Here’s What the Market Did EVERY TIME the Fed Cut Rates During an Economic Expansion

Date Posted: July 12, 2019

Read time: 50 min

NULL

By Frank Holmes

CEO and Chief Investment Officer

U.S. Global Investors

We’re just past the midpoint of 2019, and ordinarily that would mean it’s time for the Commodities Halftime Report. That will need to wait until next week, though, as there are more urgent things for me to share with you, starting with a mea culpa.

As you know, the market collapsed in the fourth quarter of 2018, sinking some 20 percent between the end of September and December. Expressed another way, it fell four standard deviations below the mean over 60 trading days—a huge move.

When the market has fallen by that much, it’s historically been a good time to get contrarian because a reversion to the mean hasn’t been too far behind. Mean reversion, as I explain in “Managing Expectations,” is the idea that prices tend to move back to their historic averages eventually.

The reason I’m telling you this now is that I didn’t take my own advice. I believed, as others did, that more pain was ahead. Prices bottomed, but instead of buying, I took money off the table. And watched the market bounce strongly. By the time it became clear that this aging bull market wasn’t slowing down, it was too late. The opportunity had come and gone.

We all have a choice on how we deal with setbacks. When asked once about the single most important lesson he’s learned over the course of his long career, the billionaire hedge fund manager Ray Dalio pointed to his bad bet in the 1980s. He believed the U.S. was headed for a depression, and when one never came, he fell so deeply into debt that he had to borrow $4,000 from his father to make ends meet. The experience “was one of the best things that ever happened to me because it gave me the humility I needed,” he wrote in his bestseller Principles: Life and Work.

I never stop learning, even after four decades spent in global markets. That’s as true now as it was when I first started as a young analyst in Toronto. And I’m pleased to say that, after thoroughly reviewing our models, our investment team and I have great confidence going forward.

Cutting Rates in an Expansionary Environment

The market is now at record highs, and unemployment is way down. Even so, a U.S. rate cut is expected as early as this month. During his congressional testimony this week, Federal Reserve Chairman Jerome Powell raised concerns over slower global growth and trade tensions, which in turn have contributed to weaker demand and manufacturing activity. The most recent Global Manufacturing Purchasing Manager’s Index (PMI) showed that, at 49.4, factories contracted for the second straight month in June. We haven’t seen back-to-back sub-50.0 PMI readings since the second half of 2012.

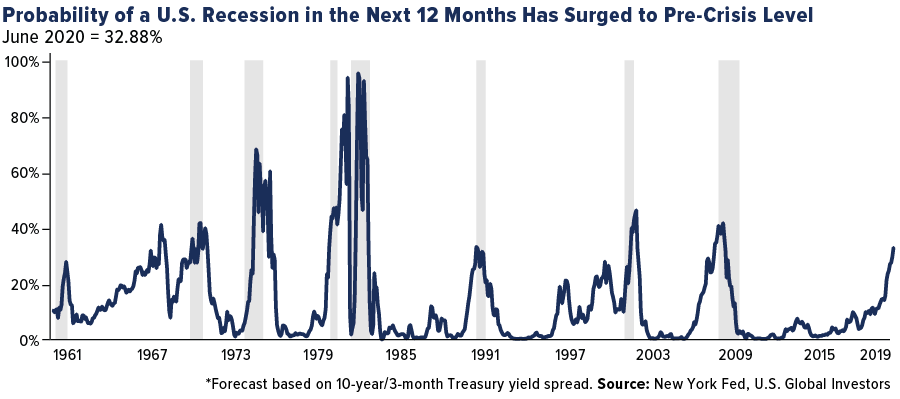

There’s also a one-in-three chance we could see a full-blown recession sometime next year. That’s according to the New York Fed’s recession probability index, which flashed a 12-year high of 32.9 percent last month. Since 1960, every time the index has surpassed 30 percent, the economy has tanked within the next 12 months.

Despite the risks, the U.S. economy is still expanding—an unusual, though not unheard-of, time for the Fed to consider cutting rates.

So let’s assume for a moment that the Fed does take action next week. What effect would that have on the stock market as well as manufacturing activity?

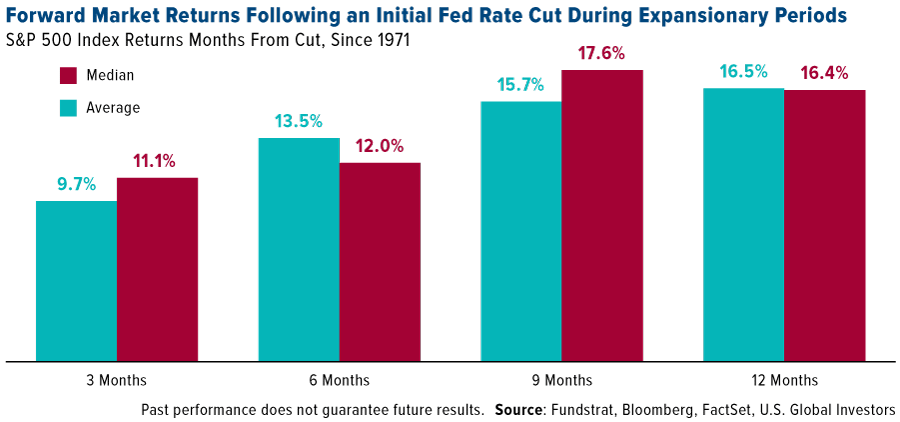

That’s precisely what analysts at market research firm Fundstrat looked into recently, and what they found is that 100 percent of the time, the market increased in the next three, six, nine and 12 months. The median gain over nine months, in fact, was nearly 18 percent.

Hypothetically, if the same thing were to happen today, that would put the S&P 500 Index at around 3,500 by next April.

Once again, for those in the back: In every case going back to 1971, when the Fed began a new easing cycle while the economy was expanding, stocks went up three months, six months, nine months and 12 months later. No exceptions.

Manufacturers Looking for Tariff Relief

That wasn’t the case with manufacturing activity. According to our own research, the ISM Manufacturing Index, which measures the U.S. sector, rose only a third of the time three months following a rate cut in good times. Six and nine months out, the index was up half the time. Twelve months out, it was higher about 66 percent of the time.

Those are decent odds, but a rate cut now would be much more favorable for stocks, statistically speaking.

To get manufacturing up to full capacity, I think there needs to be a resolution to the U.S.-China trade war. That was also the assessment of Renaissance Marco. In a note dated July 2, Neil Dutta, head of economics, observed that the word “tariff” featured prominently in purchasing managers’ June commentaries, suggesting trade issues were partly to blame for ISM weakness. If tariffs are indeed a driver of slower manufacturing growth, “it would imply the ISM has room to pick up from here. After all, we’ve seen some relief over the weekend (China) and earlier in June (Mexico),” Dutta wrote.

Bullish on Gold

If rate cuts are favorable for stocks, they can act as rocket fuel for the price of gold. As I’ve explained many times before, the yellow metal has thrived in low-rate, weak-U.S. dollar environments.

This week UBS reiterated the relationship between gold and interest rates, writing: “Low to negative rates suggest falling cost of holding gold at a time when elevated trade and geopolitical uncertainty strengthen the case for diversification.” Strategists Joni Teves, Roque Montero and Bhanu Baweja see gold hitting $1,450 an ounce by the end of this year and rising “modestly” to $1,500 in 2020.

TD Securities expects gold to average $1,400 for the rest of the year, followed by a lift toward $1,500 “in the final months of 2020,” driven by low to negative rates. One of President Donald Trump’s picks for the Federal Reserve Board of Governors, Judy Shelton, is also constructive for gold, as she is in favor of lowering rates and supports a return to the gold standard.

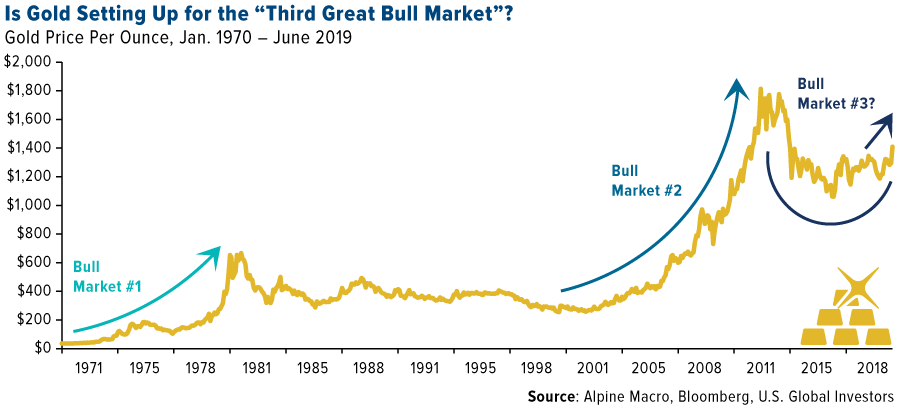

Finally, analysts at Alpine Macro see the beginnings of gold’s “third great bull market of the post-war period.” A rate cut by the Fed could set in motion a multi-year bear market in the dollar, analysts write, which is very supportive of gold. With the recent technical break above $1,400, “new all-time highs for gold should be seen in the coming years,” the research firm writes.

Curious to know which countries produce the most gold? Our ever-popular post has been updated with the latest data! Click below to see which country tops the list!

Gold Market

This week spot gold closed at $1,414.31, up $15.06 per ounce, or 1.08 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 2.67 percent. The S&P/TSX Venture Index came in off 1.83 percent. The U.S. Trade-Weighted Dollar fell 0.48 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Jul-11 | Germany CPI YoY | 1.6% | 1.6% | 1.6% |

| Jul-11 | CPI YoY | 1.6% | 1.6% | 1.8% |

| Jul-11 | Initial Jobless Claims | 221k | 209k | 221k |

| Jul-12 | PPI Final Demand YoY | 1.6% | 1.7% | 1.8% |

| Jul-14 | China Retail Sales YoY | 8.5% | — | 8.6% |

| Jul-16 | Germany ZEW Survey Current Situation | 5 | — | 7.8 |

| Jul-16 | Germany ZEW Survey Expectations | -25.0 | — | -21.1 |

| Jul-17 | Eurozone CPI Core YoY | 1.1% | — | 1.1% |

| Jul-17 | Housing Starts | 1260k | — | 1269k |

| Jul-18 | Initial Jobless Claims | 216k | — | 209k |

Strengths

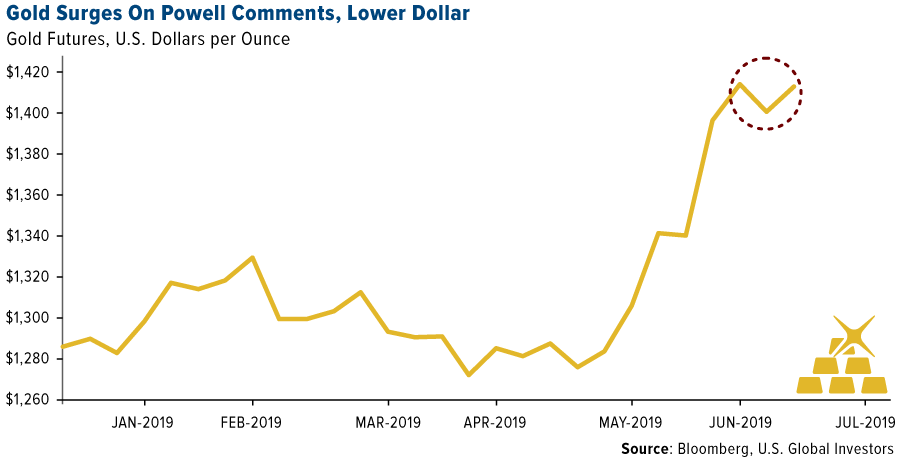

- The best performing metal this week was platinum, up 2.46 percent. The yellow metal jumped on Wednesday after Federal Reserve Chairman Jerome Powell’s comments spurred bets on a cut in interest rates later this month. Powell said concerns over trade and global growth continue to weigh on the domestic economic outlook. “Low rates help make gold and other commodities more competitive against assets that offer interest,” writes Bloomberg’s Justina Vasquez.

- China’s central bank raised its gold reserves for a seventh straight month in June, buying 10.3 tons on top of the nearly 74 tons bought since December, reports Bloomberg News. “Aside from its attempt to diversify holdings of dollars, owning more gold reserves is also an important strategy in China’s rise as a superpower,” says Howie Lee, economist at Oversea-Chinese Banking Corp.

- Several gold miners reported positive second quarter results this week, reports Kitco News. Gran Colombia Gold hiked its 2019 production guidance from 225,000 to 240,000 ounces of gold. SSR Mining produced over 98,000 gold-equivalent ounces from its three operations, which keeps it on pace to meet or beat annual guidance, says the company’s CEO. Wesdome Gold Mines mined 22,437 ounces in the second quarter, up from 16,628 ounces the same time a year ago. Lastly, Eldorado Gold is on track to meet its 2019 guidance after producing 91,803 ounces of gold this past quarter.

Weaknesses

- The worst performing metal this week was palladium, down 1.58 percent. Gold slipped on Wednesday as the U.S. dollar pared earlier losses and the yield on U.S. Treasuries hit a one-month high. Ed Meir, an analyst at INTL FCStone, told Bloomberg that gold “is sort of caught between cross-currents.” The yellow metal fell slightly on Friday morning following stronger than expected producer price index (PPI) data.

- Titan had the biggest single-day decline in almost six years on Monday, falling as much as 10.9 percent, after the Indian jewelry maker said high gold prices have dented jewelry demand. The company said that the second quarter was a tough macro-economic environment and that growth was lower than planned, reports Blomberg.

- Physical gold demand in Asia slowed this week as consumers sold back bullion to cash in on the price rally, reports Reuters. India, the world’s second largest consumer, saw weaker demand due to a surprise rise in import duties from 10 percent to 12.5 percent last week and as prices hit a record of 35,145 rupees per 10 grams on Thursday.

Opportunities

- The World Gold Council (WGC) released its mid-year outlook and cited financial market uncertainty and accommodative monetary policy as likely to support gold investment demand in the second half of 2019. HSBC raised its gold price forecast to $1,362 an ounce in 2019, up from $1,314. The National Australia Bank also raised its forecast for the yellow metal for the remainder of the year to $1,400 per ounce, up from $1,380 previously.

- According to data compiled by Bloomberg, the iShares Silver Trust had its best week in a year and hasn’t seen any outflows so far in July. Plus, the fund had its biggest monthly inflow since 2017 in June. Bloomberg’s Colin Beresford writes that silver has benefitted from haven demand as major central banks respond to weakening economic growth with a more dovish stance. The gold-to-silver ratio was at 93 this week, just shy of the high of 100 reached in February 1991.

- The U.S. dollar fell for the third consecutive day on Friday morning even after inflation data came in stronger than expected, reports Kitco News. Core U.S. consumer price index (CPI), excluding food and energy, rose 0.3 percent in June—the largest increase since January 2018. A weaker dollar has historically been constructive for the price of gold.

Threats

- South African platinum miners, including Anglo American Platinum, Impala Platinum Holdings and Sibanye Gold, are conducting pay talks this week with a major labor union. Ahead of the talks the miners have set aside cash and metal stockpiles to endure a labor strike. However, the union is asking for a pay raise of as much as 48 percent.

- KC Chang, precious metals analyst at IHS Markits, said in an interview with Kitco News that he expects gold prices to fall back to $1,300 an ounce by the end of the year. Chang says that the gold price rally in the last three weeks has run too far ahead of what economic fundamentals suggest and that there could be only one rate cut this year.

- The Chinese economy continues to lose stream. China’s exports fell in June by 1.3 percent from a year earlier as the trade war with the U.S. rages on. Reuters reports that China is expected to release data showing that its growth in the second quarter was the weakest in at least 27 years. This could contribute negatively to the overall slowdown in global growth.

Index Summary

- The major market indices finished mostly up this week. The Dow Jones Industrial Average gained 1.52 percent. The S&P 500 Stock Index rose 0.78, while the Nasdaq Composite climbed 1.01 percent. The Russell 2000 small capitalization index lost 0.36 percent this week.

- The Hang Seng Composite lost 1.26 percent this week; while Taiwan was up 0.36 percent and the KOSPI fell 1.13 percent.

- The 10-year Treasury bond yield rose 8 basis points to 2.123 percent.

Domestic Equity Market

Strengths

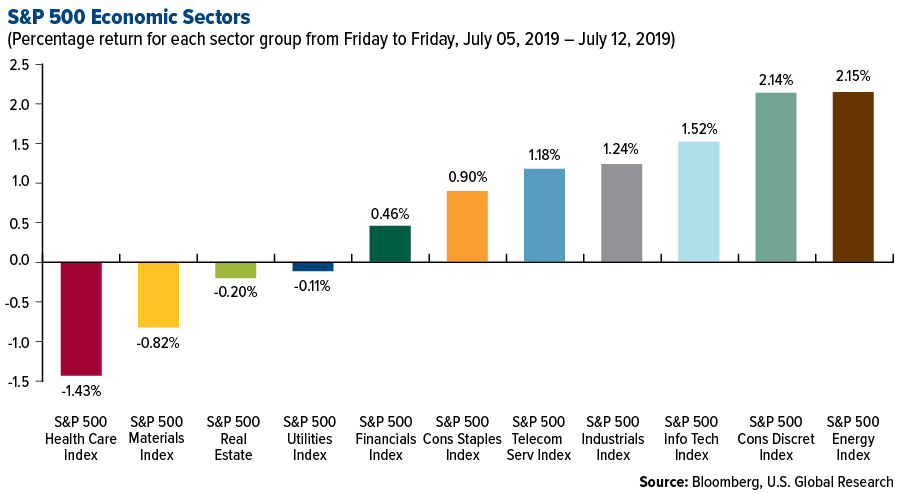

- Energy was the best performing sector of the week, increasing by 2.15 percent versus an overall increase of 0.78 percent for the S&P 500.

- Western Digital was the best performing stock for the week, increasing 13.97 percent.

- Shares of Cigna jumped more than 10 percent on Thursday after the Trump administration announced its plan to eliminate drug rebates from government prescription drug plans. The administration had attacked drug rebates in the past, stating that rebates provided financial incentives for pharmaceutical companies to set list prices for drugs artificially high.

Weaknesses

- Health care was the worst performing sector for the week, decreasing by 1.43 percent versus an overall increase of 0.78 percent for the S&P 500.

- Illumina was the worst performing stock for the week, falling 19.35 percent.

- Marriott got slammed with a $123 million fine after a major data breach exposed the personal data of 339 million hotel guests. The breach occurred in 2014 in the hotel company’s Starwood database, and Marriott inherited the undetected breach when it bought Starwood in 2016.

Opportunities

- Facebook is looking around for game studios to buy, The Information reports. The company is also signing exclusive deals to bring big blockbuster games like Assassin’s Creed on its Oculus VR headset.

- Volkswagen announced they will inject $2.6 billion into Ford unit Argo AI taking the overall deal to $7 billion. Volkswagen will reportedly contribute $1 billion in capital and $1.6 in business activities, and VW and Ford will be equal stakeholders of the venture.

- Nintendo revealed a new console – a smaller version of the Nintendo Switch called the Switch Lite. The Switch Lite costs $100 less than the Switch because it’s a portable-only console.

Threats

- Illumina stock fell nearly 20 percent on Friday after the genomic sequencing leader announced preliminary results for its second quarter on Thursday evening. Illumina said that it expects to report second quarter revenue of $835 million, $50 million lower than what Wall Street analysts anticipated. The company also updated its full-year 2019 guidance and now projects revenue growth of around 6 percent, less than half its previous forecast of full-year revenue growth between 13 and 14 percent.

- A U.S. court has ruled that Amazon can be held liable for defective products sold on its platform. The ruling comes after a woman sued Amazon in 2016 after she was blinded by a retractable dog leash that snapped and hit her in the face. Further, Amazon is coming under fire for "deceptive" ratings and reviews on its website, and lawmakers are now demanding answers.

- Deutsche Bank’s week from hell just got worse after reported links with Jeffrey Epstein and a U.S. probe into its role in the 1MDB scandal. The U.S. government is reportedly probing whether the German bank’s work with the Malaysia 1MDB fund violated foreign corruption or anti-money laundering laws. Further, the bank is being slammed for paying $52 million ‘golden parachutes’ to fired execs. This came after news emerged that execs were being fitted for lavish suits while the firings were going on.

The Economy and Bond Market

Strengths

- The number of Americans filing applications for unemployment benefits dropped to a three-month low last week, suggesting sustained labor market strength that could help support a slowing economy. Initial claims for state unemployment benefits declined 13,000 to a seasonally adjusted 209,000 for the week ended July 6, the lowest level since April, the Labor Department said on Thursday. Economists polled by Reuters had forecast claims rising to 223,000 in the latest week.

- U.S. underlying consumer prices increased by the most in nearly one and a half years in June amid solid gains in the costs of a range of goods and services. The Labor Department said on Thursday its consumer price index, excluding the volatile food and energy components, rose 0.3 percent last month. That is the largest increase since January 2018 and follows four straight monthly gains of 0.1 percent. In the 12 months through June, the core CPI climbed 2.1 percent after advancing 2.0 percent in May. The Fed, which has a 2 percent inflation target, tracks the core personal consumption expenditures (PCE) price index for monetary policy. The core PCE price index increased 1.5 percent year-on-year in May and has undershot its target this year.

- Economists expect U.S. consumer spending, the biggest part of the economy, to pick up in the second quarter by more than previously estimated. Consumer spending will climb at a 3.4 percent annualized pace in the April through June period, according to a July 5-11 survey of 53 economists by Bloomberg News. That compares with a 2.7 percent rate seen in last month’s survey and a 0.9 percent reading in first-quarter data.

Weaknesses

- U.S. mortgage applications decreased last week, the Mortgage Bankers Association said on Wednesday. The seasonally adjusted index on loan requests, both to buy a home and refinance one, fell 2.4 percent to 505.8 in the week ended July 5. The week’s results include an adjustment for the Fourth of July holiday. “Borrowers have been less sensitive to low rates as many borrowers have either recently refinanced or are likely waiting for rates to fall even further,” Joel Kan, MBA’s associate vice president of economic and industry forecasting, said in a statement.

- American small business owners weren’t as optimistic in June as they were in May. Optimism slipped 1.7 points to 103.3, according to the NFIB Small Business Optimism Index. “Last month, small business owners curbed spending, sales expectations and profits both fell, and the outlook for expansion dampened. When you add difficulty finding qualified workers and harmful state-level laws and regulations, you’re left with a volatile mix where uncertainty has increased to levels not seen in more than two years,” said NFIB president and CEO Juanita Duggan.

- Americans’ financial anxiety remains high despite a strong economy. Gallup’s annual survey on personal finances, conducted each April, found that 40 percent of Americans say they are either running into debt or barely making ends meet. And, about one-in-five say they have saved nothing at all for retirement.

Opportunities

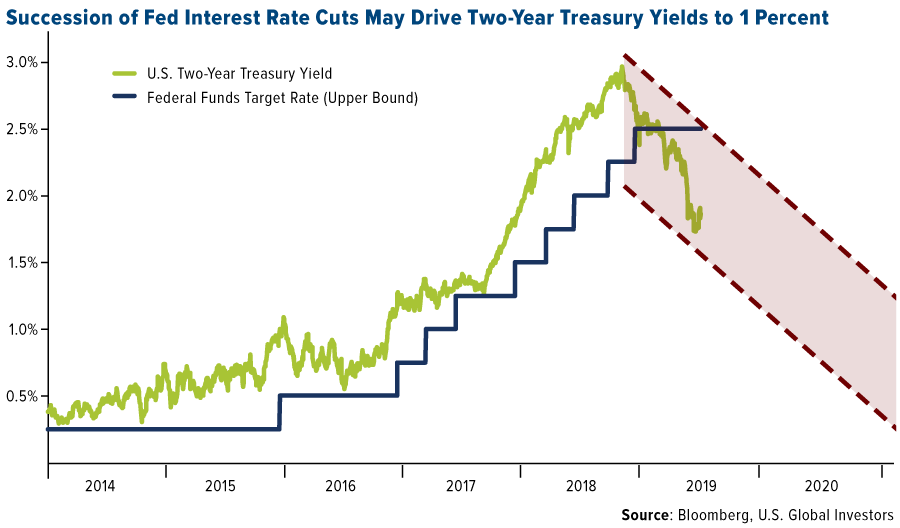

- Treasury two-year yields may slide to 1 percent by the end of 2020 as the Federal Reserve makes a series of interest rate cuts to counter slowing growth, according to Citigroup Inc. The firm forecasts the Fed will lower its benchmark rate by 25 basis points in July and potentially cut another two times by year-end. “I wouldn’t be surprised if we see two-year yields dropping to 1 percent by the end of next year,” said Shyam Devani, senior technical strategist in Singapore.” Such a move would be beneficial for short-term bonds.

- Regional production surveys next week out of New York (Monday) and Philadelphia (Thursday), as well as the Beige Book (Wednesday), will signal the degree to which the factory sector is rebounding from heightened trade anxieties in the second quarter, in addition to setting the tone for the pace of factory activity in the second half of this year.

- While calling the slowdown in global economic growth “largely a cyclical development,” the 36-member Organization for Economic Cooperation and Development (OECD) identified five “structural reform priorities” to give economic growth the shot in the arm it needs in each OECD member nation. The annual report, titled “Going for Growth 2019,” has identified the top five national reform priorities to “achieve strong, inclusive and sustainable growth.” These are: 1) Higher productivity growth; 2) Faster pace of reform; 3) Growth policies should ensure equality of opportunity; 4) Open markets that foster competition, innovation and productivity; 5) Environmental sustainability.

Threats

- U.S. Federal Reserve Chairman Jerome Powell said Wednesday that uncertainties hanging over global growth and trade tensions show little sign of abating recently. Powell said crosscurrents such as trade tensions and concerns about global growth have been weighing on the U.S. economic activity and outlook.

- Bank of America Corp. cut forecasts for global economic growth this year and next, blaming the uncertainty wrought by the trade war between the U.S. and China. Economists at the bank now expect the world economy to grow 3.3 percent both this year and next, down from previous estimates of 3.6 percent and 3.7 percent respectively.

- The European Commission lowered its forecast on Wednesday for the eurozone economy next year, saying that uncertainty over U.S. trade policy posed a major risk to the bloc. The European Union’s executive arm also lowered its estimate for inflation in the bloc.

Energy and Natural Resources Market

Strengths

- The best performing major commodity for the week was lead, which gained 6.06 percent. Crude oil soared to a seven-week high as a potential hurricane has forced offshore producers to evacuate. Flooding around the Gulf of Mexico could disrupt refiners. WTI topped $60 per barrel on a report that stockpiles are at their lowest since April, reports Bloomberg.

- Iron ore rose for a second day on Tuesday as supply disruptions and strong demand from China spur a global deficit, writes Bloomberg’s Krystal Chia. “There has been no change in the fundamentals—this year’s global deficit is hard to fill,” says Huatau Futures analysts Sarah Zhao. Futures in China rose as much as 4.5 percent after just last week seeing the biggest two-day fall since 2017.

- Nickel hit the highest price in three months on Friday morning on fears that major producer Indonesia will resume an export ban on ore in 2022, reports Reuters. In 2017, the nation relaxed the ban, but said that it would only last for five years and that nickel exports would be restricted again in 2022. Tighter supply with continued demand growth is constructive for higher prices.

Weaknesses

- The worst performing major commodity for the week was lumber, which fell 6.78 percent. While miners such as Rio Tinto, BHP Group and Anglo American are doing well with the rally in iron ore, Glencore is missing out. This is largely due to the miner relying on coal and not producing any iron. Bloomberg writes that Societe Generale and Macquarie Group cut their recommendations on the stock on Tuesday.

- BloombergNEF shows that worldwide investments in clean energy projects have hit a six-year low, with project financing slowing in all three major markets of the U.S., Europe and China. Global spending totaled $117.6 billion in the first six months of 2019, which is down 14 percent from a year earlier.

- Zinc fell close to its lowest level this year on Monday as Chinese output of refined zinc rose to 501,300 tons in June, the highest level since November 2017, according to data from SMM Information and Technology. Teck Resources said this week that the global zinc concentrate market is in surplus and that trade tensions are hurting the metal’s price.

Opportunities

- As Germany is moving away from coal use, German lignite miner and power plant operator Lausitz Energie Kraftwerke is moving into large-scale electricity storage, reports Bloomberg. Capital Dynamics, an asset manager handling more than $16 billion and buyer of clean power plants, is betting on smaller solar projects and installations. An announcement this week said the company is investing in Sol Systems to develop 100 megawatts annually of solar energy.

- Since the U.S.-China trade war began, China has been focusing on replacing foreign imports with domestic technology, such as carbon fiber. Current capacity is around 25,000 metric tons and four carbon fiber companies announced this week a plan to ramp up capacity to 111,800 metric tons by 2025, reports BloombergNEF.

- Copper fell then rose back up this week after speculation that President Donald Trump is seeking to weaken the dollar. Deutsche Bank analysts wrote in a note this week that copper is its preferred metal play for the second half of the year due to rising demand and mining disruptions.

Threats

- Tensions continue to grow in the Middle East. Iran’s military has vowed to retaliate against the seizure by British Royal Marines of an oil tanker filled with Iranian crude oil off the coast of Gibraltar last week, reports Bloomberg.

- Artisanal output of cobalt could drop 70 percnet this year in the Democratic of Congo—which produced 72 percent of the world’s total cobalt last year—as prices have tumbled significantly since early 2018. Many artisanal miners are instead switching to copper.

- The world’s largest chemical maker, BASF SE, has cut its sales and profit forecast for this year due to a deepening economic slowdown, a weakened automotive market and troubles from the U.S-China trade war, reports Bloomberg. Other chemical makers have cut forecasts and German-based BASF says earnings before interest, taxes and special items will be as much as 30 percent lower this year than the previous year.

Emerging Europe

Strengths

- Romania was the best performing country this week, gaining 1.39 percent.

- The Russian ruble was the best performing currency this week, gaining 1.38 percent against the U.S. dollar.

- Consumer staples was the best performing sector among eastern European markets this week.

Weaknesses

- Greece was the worst performing country this week, losing 4.06 percent. The Greek stock market pared some of its recent gains as the market moves from pricing in a pro-business government to focusing on the problems that lie ahead for the local economy.

- The Turkish lira was the worst performing currency this week, losing 1.52 percent against the U.S. dollar. The lira extended declines and stocks fell after the country said it started receiving the first major cargo of a Russian missile-defense system, a purchase that could trigger U.S. sanctions.

- Healthcare was the worst performing sector among eastern European markets this week.

Opportunities

- French industrial output surged in May, indicating the euro area’s second-largest economy resisted a downturn in manufacturing in the currency bloc. Industrial production jumped 4 percent from a year earlier, the most since 2017 and beating even the most optimistic prediction in a Bloomberg poll of economists. The monthly number was the best reading since 2016.

- The European Central Bank (ECB) is using its July meeting to tee up a September move via an easing , tiering, QE bias. The Fed signal increases somewhat the likelihood that ECB President Draghi will decide not to wait and pull the trigger on the whole package in July. According to EvercoreISI, the Bank of England will join the general turn towards more dovish policy.

- The U.K. housing market saw an increase in new buyers for the first time since November 2016 last month, the Royal Institution of Chartered Surveyors (RICS) said. There are several signs that the housing market is starting to stabilize. Sales and new constructions started to pick up for the first time this year in June. A gauge of prices indicated stagnation after four months of declines. U.K. home values have been suffering since the Brexit referendum in 2016, with London hit particularly hard.

Threats

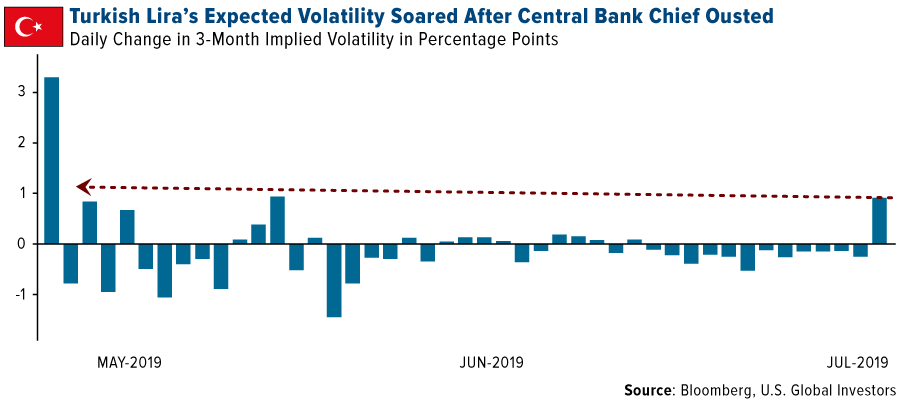

- Turkish President Recep Tayyip Erdogan unexpectedly removed Murat Cetinkaya as central bank governor, after he refused an informal request to resign. Apart from the damage inflicted on the central bank’s credibility, the biggest concern for investors is whether Erdogan will force the central bank to cut rates too aggressively and too quickly. The lira slumped against all of the world’s major currencies on concern that the interest rates will be lowered faster than warranted. The lira’s expected volatility soared after the news broke.

- According to Bloomberg Economics, slower exports largely explained weaker euro area growth last year. However, a close inspection of the data shows the trade war between the U.S. and China only had a small direct effect on European trade. So far, souring global sentiment is mostly to blame for the deteriorating outlook. Still, a further escalation of the trade war, a pivot toward tariffs on Europe’s automakers or a hard Brexit could all deliver another blow to exporters.

- The European Commission cut its Euro area growth and inflation forecasts for next year as trade tensions and policy uncertainty weigh on the region. The EC trimmed its 2020 Euro area GDP projection to 1.4 percent from 1.5 percent due to “increased downside risks”. On inflation, both this year and next were lowered to 1.3 percent. The report strengthens Mario Draghi’s case for further stimulus measures as the ECB prepares to meet in two weeks.

China Region

Strengths

- Taiwan was the best performing country in the region this week, gaining 36 basis points.

- The Indonesian rupiah was the best performing currency in the region this week, up 81 basis points.

- Energy was the best performing sector this week up 18 basis points.

Weaknesses

- China was the worst performing country in the region this week, losing 2.67 percent.

- The Thai baht was the worst performing currency in the region this week, down 42 basis points.

- Consumer goods was the worst performing sector this week down 2.79 percent.

Opportunities

- China’s credit growth exceeded expectations in June, indicating the central bank’s efforts to spur lending are taking effect. Aggregate financing was 2.26 trillion yuan ($329 billion) last month, compared to about 1.4 trillion yuan in May.

- Trump’s trade war is turning out to be a boon for Bangladesh. For the first time in 30 years, Newage Group, a Bangladesh-based garment manufacturer, is sensing an opportunity to sell in the U.S. Newage, a supplier to Hennes & Mauritz AB, has been doing business with European companies for three decades, but is now getting inquiries from Macy’s Inc. and Gap Inc., Asif Ibrahim, vice-chairman of Newage Group, said in an interview. The company executive said inquiries from the U.S. have risen 30 percent.

- Thailand’s struggling tourism industry is finding support with visitors India. At a beachfront hotel on the tropical island of Phuket, the occupancy rate from Chinese clientele has stalled, while bookings from India have begun to rise. Indian arrivals accelerated in recent months due to more direct flights, a visa waiver and, most importantly, increasing wealth. Thailand expects to see a fivefold jump in Indian visitors in the next 10 years.

Threats

- Investors who have stomached the ups and downs of South Korea’s stock market this year have just been dealt another blow: resurgent tensions with Japan. A trade war initiated by Japan to curb exports of materials crucial for the production of memory chips has wiped out over $35 billion in value from the Korean equity benchmark in July. Investors sold shares in semiconductor makers amid rising concern that they will be the biggest victims of the dispute.

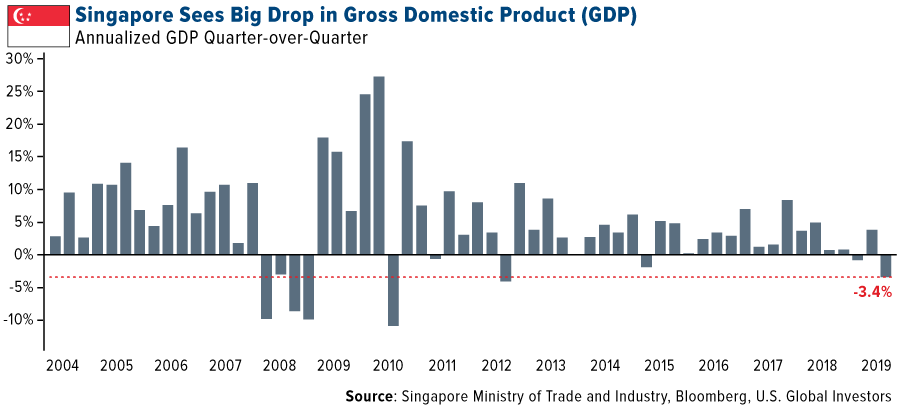

- Singapore’s gross domestic product (GDP) contracted by an annualized 3.4 percent in the second quarter from the previous three months, which is the biggest decline since 2012. Singapore is often held up as a bellwether for global demand given its heavy reliance on foreign trade. An unexpected contraction in Singapore’s economy and a slump in China’s exports sends a warning shot to the world economy as simmering trade tensions wilt business confidence and activity.

- China’s producer price index (PPI), which has a high correlation with nominal GDP, slowed year-over-year in June to zero – the weakest reading in nearly three years. Prices fell 0.3 percent from May. The downward trend accentuates fears of a return of deflation for manufacturing, which would erode company profits and increase debt repayment pressures.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended July 12 was Constant, up 1,547.77 percent.

- During a panel at 92Y in New York this week, the Winklevoss twins, Tyler and Cameron, made a bullish long-term call on bitcoin, saying that the leading cryptocurrency is now at the “bottom of the first inning” and just getting started. The twins, who own an estimated 1 percent of bitcoin’s total reserves, also pointed out that “to shut down bitcoin, you [would] have to shut down the internet… like North Korea.”

- The Miami Dolphins now have an official cryptocurrency: Litecoin. The Litecoin Foundation made the announcement in a press release this week, writing that the collaboration “gives Litecoin the ability to tap into one of the NFL’s largest and most passionate fan bases through in-game branding and advertising opportunities at Hard Rock Stadium, as well as includion across the team’s various online properties and digital content.”

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended July 12 was Posscoin, down 98.94 percent.

- The price of bitcoin fell as much as 8 percent in less than two hours on Thursday in response to Federal Reserve Chairman Jerome Powell’s insistence that Facebook halt its Libra crypto project. “Bitcoin has had a hard time maintaining buying support above $13,000 per coin during the recent relly,” John Todaro, director of digital currency research for TradeBlock, told Forbes. During his Congressional testimony on Wednesday, Powell said that “Libra raises many serious concerns regarding privacy, money laundering, consumer protection and financial stability,” adding that those concerns need to be addressed before Facebook should be allowed to move forward with the project.

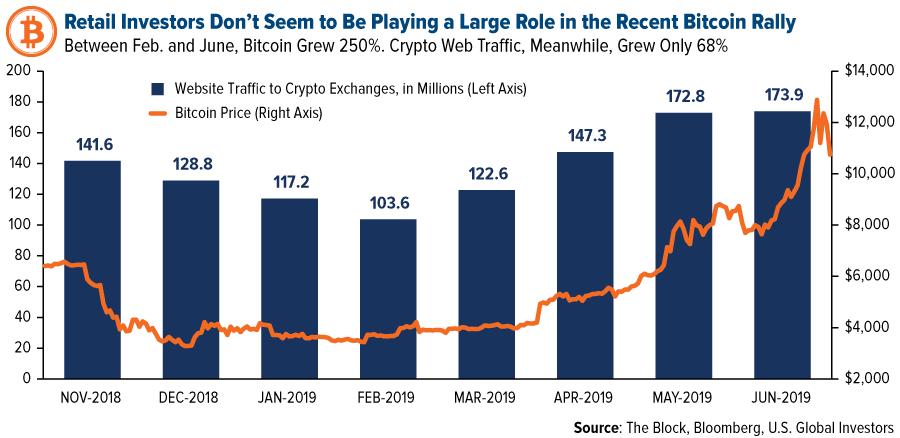

- Retail investors don’t appear to be playing a large role in the recent bitcoin rally, according to Larry Cermak, director of research at The Block. Website traffic to cryptocurrency exchanges—Coinbase, Binance, Bitfinex and others—reached 174 million visits in June, a figure that’s virtually unchanged from the previous month. This came despite bitcoin’s meteoric rise in recent months. Between February and June, the cryptocurrency soared a whopping 250 percent, but over this same period, traffic to exchanges rose only 68 percent. Google searches for crypto exchanges were also muted, Cermak says, a sharp departure from late 2017 when bitcoin last had a massive price surge.

Opportunities

- U.S. regulators potentially cleared the way for dozens of firms to become registered cryptocurrency brokers, writes Bloomberg, by issuing guidance on how securities rules apply to some of the complex issues posed by digital tokens. After the guidance was issued by the SEC, bitcoin jumped as much as 11 percent, to $12,290. Enthusiasts in the space say solving the issue around custody “will pave the way for more widespread investment in digital tokens,” the article continues.

- Bitcoin could “eclipse” the $100,000 barrier by 2021, says Anthony Pompliano, cofounder and managing partner at early-stage venture capital firm Full Tilt Capital. In an interview with Yahoo! Finance’s “The Ticker,” Pompliano reminded listeners that bitcoin is “a fixed supply asset, and so supply and demand economics apply. If there are increases in demand, you’re going to see the price move up.” He also forecast that Facebook’s upcoming Calibra e-wallet would support prices, as it will be given “to hundreds of millions of people, if not billions of people.”

- Blockchain financial services firm Diginex is scheduled to begin trading through a reverse merger with investment holding company 8i Enterprises Acquisition. The Hong Kong-based firm will be listed on Nasdaq following the deal, which is poised to value it at about $276 million, according to Bloomberg.

Threats

- Toward the end of last week, a group of Democrats on the House Financial Services Committee asked Facebook to halt plans for its Libra cryptocurrency, reports MarketWatch. “If products and services like these are left improperly regulated and without sufficient oversight, they could post systemic risks that endanger U.S. and global financial stability.”

- These same concerns were raised during a Congressional testimony this week by Fed Chairman Powell, who suggested that a full and complete assessment of Libra could take longer than 12 months. President Donald Trump knocked bitcoin and Facebook’s proposed coin, writing on Twitter that “Unregulated Crypto Assets can facilitate unlawful behavior, including drug trade and other illegal activities… Similarly, Facebook Libra’s ‘virtual currency’ will have little standing or dependability.” Trump added that if Facebook is interested in becoming a bank, it “must seek s a new Banking Charter and become subject to all Banking Regulations.” Not everyone saw Trump’s criticism as a bad thing. Coinbase CEO Brian Armstrong tweeted: “Achievement unlocked!… First they ignore you, then they laugh at you, then they fight you, then you win.’ We just made it to step 3 y’all.” Billionaire Mark Cuban also spoke unfavorably about Libra this week, saying he was “not a big fan of what [Facebook is] doing there.” Cuban commented that he believes Libra “could be dangerous” and is a “mistake.”

- Police in Spain believe drug traffickers have been using the country’s bitcoin ATMs to launder money, taking advantage of a loophole in European anti-money-laundering controls, according to a report by Bloomberg. Know-your-client (KYC) rules do not apply to the owners of cash machines or crypto exchanges, but that is set to change next year when new European Union (EU) legislation goes into effect, making them subject to the same rules as banks, jewelry dealers and certain other firms.

Leaders and Laggards

| Index | Close | Weekly Change($) |

Weekly Change(%) |

|---|---|---|---|

| Oil Futures | 60.39 | +2.88 | +5.01% |

| 10-Yr Treasury Bond | 2.12 | +0.09 | +4.32% |

| XAU | 85.80 | +2.62 | +3.15% |

| S&P/TSX Global Gold Index | 225.55 | +6.33 | +2.89% |

| S&P Energy | 476.89 | +10.05 | +2.15% |

| Natural Gas Futures | 2.46 | +0.04 | +1.65% |

| DJIA | 27,332.03 | +409.91 | +1.52% |

| Gold Futures | 1,417.80 | +17.70 | +1.26% |

| Nasdaq | 8,244.15 | +82.35 | +1.01% |

| S&P 500 | 3,013.77 | +23.36 | +0.78% |

| Russell 2000 | 1,570.00 | -5.63 | -0.36% |

| S&P Basic Materials | 366.04 | -3.02 | -0.82% |

| Korean KOSPI Index | 2,086.66 | -23.93 | -1.13% |

| Hang Seng Composite Index | 3,782.54 | -48.15 | -1.26% |

| S&P/TSX VENTURE COMP IDX | 576.03 | -10.75 | -1.83% |

| Index | Close | Monthly Change($) |

Monthly Change(%) |

|---|---|---|---|

| Oil Futures | 60.39 | +9.25 | +18.09% |

| XAU | 85.80 | +10.94 | +14.61% |

| S&P/TSX Global Gold Index | 225.55 | +24.48 | +12.17% |

| S&P Energy | 476.89 | +31.63 | +7.10% |

| Gold Futures | 1,417.80 | +81.00 | +6.06% |

| Nasdaq | 8,244.15 | +451.43 | +5.79% |

| DJIA | 27,332.03 | +1,327.20 | +5.10% |

| S&P 500 | 3,013.77 | +133.93 | +4.65% |

| Hang Seng Composite Index | 3,782.54 | +132.78 | +3.64% |

| Russell 2000 | 1,570.00 | +50.21 | +3.30% |

| Natural Gas Futures | 2.46 | +0.07 | +3.02% |

| S&P Basic Materials | 366.04 | +5.44 | +1.51% |

| 10-Yr Treasury Bond | 2.12 | +0.00 | +0.09% |

| Korean KOSPI Index | 2,086.66 | -22.09 | -1.05% |

| S&P/TSX VENTURE COMP IDX | 576.03 | -15.59 | -2.64% |

| Index | Close | Quarterly Change($) |

Quarterly Change(%) |

|---|---|---|---|

| S&P/TSX Global Gold Index | 225.55 | +31.21 | +16.06% |

| XAU | 85.80 | +9.82 | +12.92% |

| Gold Futures | 1,417.80 | +118.50 | +9.12% |

| DJIA | 27,332.03 | +1,188.98 | +4.55% |

| S&P 500 | 3,013.77 | +125.45 | +4.34% |

| Nasdaq | 8,244.15 | +296.79 | +3.73% |

| S&P Basic Materials | 366.04 | +6.98 | +1.94% |

| Russell 2000 | 1,570.00 | -9.14 | -0.58% |

| S&P Energy | 476.89 | -21.79 | -4.37% |

| Oil Futures | 60.39 | -3.19 | -5.02% |

| Hang Seng Composite Index | 3,782.54 | -226.61 | -5.65% |

| Korean KOSPI Index | 2,086.66 | -137.78 | -6.19% |

| Natural Gas Futures | 2.46 | -0.21 | -7.73% |

| S&P/TSX VENTURE COMP IDX | 576.03 | -48.38 | -7.75% |

| 10-Yr Treasury Bond | 2.12 | -0.38 | -15.01% |

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission ("SEC"). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (06/30/2019):

Gran Colombia Gold Corp

SSR Mining Inc

Wesdome Gold Mines Ltd

iShares Silver Trust

Anglo American Platinum Ltd

Impala Platinum Holdings Ltd

BHP Group Ltd

Anglo American Plc

Teck Resources Ltd

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry.

The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies.

The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks.

The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months.

The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange.

The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver.

The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar.

The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500.

The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500.

The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period.

The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500.

The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500.

The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500.

The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500.

The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500.

The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500.

The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns.

The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment.

The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

Producer price index measures the average changes in prices received by domestic producers for their output. It is produced by the Bureau of Labor Statistics and measures price movements from the seller’s point of view. The Small Business Optimism Index is compiled from a survey that is conducted each month by the National Federation of Independent Business (NFIB) of its members. The “core” PCE price index is defined as personal consumption expenditures (PCE) prices excluding food and energy prices. Standard deviation is a measure of the dispersion of a set of data from its mean. The more spread apart the data, the higher the deviation. Standard deviation is also known as historical volatility. The ISM manufacturing composite index is a diffusion index calculated from five of the eight sub-components of a monthly survey of purchasing managers at roughly 300 manufacturing firms from 21 industries in all 50 states.