing $2 trillion. Over the past 21 days, crypto markets have surged $700 billion, or 58%.

- According to a new report from accounting firm KPMG, titled “Pulse of Fintech H1 2021,” crypto and blockchain investments continue to grow thanks to ever-rising investor interest. The first six months of 2021 saw 548 investment activities, including venture capitals, private equities and mergers and acquisitions in the blockchain and cryptocurrency sectors, CoinTelegraph recaps. The total value of investments during the first half of the year is $8.7 billion.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week was Crypto Village Accelerator, falling 88.48%.

- Institutional crypto products have seen their fifth consecutive week of outflows, writes CoinTelegraph, despite the bullish momentum in the markets. CoinShares estimates that outflows totaled $26 million for the week. Other negative news in the sector comes from Coinbase dropping its promise that its stablecoin was backed dollar-for-dollar, upon recent disclosure. It turns out that holdings included commercial paper and corporate bonds; securities that might not retain their value should there be a large withdrawal of assets.

- Ethereum network congestion is forcing some companies to look for new solutions. As reported by CoinTelegraph, one example is Funfair Technologies-owned KingTiger Casino. The casino’s official website announced the following: “We have had to temporarily close our casinos due to the Ethereum network congestion, making it impossible to run our games in their current format.” The gambling site was powered by FUN token, an in-house initiative by FunFair Technologies running on smart contract technology.

Opportunities

- Tron Foundation has partnered with APENFT and WINKLinkto launch the $300 million Tron Arcade fund, writes CoinDesk, which will invest in so-called GameFi projects over the next three years. The fund’s goal is to support developers and create GameFi projects by building DeFi content, according to the foundation.

- Cryptocurrencies were in the crosshairs this week as the Senate negotiated tax rules for cryptocurrencies. On Friday, an official at the U.S. Treasury Department spoke on condition of anonymity, that the department is seeking to clarify that it only wants tax data from brokers. Other firms key to the nearly $2 trillion crypto market, such as developers and miners, to hardware and software, won’t have new requirements.

- With Bitcoin up 50% form recent lows, predictions of the popular digital asset surging to $100,000 are back in vogue. Revived animal spirits and “FOMO” from the near breach of $20,000 has speculators hungry for further gains.

Threats

- On Tuesday, cross-chain decentralized finance (DeFi) platform Poly Network was hacked, reports CoinDesk, with the alleged hacker draining roughly $600 million in crypto. Poly Network operates on the Binance Smart Chain, Ethereum and Polygon blockchains and the attack struck each chain consecutively. The Poly team identified three addresses where stolen assets were transferred, the article continues. According to a tweet by Poly Network on Thursday, $342 million had been returned.

- Even though the cryptocurrency sector is back in sight of a $2 trillion market value, Bloomberg reports that further gains face an obstacle from potential new U.S. tax reporting requirements. The crypto industry failed to adjust the tax reporting rules (projected to raise $28 billion in revenue), the article explains, despite a big push by lobbyists. Procedural issues could imperil efforts to change the provision when the House of Representatives takes up the bill.

- Sam Benstead of the Telegraph recently penned a note on why the “Bitcoin revolution” could cost you your privacy. Sam sees the greatest threat when governments launch digital versions of legal tender. If cash is pushed further to the fringes for your transactions, then every spending record would be online and traceable by the government, he explains. Governments may even set the terms on how, when or where your digital currency is spent.

Gold Market

This week spot gold closed the week at $1,779.74, up $16.71 per ounce, or 0.95%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 1.75%. The S&P/TSX Venture Index came in off just 0.28%. The U.S. Trade-Weighted Dollar fell 0.30%.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Aug-10 | Germany ZEW Survey Expectations | 55.0 | 40.4 | 63.3 |

| Aug-10 | Germany ZEW Survey Current Situation | 30.0 | 29.3 | 21.9 |

| Aug-11 | Germany CPI YoY | 3.8% | 3.8% | 3.8% |

| Aug-11 | CPI YoY | 5.3% | 5.4% | 5.4% |

| Aug-12 | Initial Jobless Claims | 375k | 375k | 387k |

| Aug-12 | PPI Final Demand YoY | 7.2% | 7.8% | 7.2% |

| Aug-15 | China Retail Sales YoY | 10.9% | — | 12.1% |

| Aug-18 | Eurozone CPI Core YoY | 0.7% | — | 0.7% |

| Aug-18 | Housing Starts | 1605k | — | 1643k |

| Aug-19 | Initial Jobless Claims | 360k | — | 385k |

Strengths

-

- The best performing precious metal for the week was platinum, up 4.93%. Barrick Gold’s earnings exceeded estimates as higher metal prices blunted the impact of rising costs and lower output for the world’s second-largest bullion producer. The company reported adjusted profit of 29 cents a share for the second quarter, compared with the 26-cent average estimate among Bloomberg analysts. It was Barrick’s eighth straight earnings beat. During the quarter, the company produced 1.04 million ounces of gold at a cash cost of $729 per ounce.

- Karora Resources reported earnings per share (EPS) of $0.10 per share, ahead of consensus of $0.08 per share. EPS was helped by the strong sales and production numbers during the quarter of 29,800 ounces and 30,400 ounces, respectively. Cash costs of $874 per ounce were marginally better than consensus of $887 per ounce.

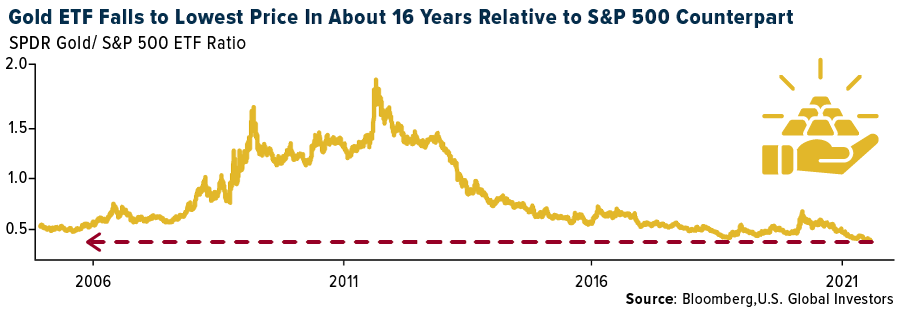

- Gold’s status as a precious metal is belied by its performance relative to U.S. stocks. Comparing the SPDR Gold Shares and SPDR S&P 500 exchange-traded funds shows as much. Monday’s ratio between the gold and stock ETFs was the lowest since September 2005, according to data compiled by Bloomberg. The ratio was down 44% from a March 2020 peak and off 78% from a record set 10 years ago this month.

Weaknesses

- The worst performing precious metal for the week was silver, down 2.93% on little specific news largely following gold’s drop on Monday. Pan American Silver reported EPS of 22 cents versus a 34-cent consensus, primarily due to lower-than-expected production and inventory build-up of $38 million. Silver production of 4.5 million ounces. was down 2% quarter to quarter and 8% lower than consensus. Gold production of 142,000 ounces. was up 3% but 4% lower than consensus.

- U.S. gold futures traded modestly lower last week, however a sudden burst of selling on Sunday of gold futures contracts sent gold prices plunging to as low as $1,677 an ounce. The plunge was obvious manipulation of the price by the bullion banks, creating 20,000 contracts out of thin air and then forcing the sale when markets are largely closed; you expect to get the worst price. Together with Friday’s post-payroll plunge, this has been the biggest two-day drop in gold (in dollar terms) since the March 2020 crash.

- Gold headed for a second straight weekly loss amid concerns that the Federal Reserve may soon curb its massive monetary stimulus. The durability of the global economic recovery has dimmed the appeal of the haven asset in recent weeks as some Fed officials signaled they’re ready to discuss softening ultra-loose monetary policy. U.S. data on Thursday added to signs of rising inflation pressures and a strengthening labor market. Ten-year benchmark Treasury yields have climbed this week, curbing the appeal of non-interest paying bullion, but eased slightly on Friday. The dollar inched lower. Gold has slid this month — despite the spread of the delta variant of COVID-19 clouding the global economic outlook — and has now given up most of its gains from a rally in April and May.

Opportunities

- Jerry Braakam, CIO of First American Trust, is concerned that stagflation – rising prices and falling incomes – may be in the cards. Such an environment should benefit sectors with the highest degree of pricing power — “energy, materials, even some consumer durables, if they can pass on higher costs to consumers, which they’re trying to do,” he said. “P/E multiples would likely compress if this becomes sustainable and thus highly valued stocks would be most vulnerable and cheaper ones less so.” With the rising inflation of the1970s, gold shot up and gold stocks significantly outperformed the broader markets.

- Metal and mining equities could have a 40% upside from current levels over the next 6-9 months, Citi says, assuming the duration and magnitude of the current rally is like past cycles. The history of mining cycles shows that pullbacks in commodities and equities in the 12–18-month period from trough are followed by price acceleration.

- SilverCrest Metals provided a construction update for the Las Chispas property. Overall construction is 33% complete, ahead of the scheduled 28%. Management remains comfortable with the $138 million initial capex estimate with the fixed price plant construction contract and efficiencies limiting the impact of inflation. Detailed engineering is 90% complete.

Threats

- Jackson Hole is gold’s biggest risk factor, with gold already dropping below $1,700 after Friday’s payrolls beat highlighted the potential that policy makers will shift from spurring growth toward curbing inflation.

- The world’s second-largest bullion producer, Barrick Gold, sees the U.S. as its “big challenge” with regards to COVID-19 vaccinations for its workers, CEO Mark Bristow said in an interview with Bloomberg TV. Vaccination rates among Barrick employees in Nevada are about 25%.

- Demand for platinum group metals (PGMs) is facing decline due to the growth of battery electric vehicles. Conventional cars with internal combustion engines use three PGMs – platinum, palladium, and rhodium – in their catalysts to limit emissions. Electric vehicles do not use catalysts. Bloomberg NEF estimates that demand for PGMs from autos will peak around 2024 and fall 59% by 2040. Platinum may not be down and out though as fuel cell-powered vehicles do use platinum as a catalyst to convert hydrogen to energy.

Leaders and Laggards

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission (“SEC”). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product. Certain materials in this commentary may contain dated information. The information provided was current at the time of publication. Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content. All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (06/30/2021):

Blackstone Group Inc.

Delta Air Lines

Goldman Sachs Group Inc.

JetBlue Airways Corp.

Ryanair Holdings PLC

SkyWest Inc.

Southwest Airlines

Wizz Air Holdings

Barrick Gold Corp.

Karora Resources

Pan American Silver

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

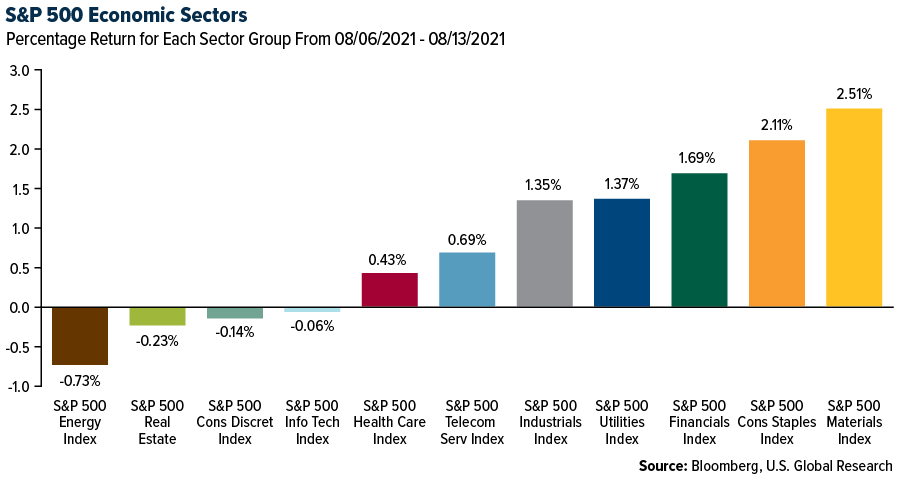

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The Producer Price Index (PPI) program measures the average change over time in the selling prices received by domestic producers for their output.

The University of Michigan Consumer Sentiment Index is a consumer confidence index published monthly by the University of Michigan.

M2 Money Supply is a broad measure of money supply that includes M1 in addition to all time-related deposits, savings deposits, and non-institutional money-market funds.