Keep Calm and Stay Long: This Gold Price Correction Is Normal and Healthy

Date Posted: September 25, 2020

Read time: 55 min

In the nearly six years since Greg Abbott has been governor of Texas, the Lone Star State has been the number one destination for U.S. businesses looking to relocate.

By Frank Holmes

CEO and Chief Investment Officer

U.S. Global Investors

Gov. Greg Abbott on the size of Texas’ economy compared to Russia’s: “We’re bigger than Putin.”

Photo of Greg Abbott by: Gage Skidmore from Peoria, AZ | Attribution 2.0 Generic (CC BY 2.0) Photo of Putin by: kremlin.ru | Attribution 4.0 International (CC BY 4.0)

In the nearly six years since Greg Abbott has been governor of Texas, the Lone Star State has been the number one destination for U.S. businesses looking to relocate.

That includes California businesses. In 2018 and 2019, as many as 660 California-based companies pulled their stakes up and moved to greener pastures in Texas, where the cost of doing business is roughly 10 percent below the national average.

Next up is Tesla. The electric vehicle (EV) company is currently in the process of building its fourth factory in the Texas capital of Austin, a growing tech hub with a young, highly educated population.

A city in Texas may also be named headquarters to TikTok, the popular video-sharing app whose fate is still in limbo after Oracle and Walmart struck a deal to jointly buy the U.S. service from TikTok’s Chinese parent company, ByteDance. This could bring as many as 25,000 high-paying jobs to the Lone Star State, according to President Donald Trump, who favors Texas as the app’s HQ.

Gov. Abbott touched on jobs, the economy and more during a Young Presidents’ Organization (YPO) event I had the pleasure of attending this week just outside San Antonio. He pointed out that the Texas GDP, at $1.9 trillion, is bigger than the economies of Canada, Brazil and Russia.

"We’re bigger than Putin,” the governor quipped, eliciting laughter.

Abbott also briefly addressed the recent protests across the nation, some of which have unfortunately turned violent. Texas would always support people’s First Amendment right to peacefully protest, he stressed, but once demonstrations resorted to rioting and looting, they were no longer protected by the Constitution.

Last week, I shared with you that the multi-city riots between May and June alone are now estimated to be the costliest civil disorders in U.S. history, costing the insurance industry between $1 billion and $2 billion in property damage.

This isn’t the first time I’ve praised our great home state, and it won’t be the last. An article I wrote four years ago on why everyone wants to move to Texas ended up being a huge viral hit on LinkedIn. Two years ago, Gov. Abbott tweeted another article I wrote, “6 Reason Why Texas Trumps All Other Economies.”

Gold Correction Is Normal and Healthy, Says the DNA of Volatility

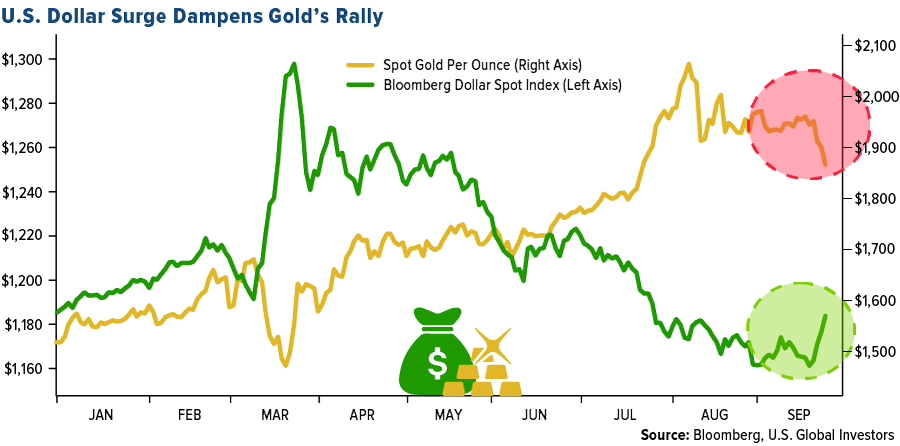

Gold had its worst week since March, falling some 4.6 percent from last Friday, as the U.S. dollar staged a rally against the euro. The price of bullion closed below $1,900 an ounce on Wednesday for the first time since July 23 and is now down about 10 percent from its high of $2,075, putting it in correction territory.

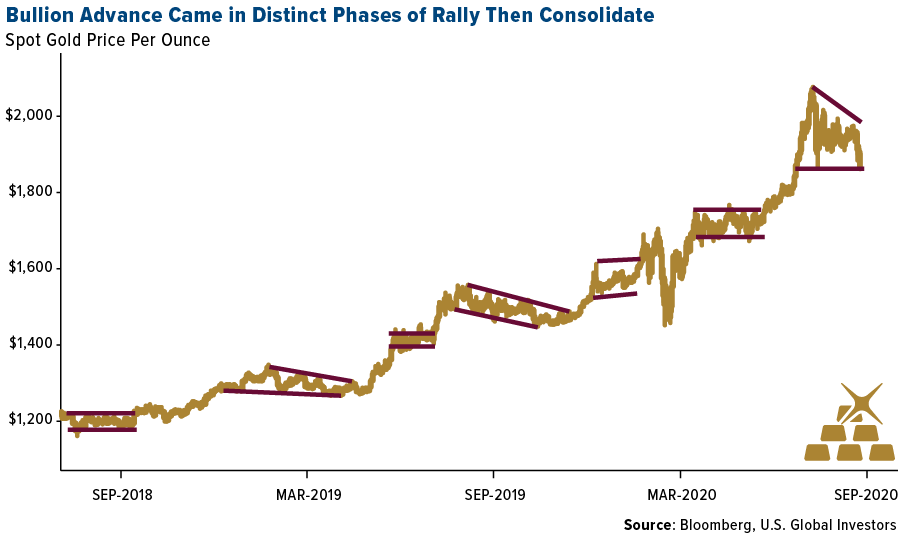

I’ve already seen numerous headlines questioning whether this is the end of the gold rally. Hardly. As I’ve explained many times before, corrections such as this are normal and healthy. They’re a part of gold’s DNA of volatility. During the monster rally of the 2000s that culminated in gold hitting its previous record high of $1,900, there were several significant pullbacks, some of them exceeding 20 percent.

Take a look below. Gold is now more oversold on the short-term, 10-day relative strength index (RSI) than at any other time since the golden cross took place in January 2019. The last time the precious metal was this oversold, in mid-March, gold fell below not just its 50-day moving average but also its 200-day average. We’re not quite there yet—gold is trading below its 50-day but still well above the 200-day—but had you bought the March dip, you would have seen your position increase 40 percent over the next five months.

Looking at a longer-term period, gold doesn’t yet appear to be oversold. The oscillator chart below is based on the daily gold price over a rolling 60-day period, which is equivalent to a three-month quarter. As you can see, gold has recently fallen out of overbought territory and is returning to its five-year mean, or average price. It’s important to remember that for the 60-day period, a move of one standard deviation is equivalent to 10 percent. In other words, the price of gold needs to changer by 10 percent to record a move of one standard deviation.

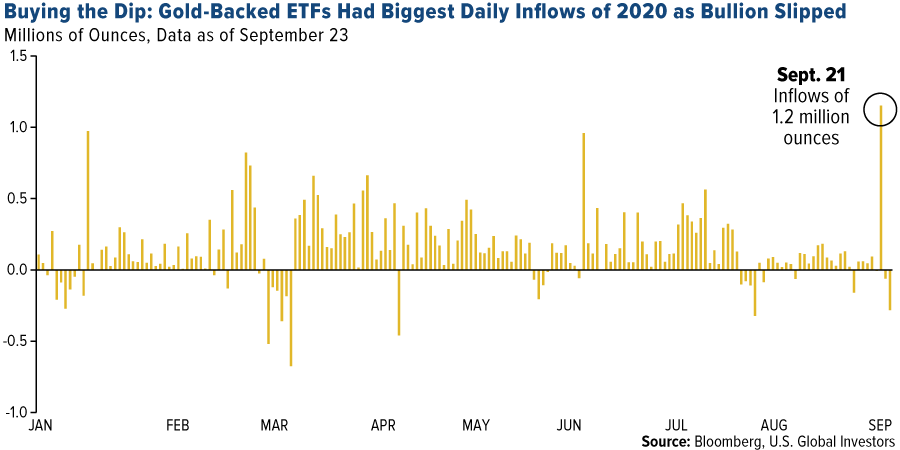

Biggest One-Day Inflows into Gold-Backed ETFs

With real rates still negative (and likely to remain that way for some time longer), and unprecedented money-printing threatening to heat up inflation, I believe it only makes sense to buy the dips at this time.

That’s exactly what many investors did earlier this week. On Monday, when the yellow metal fell nearly 2 percent, investors added 1.2 million ounces to ETFs backed by physical gold. That was the most for a single day in 2020.

Randy Smallwood: Precious Metals in “Golden Times”

Gold and silver are in “golden times” right now, according to Wheaton Precious Metals’ president and CEO Randy Smallwood during an online Denver Gold event earlier this week. The “helicopter money” from governments will continue to be highly supported of prices.

Randy is also optimistic of base metals, saying they were likely to be the bulk of streaming deal opportunities. “It’s good to see money going to the ground in the base-metals space,” he commented.

Wheaton Precious is planning to list on the London Stock Exchange, which will put the $23 billion streaming company on the radar of United Kingdom investors who are seeking to gain equity exposure to precious metals. Wheaton currently trades in Toronto and New York.

I believe this is a well-timed decision on the part of Randy, who was named the new chair of the World Gold Council (WGC) earlier this month. According to Edison Investment Research, precious metal companies listed in London “have tended to outperform their peers, with 52 percent of London-listed companies outperforming the gold price over the period of the worst depredations of the coronavirus so far this year, compared with 39 percent globally.”

Further, Wheaton Precious “will provide premium-quality, geared exposure to precious metals prices and fill a void for investors left by the departure of Randgold Resources in December 2018 after it was acquired by Barrick,” analyst Charles Gibson wrote in a note dated September 22.

As you know, Wheaton is one of our favorite mining stocks. At present it pays out 30 percent of its cash flow in dividends, but this could rise to between 40 percent and 50 percent with higher metal prices, Randy says.

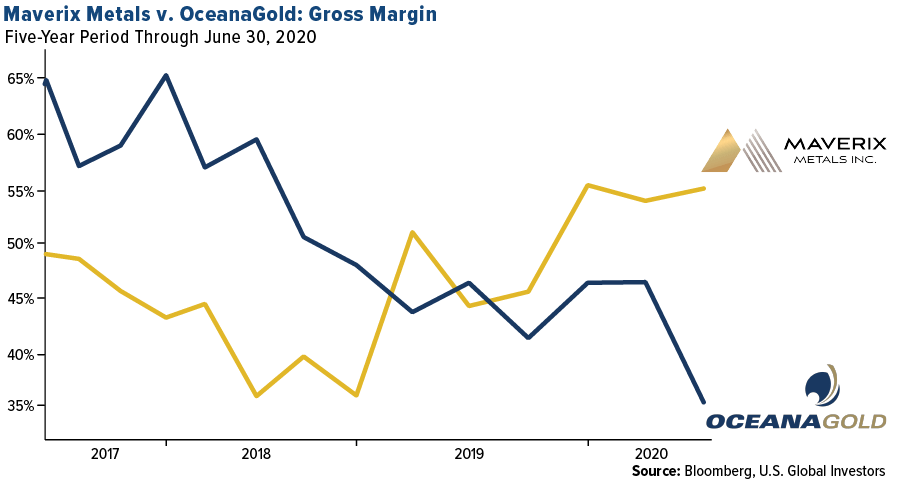

Maverix Metals: A Rising Star in the Streaming Space

Another royalty and streaming company we have our eye on is Maverix Metals, formed in 2016 after the company acquired a package of assets from Pan American Silver. This week, Maverix entered into a binding purchase and sale agreement to buy a portfolio of 11 royalties from Newmont, including the Camino Rojo gold and silver project in Mexico.

The transaction, according to a note by Raymond James, “provides Maverix with potential near-term gold equivalent ounce (GEO) and cash flow growth from five development assets in the Americas, while adding longer-term optionality through the six exploration properties.”

Raymond James has given the stock an Outperform rating, with a price target of C$7.50.

We like the stock and, based on our quant stock-picking model, added it our portfolio. This replaced Australia-based producer OceanaGold. Maverix’ gross margin overtook OceanaGold’s in 2019 and has only continued to increase, which is why we made the rotation.

Since it began trading in July 2016, Maverix has outperformed OceanaGold and other global gold stocks.

JPMorgan to Pay Record $1 Billion Spoofing Penalty

On a final note, some of you may have heard that JPMorgan & Chase, one of the world’s largest gold and precious metal traders, is set to pay close to $1 billion to resolve market manipulation investigations by U.S. authorities that have been ongoing for months now. The settlement would allow JPMorgan to continue normal operations without being indicted.

Two former JPMorgan traders are being alleged of “spoofing,” or placing false orders with no intent to execute them to trick others into moving prices in a desired direction.

Unfortunately, market manipulation in the global gold market is real, but there are those who are fighting to expose it. If you recall from May of last year, I interviewed Chris Powell, secretary/treasurer at Gold Anti-Trust Action Committee (GATA).

We briefly discussed the JPMorgan spoofing scandal, during which Chris shared an interesting thought on John Edmonds, one of the traders: “He was allegedly doing it with the knowledge and counsel of his superiors, and if it were done on behalf of the government, presumably it’s legal under the Gold Reserve Act… [But] I can’t imagine the Justice Department would be prosecuting him if his trading was being conducted on behalf of the U.S. government.”

Do you know the world’s top 10 gold producing countries? Click the banner below to find out!

Gold Market

This week spot gold closed at $1,861.58, down $89.28 per ounce, or 4.58 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 7.51 percent. The S&P/TSX Venture Index came in off 6.72 percent. The U.S. Trade-Weighted Dollar rose 1.78 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Sep-24 | Hong Kong Exports YoY | -3.0% | -2.3% | -3.0% |

| Sep-24 | Initial Jobless Claims | 840k | 870k | 866k |

| Sep-24 | New Home Sales | 890k | 1011k | 965k |

| Sep-25 | Durable Goods Orders | 1.5% | 0.4% | 11.7% |

| Sep-29 | Germany CPI YoY | 0.0% | — | 0.0% |

| Sep-29 | Conf. Board Consumer Confidence | 90.0 | — | 84.8 |

| Sep-29 | Caixin China PMI Mfg | 53.1 | — | 53.1 |

| Sep-30 | ADP Employment Change | 650k | — | 428k |

| Sep-30 | GDP Annualized QoQ | -31.7% | — | -31.7 |

| Oct-1 | Initial Jobless Claims | 850k | — | 870k |

| Oct-1 | ISM Manufacturing | 56.0 | — | 56.0 |

| Oct-2 | Eurozone CPI Core YoY | 0.5% | — | 0.4% |

| Oct-2 | Change in Nonfarm Payrolls | 900k | — | 1371k |

| Oct-2 | Durable Goods Orders | — | — | 0.4% |

Strengths

- The best performing precious metal for the week was gold, but still down 4.58 percent. Gold took a hit this week from a stronger dollar and investors bought the dip. The SPDR Gold Shares saw an inflow of more than 30 tons on Monday. Gold-backed ETFs had the biggest day of inflows in 2020 collectively on Monday of 1.2 million ounces. This shows confidence in the metal despite prices swings. With this past week also being one of the bigger gold mining industry investor conferences, the rush to flush the gold miner’s positive message of free cash flow and rising dividends by gold bears didn’t resonate for long.

- Great Dyke Investments, owned by Russia’s Vi Holding and Zimbabwean investors, cleared a hurdle to develop Zimbabwe’s biggest platinum mine. The African Export-Import Bank completed a due diligence study allowing the company to proceed with a $500 million syndicated funding program. Once complete, the project is expected to produce 860,000 ounces of platinum group metals and gold a year and would significantly boost the country’s economy.

- Maverix Metals is acquiring a portfolio of 11 gold royalties from Newmont for upfront consideration of $75 million and contingent payments of up to $15 million. Ghana plans to list its gold royalty fund Agyapa Royalties on the London Stock Exchange in October and plans to raise $400 to $500 million from the IPO, Reuters reports. The fund share will also be listed on the Ghanian Stock Exchange.

Weaknesses

- The worst performing precious metal for the week was silver, down 14.55 percent as expected with the selloff in gold. Silver is back in a bear market. After approaching $30 an ounce in mid-March, silver suffered severe losses this week on a resurgent U.S. dollar and concerns about growth. The metal traded below its 50-day moving average for the first time since May.

- The key driver of gold prices right now is the U.S. dollar – and it’s making a comeback. The two assets historically trade in the opposite direction. The dollar’s vigor is linked to fading hopes of another stimulus package from the U.S., but it shouldn’t last since Federal Reserve policy will remain expansionary for years.

- Fresnillo Plc, one of the world’s biggest silver producers, took the rare step of locking in gains from the silver’s almost 50 percent rally this year, reports Bloomberg. The Mexican-focused mine said it has hedged 7 percent of next year’s output with a floor of $20 an ounce and a ceiling of $50 an ounce. Hedging has been shunned by investors who in the past spent at least $10 billion unwinding unprofitable forward sales when prices surged.

Opportunities

- According to Citigroup, gold could hit a new record before the year-end aided in part by the risks surrounding the U.S. presidential election. Analysts including Aakash Doshi said in a quarterly commodities outlook that uncertainty over election results could “be under-appreciated by precious metal markets.” Bloomberg notes the bank implies a surge of more than $200 for bullion futures from current levels.

- Even though gold is trading lower, that doesn’t mean the rally is over, writes Bloomberg’s Eddie van der Walt. Gold’s move that started below $1,230 in 2018 has been filled with pauses. Gold is trading at the lower end of its pennant-range and the “path of least resistance is higher.” Bullion hit its new record high just last month above $2,075 due to global stimulus, negative real rates and a weaker dollar.

- After announcing a surprise 3.5-fold mining extraction tax increase in Russia last week, the government slightly reversed course. Silver mining will be excluded from the tax and new mining projects will also be shielded. Canada’s Wheaton Precious Metals is planning to list of the London Stock Exchange by the end of this year, said CEO Randy Smallwood. The royalty and streaming company hopes to tap into investor demand for streaming deals.

Threats

- In an open letter to the mining industry, a coalition of prominent gold investors and money managers said performance of mining companies “continues to fall short.” The investors were targeting issues such as executive compensation and directors who own few shares of the companies they represent. “Though the performance of gold mining stocks has been noteworthy recently, we believe that performance continues to fall short in the areas of corporate governance, alignment of incentives and strategic vision & communication with investors,” the group said in the letter released Sunday, the first day of the annual Denver Gold Group Americas conference.

- Two precious metals dealers and their firms are the target of a joint civil enforcement action filed in a Texas court by the Commodity Futures Trading Commission (CFTC) and 30 state regulators, reports Bloomberg. Metals.com, Barrick Capital and its principals have a complaint against them charging the defendants “with executing an ongoing nationwide fraud that solicited and received more than $185 million in investor funds to purchase fraudulently overpriced gold and silver bullion.”

- Gold fell to a two-month low as the dollar extended gains and hopes for further U.S. fiscal stimulus faded, writes Bloomberg. “If global growth concerns continue to push up the U.S. dollar, like we have seen this week, we could see some near-term headwinds for the precious metal,” Vivek Dhar, commodities analyst with Commonwealth Bank of Australia said.

Index Summary

- The major market indices finished mixed this week. The Dow Jones Industrial Average lost 2.61 percent. The S&P 500 Stock Index fell 1.74 percent, while the Nasdaq Composite rose 0.03 percent. The Russell 2000 small capitalization index lost 4.39 percent this week.

- The Hang Seng Composite lost 4.64 percent this week; while Taiwan was down 4.97 percent and the KOSPI fell 5.29 percent.

- The 10-year Treasury bond yield fell 3 basis points to 0.656 percent.

Domestic Equity Market

Strengths

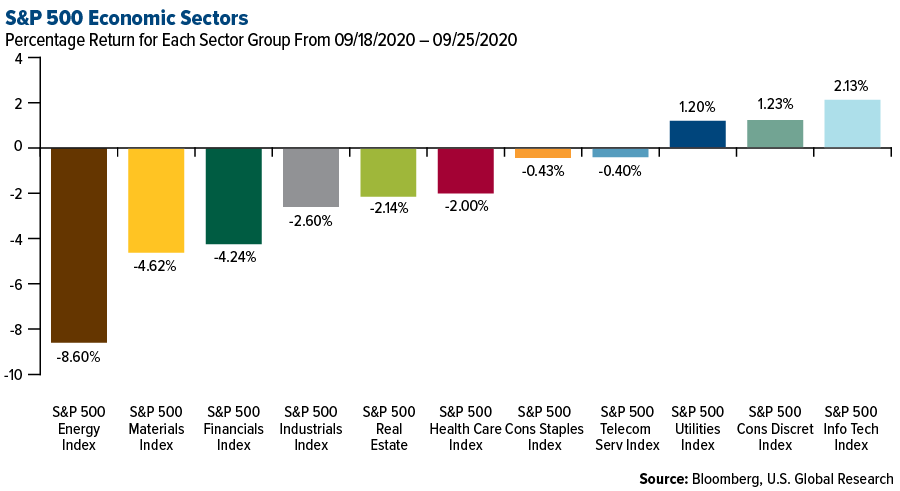

- Information technology was the best performing sector of the week, increasing by 2.13 percent versus an overall decrease of 0.72 percent for the S&P 500.

- Twitter was the best performing S&P 500 stock for the week, increasing 9.19 percent.

- Jack Ma’s Ant is lifting its IPO funding target to $35 billion, putting it on track for a record debut. Ant’s record IPO would value the firm at about $250 billion, according to Bloomberg.

Weaknesses

- Energy was the worst performing sector for the week, decreasing by 8.60 percent versus an overall decrease of 0.72 percent for the S&P 500.

- Apache was the worst performing S&P 500 stock for the week, falling 22.13 percent.

- While some dip buying is taking place, sentiment has switched to risk off, with pessimism seeping in about the prospect of further fiscal stimulus to support the world’s biggest economy. The S&P 500 Index closed its fourth straight weekly drop, its longest losing streak in more than a year.

Opportunities

- Secretive data-miner Palantir could fetch a $22 billion price-tag at its market debut next week. The controversial company is choosing to bypass the traditional IPO route, and opt for a direct listing instead.

- John Stoltzfus, Oppenheimer chief investment strategist, told CNBC that the recent market pullbacks signal a bargain buying opportunity for growth companies in the U.S., writes Business Insider. He said that the U.S. has been outperforming most of the markets around the world, and its innovation makes it the best place to invest.

- Jet fuel demand will accelerate in 2021 says Goldman Sachs, driven by availability of a COVID-19 vaccine by the second-quarter." We do not believe that jet fuel demand has peaked and see jet as an area of long-term demand growth in this decade," analysts said. This would imply higher demand for air travel, and thus benefit airline companies.

Threats

- As investors continue to grapple with a rise in COVID-19 cases and the uncertainty of more fiscal stimulus from Congress, the technical picture of the stock market "has deteriorated," Morgan Stanley said in a note on Monday. After both the S&P 500 and Nasdaq 100 indices closed below their respective 50-day moving averages, the next level of support investors should watch is the 200-day moving average, according to the note. A continued market sell-off to the 200-day moving average would represent downside potential of 5 percent and 12 percent in the S&P 500 and Nasdaq 100, respectively, based off of Monday’s closing prices.

- Nikola founder Trevor Milton resigned from the company’s board following fraud allegations. Hindenburg Research, a short-seller, published a lengthy report accusing the electric truck maker of fraud on September 10.

- The European Union wants to give itself the power to kick U.S. technology giants out of Europe. A regulatory blueprint includes massive penalties to force tech companies to sell off their European operations and even shut them out of the European single market.

The Economy and Bond Market

Strengths

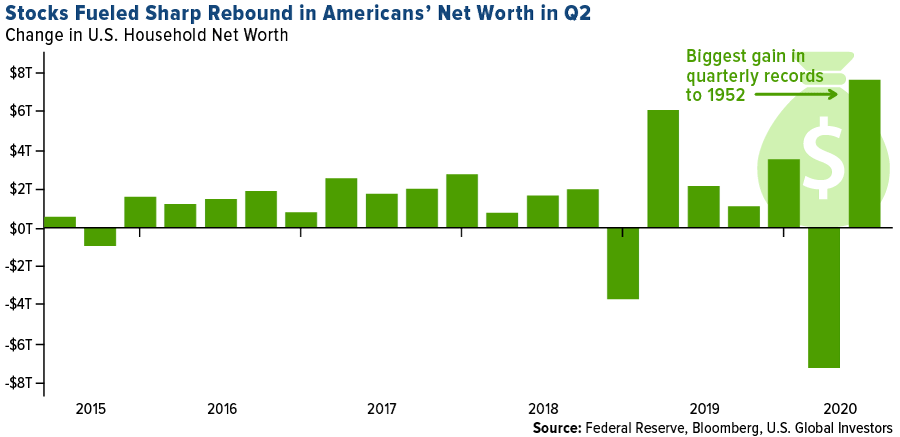

- American households’ net worth surged in the second quarter to surpass the pre-pandemic peak after a virus-driven slump at the start of the year. The $7.6 trillion, or 6.8 percent, gain was the largest in quarterly data back to 1952, and more than erased a record setback in the previous three months, a Federal Reserve report showed Monday.

- The housing market continued to boom in August, as low mortgage rates and pandemic-driven demand fueled new home sales above 1 million for the first time in 14 years. Sales of new single-family homes rose 4.8 percent in August from July to a seasonally adjusted annual rate of 1.01 million, the Commerce Department said Thursday. Economists polled by the Wall Street Journal had expected a 0.3 percent decline to 898,000. August sales were 43 percent above the year-earlier level.

- Business activity in the U.S. manufacturing sector is seen expanding at a robust pace in September with the IHS Markit’s advanced Manufacturing PMI rising from 53.1 in August to 53.5. The reading came in slightly better than the market expectation of 53.2. “US businesses reported a solid end to the third quarter, with demand growing at a steepening rate to fuel a further recovery of output and employment," said Chris Williamson, chief business economist at IHS Markit.

Weaknesses

- The number of first-time filers for unemployment benefits were slightly higher than expected last week as the labor market continues its sluggish recovery from the coronavirus pandemic. The Labor Department reported Thursday that initial jobless claims for the week ending September 19 came in at 870,000, adjusted for seasonal fluctuations. Economists polled by Dow Jones expected first-time claims at 850,000, down slightly from the previous week’s 860,000. Thursday’s data comes as U.S. lawmakers struggle to move forward with a new fiscal stimulus package, something economists and the Federal Reserve argue is needed for the economic recovery to continue.

- After reporting sharp increases in new orders for U.S. manufactured durable goods over the past few months, the Commerce Department released a report on Friday showing durable goods orders climbed much less than expected in the month of August. The Commerce Department said durable goods orders rose by 0.4 percent in August after soaring by an upwardly revised 11.7 percent in July. Economists had expected durable goods orders to surge up by 1.5 percent.

- Federal government debt outstanding has ballooned by an annualized 58.9 percent on lawmakers’ fiscal relief efforts to backstop the economy. Now totaling over $26.7 trillion, the U.S. debt-to-GDP ratio is one of the highest in the world. Though the effects of the coronavirus pandemic are expected to fade through the next year, deficits linked to fiscal stimulus will drive debt to worrying levels. The Congressional Budget Office (CBO) expects federal debt to reach 98 percent of the U.S.’s gross domestic product (GDP) this year and 104 percent in 2021. For comparison, the previous record was 106 percent, seen just after World War II.

Opportunities

- Whether the selloff in markets continues may depend mostly on the U.S. employment data that will be released next Friday. Nonfarm payrolls are expected to have risen by another 850,000 in September, from almost 1.4 million in August, pushing the unemployment rate down to 8.3 percent, from 8.4 percent previously. Indeed, initial and continued jobless claims declined between mid-August to mid-September, which is the period this employment report will cover, diminishing the risk of a major negative surprise.

- Next Thursday’s ISM Manufacturing Survey is likely to show expansion continued through the end of the third quarter at a steady clip. Recent regional Fed surveys have been strong. The forecast is for a reading of 56, solidly above the 50 expansion/contraction level.

- Next Tuesday, the Conference Board Consumer Confidence index will likely post a small improvement. In August, it fell to a new pandemic low while the economy continued to slowly recover. Since then, net job gains have remained solid, a net positive for sentiment. Expectations are for an index reading of 90, up from the prior 84.8.

Threats

- The expiration of add-on unemployment benefits is likely to become more apparent in next Thursday’s personal income data. Expectations are for a drop of 2.5 percent.

- Jobless claims remain stubbornly high and any signs of a sustained downtrend are still elusive. The level of claims remains extremely elevated, signaling continued dislocation in the labor market recovery. Next Thursday’s initial jobless claims are forecasted to be 850,000.

- The U.S. is facing a dollar collapse by the end of 2021 and over a 50 percent chance of double-dip recession, economist Stephen Roach says. Historically, the U.S. has seen economic output rise briefly and fall back lower in eight of the past 11 business cycle recoveries, Roach said.

Energy and Natural Resources Market

Strengths

- The best performing commodity for the week was lumber, up 4.87 percent on strong housing demand. Wood product supplies are tight however, with logging and lumber mills running short on labor access. Rhodium hit a record $14,500 an ounce last week and could keep running. Uve Kupka, CEO of Heraeus Precious Metals North America, says rhodium could keep soaring due to expanded pollution laws driving demand. “$20,000 is possible. Will this happen this year? I don’t know. In one to three years, it’s possible.”

- China’s President Xi Jinping said at a United Nations General Assembly on Tuesday that the country plans to be carbon neutral by 2060. The world’s most populous nation and top energy user said it plans to spend more on green technologies in the next five years. Xi reiterated his goal for emissions to peak before 2030.

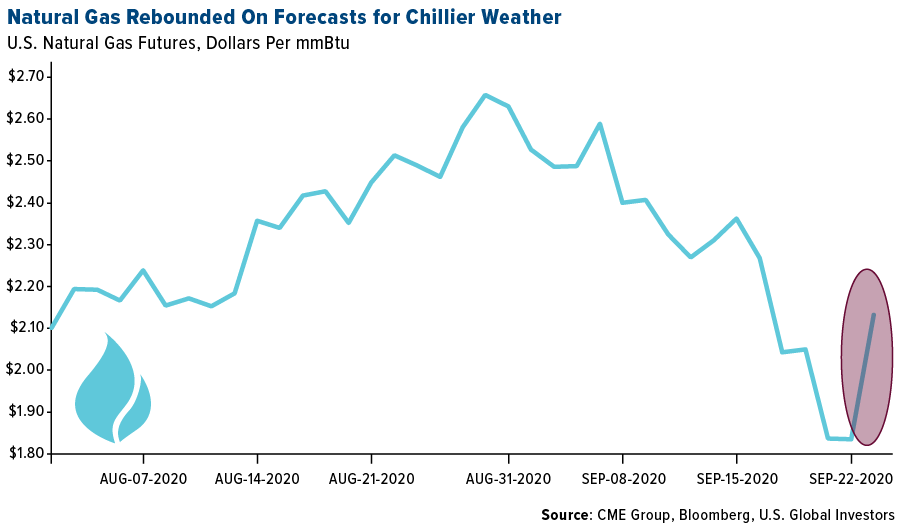

- Despite U.S. natural gas prices falling 22 percent last week, traders are still bullish on the fuel due to expectations for a colder winter. Futures for delivery in December through March are trading above $3. A Bloomberg News survey of traders and analysts say winter prices could rise higher and even test $4.

Weaknesses

- The worst performing commodity for the week was crude palm oil, down 8.38 percent for the week with expectations that Malaysia palm oil production could increase in September. FTS International, a U.S. fracking services provider, will file for bankruptcy as companies that rent out pumps for blasting oil-soaked shale rock have been among the hardest hit by the crude crash and pandemic, reports Bloomberg. More than 220 oilfield service companies with at least $95 billion in combined debt have filed for bankruptcy since 2015, according to Haynes & Boone.

- Battery makers aren’t producing fast enough according to Elon Musk. Speaking at Tesla’s Battery Day event this week, Musk said they will face “significant shortages” from 2022 if it doesn’t start producing its own batteries. The world’s top three battery makers that all supply Tesla – LG Chem, Contemporary Amperex Technology and Panasonic – all fell on the news. Musk added that Tesla is still trying to reduce battery costs and aims to manufacture at $25,000 electric vehicle in the next three years. Investors sold off Tesla on their ambitious plans to control the supply chain from car production down to lithium mining from clays in Nevada are problematic.

- Marco Dunand, head of commodities trade Mercuria Energy Group, says global oil markets won’t be able to absorb planned production increases by OPEC+ members as demand remains weaker than expected. Dunand said in an interview “we do not need the extra oil.” This comes as Libya has restarted oil exports at a third port this week.

Opportunities

- Exchange-traded funds (ETFs) tracking clean energy share indexes have jumped fourfold in the last 12 months. BloombergNEF analysis shows that nine ETFs focusing on shares in sectors such as renewable power, energy efficiency and fuel cells saw their aggregate market capitalization increase from $1.7 billion to $6.6 billion in the one-year period ended September 18.

- Airbus unveiled a trio of zero emissions passenger aircraft powered by hydrogen that could take to the skies by 2035. The jet maker’s new designs feature a turbofan aircraft with a range of 2,000 nautical miles, a modified gas-turbine engine and capacity for 200 passengers.

- Goldman Sachs says green hydrogen, where renewable energy powers the electrolysis of water, is a once-in-a-lifetime opportunity and could be worth $11.7 trillion by 2050. London-based analysts led by Alberto Gandolfi say green hydrogen could turn into the largest electricity consumer and double power demand in Europe.

Threats

- Russia’s Finance Ministry told mining companies that the surprise plan to more than triple mineral-extraction taxes in 2021 is a done deal, reports Bloomberg. The ministry plans to raise taxes by 3.5-fold to bring as much as $774 million into the state budget next year, which is facing a deficit this year. Just days later First Deputy Prime Minister Andrey Belousov agreed with mining executives that new mining projects should be safeguarded from the tax hike.

- Tom Collier, head of the Northern Dynasty Mineral’s Pebble Limited Partnership unit has submitted his resignation after being tapped making comments boasting of his ties to state and federal leaders. The CEO was secretly taped EIA investigators posing as investors. The contentious Alaska Pebble mining project is argued to irreparably harm indigenous communities and one of the world’s largest sockeye salmon fishery. The project has garnered heavy news attention due to Donald Trump Jr.’s involvement.

- Iron ore is having one of its worst weeks of the year, writes Bloomberg, falling again on Friday as investors bet China’s demand frenzy may not stay strong enough to match a pickup in supply. Steel markets are easing and iron ore availability is rising as stockpiles in China rose this week, adding to signs of slackness.

Emerging Europe

Strengths

- Turkey was the best performing country this week, gaining 1 percent. Equites moved higher as investors’ confidence improved after geopolitical tensions with Greece eased and the central bank unexpectedly changed its monetary policy, hiking its main rate by 200 basis points. Steel producer, Cemtas Celik Makina, was the best equity trading on the Istanbul Stock Exchange, gaining 23 percent over the past five days.

- The Turkish lira was the best relative performing currency this week, losing 1.3 percent. Emerging currencies declined with the dollar sharply moving higher over the past five days. However, the lira recorded smaller losses against its peers due to the country’s unexpected decision to hike rates.

- Industrials was the best performing sector among eastern European markets this week.

Weaknesses

- Hungary was the worst performing country this week, losing 5 percent. The Budapest Stock Exchange underperformed its central emerging European peers due to a sharp sell-off in the banking sector. Shares of the largest lender, OTP Bank, declined by 10.2 percent over the past five days after the government extended a loan repayment moratorium. The country’s central bank unexpectedly hiked its main rate by 15 basis points.

- The Polish zloty was the worst performing currency in the region this week, losing 3.8 percent. All of emerging Europe’s currencies depreciated over the past five weeks as the dollar spiked. The Polish zloty underperformed its peers due to a ruling coalition crisis after the junior party voted against government-backed legislation in parliament.

- Energy was the worst performing sector among eastern European markets this week.

Opportunities

- Despite a coronavirus resurgence, economic development in Germany was reported at 93.4 in September, the highest reading since February. French business confidence grew in September to the highest level since just before the coronavirus outbreak, rising to 92 from 90 in August. Companies are assessing their current business situation more optimistically than in the previous months.

- The central bank of Turkey positively surprised the market this week with its decision to hike its main rate by 200 basis points. On top of that, the banking regulator eased swap rules for Turkish banks with non-residents, meaning the lira will be more accessible to international investors in swap markets, a step toward normalization, Ilgin Erdogan says from Wood & Company. These moves lower the risk of lira’s further devaluation and could restore investors’ confidence in Turkish equites.

- Reuters cited comments by ECB chief economist Philip Lane on Thursday, who said containing the coronavirus must be a priority for policymakers as a surge in infections would damage consumer and investor confidence in the economy. Lane highlighted that its baseline scenario in the ECB’s staff projections factors in a medical solution potentially fund over the course of next year.

Threats

- JPMorgan is moving about 200 billion euros from the U.K. to Frankfurt as a result of Brexit. The firm plans to migrate its assets to Germany by the end of the year. Banks are making sure they have sufficient operations in the EU so they can service clients if U.K.-based firms lose passporting rights in a post-Brexit trade deal. U.K. officially left the EU on January 31, 2020, and the transition period is due to end December 31, 2020. If a deal between the EU and the U.K. is not brokered before the transition period ends in December, then the U.K. will drop out of both the customs union and the single market.

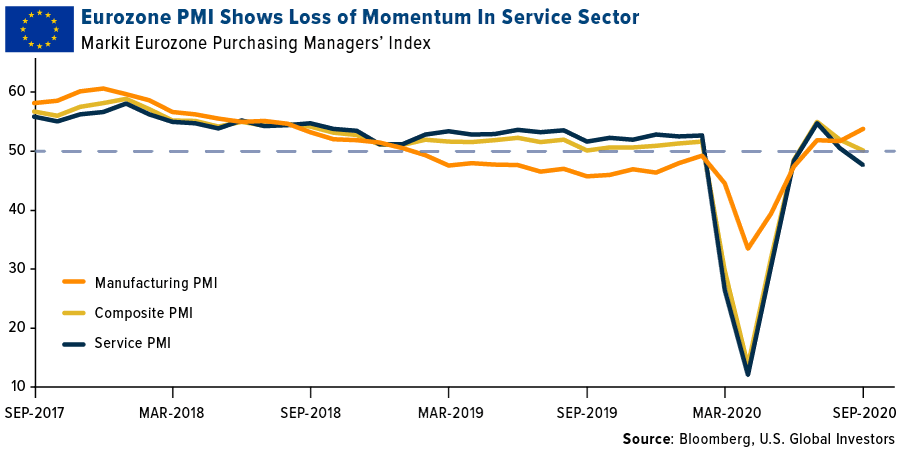

- The EU composite PMI fell to 50.1 from 51.9. Consensus was no change. Manufacturing PMI stayed above the 50 level, but the EU’s Service PMI fell below. The service sector was negatively affected by a slowdown once again in tourism and reinstated restrictions.

- Coronavirus cases are on the rise in Europe. The Czech Republic’s new coronavirus cases now bypass France’s as the EU’s second-worst country based on the 14-day cumulative number of infections per 100,000 people. The Czech health minister quit on Monday, saying the government needs a different strategy to tackle a spike in the new coronavirus cases. The U.K.’s chief scientific and medical advisers have warned that the country is on course for up to 50,000 new daily cases of COVID-19 by mid-October. The U.K. imposed new pandemic restrictions, focusing on hot spots without locking down the entire country.

China Region

Strengths

- Vietnam was the best performing country this week, gaining 8 basis points. The country will hold strategic partnership talks with the United Kingdom next week and potentially sign a trade deal agreement. Thanh Thanh Cong – Bien Hoa, an agricultural producer, was the best performing equity among the stocks trading in the iShares Vietnam ETF (VNM), gaining 6.7 percent over the past five days.

- The Philippine peso was the best performing currency this week, gaining 1 basis point. The currency was little changed ahead of next week’s central bank meeting. Most Bloomberg economists predict rates to remain unchanged.

- Healthcare stocks were the best performing among the stocks trading on the Hong Kong Stock Exchange.

Weaknesses

- South Korea was the worst performing market this week, losing 5.5 percent. Equites sold off on increased tension with North Korea. Consumer confidence declined to 79.4 in September from 88.2 the prior month. Shin Poong Pharmaceutical was the worst performing equity among the stocks trading in the iShares MSCI South Korea ETF (EWY), losing 31.3 percent over the past five days. The company announced a shares sale plan at a discount.

- The Thailand baht was the worst performing currency this week, losing 15 basis points. The currency was weighed down by equity outflows as well as political and economic concerns. Lawmakers failed to reach an agreement to amend the constitution, further upsetting anti-government protestors calling for more democracy and reform of the monarch. Global investors sold a net $40.6 million of Thai equites on September 24, which marked a seventh day of outflows, according to Bloomberg.

- Financial stocks were the worst performing among the stocks trading on the Hong Kong Stock Exchange.

Opportunites

- Despite the MSCI Indonesia Index suffering poor performance of negative 10 percent in September so far, Tellimer is still positive on the country. The research firms says Indonesia enjoys a large and youthful population, strong manufacturing potential, low foreign currency rates and low twin-deficits.

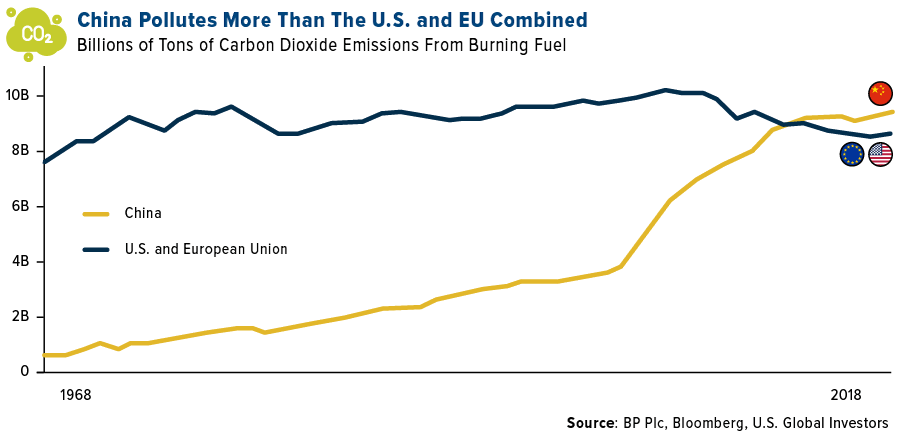

- China has said it hopes to become carbon neutral by 2060. According to IHS Markit, China will have to increase solar generation to 2,200 gigawatts and wind to 1,700 gigawatts to make this happen. At the end of 2019, China had just 200 gigawatts of each. Bernstein says the country’s goal is a “monumental challenge” that could cost $5.5 trillion. The world’s most populous country emits more carbon dioxide than the U.S. and E.U. combined.

- Purchasing Manager’s Index (PMI) figures will be released next week, and the expectation is for China to continue to show signs of a strong recovery and lead the world in manufacturing. Expectations are for a manufacturing PMI reading of 54.9 – above the 50 level that separates growth from contraction.

Threats

- China’s Ministry of Commerce released provisions on its so-called “unreliable entity list”, or blacklist, which is similar to the U.S. Commerce Department’s entity list restricting named companies from accessing items originating in the U.S. “The coming debut of the (unreliable entity list) underscores the dilemma facing (multi-national corporations) in China, who are squeezed between the legal and political dictates of the U.S. and its Western allies on the one hand and Beijing on the other,” says Michael Hirson, practice head, China and Northeast Asia, at Eurasia Group.

- Analysts are predicting that should Biden beat Trump for the presidency in the upcoming U.S. election, he would be tougher on China than Trump. Biden has already promised to take a harder line on China’s crackdowns on ethnic minorities and Hong Kong. Chinese officials are estimating that whoever wins the election, China will likely still face a harsher political environment.

- Indian stocks fell by the most since May as foreign investors sold shares at the fastest pace in three weeks, reports Bloomberg. All but two stocks closed in the red on Thursday and the NSE Nifty 50 Index ended down 2.9 percent. Foreign investors sold a net $241 million worth of Indian stocks in the week through Thursday.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended September 25 was MoonSwap, up over 9,000 percent.

- As the price of bitcoin rises by $200 each month, the 200-week moving average has formed an implied price floor since the digital asset first appeared in 2009, writes CoinTelegraph. New data suggests that speculators waiting for a BTC price drop of even 35 percent might be waiting forever. On September 22, quant analyst PlanB noted that bitcoin will break the habit of a lifetime if it goes lower than $6,700, the article continues.

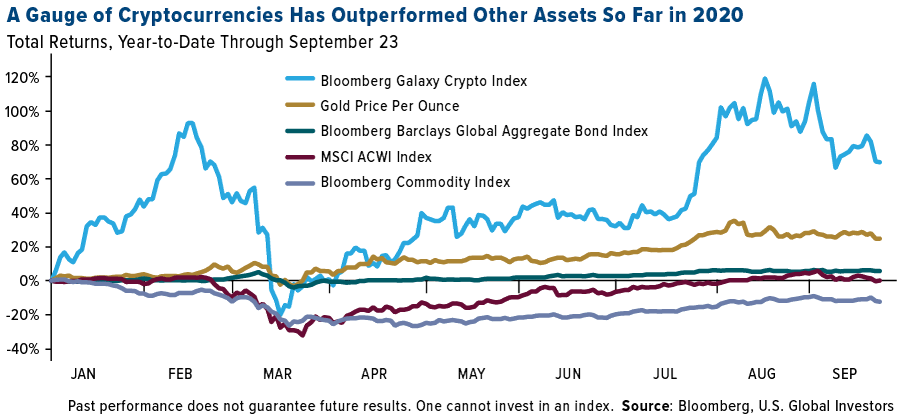

- So far this year, a gauge of cryptocurrencies has been the top performer of 2020 so far, substantially beating gold, global government bonds, global equities and commodities.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week ended September 18 was DeFi Bids, down 98.18 percent.

- A new report from the Bank of Canada suggests that bitcoin ownership is associated with a lack of financial literacy. For the second year in a row, the survey “found that awareness of bitcoin increased with financial literacy, but the likelihood of ownership declined as the level of financial literacy increased.” However, the findings could be explained by the fact that cryptocurrency awareness and ownership tend to be highest among young men who may not have as much investing experience under their belts.

- Russia’s Ministry of Finance is cracking down even further on crypto assets. The ministry this week amended its law on digital currencies, requiring crypto users to report their digital wallet address, transaction history and balance if the amount is over 100,000 Russian rubles, or about $1,295, in a single year. Failing to do so, the law states, could lead to a punishment of up to three years in prison. Russia has already banned crypto as a mode of payment.

Opportunities

- Announced Wednesday, the Chamber of Digital Commerce (a blockchain advocacy group) has appointed former acting White House chief of staff Mick Mulvaney to its board of advisors. CoinDesk also reports that Visa, Goldman Sachs and Six Digital Exchange have joined the group as executive committee members.

- Robert Alice, art historian-turned-blockchain artist, believes that the bitcoin codebase is a culturally and politically significant piece of 21st century history, writes Coin Telegraph. Christie’s will sell its first nonfungible token in an upcoming auction of what has been characterized as the “largest artwork” in the history of bitcoin.

- CEO of MicroStrategy Inc. Michael Saylor believes that the Federal Reserve’s recent relaxing of its inflation policy helped convince him to put the remainder of the enterprise-software maker’s cash into bitcoin, writes Bloomberg. “We feel pretty confident that bitcoin is less risky than holding cash, less risky than holding gold,” Saylor said in an interview.

Threats

- The U.S. Department of Justice has made one of the biggest drug busts in history, writes CoinDesk, with half a tonne of narcotics and millions of dollars in cash and cryptocurrencies taken from dealers using the dark web. Results of “Operation DisrupTor” were announced Tuesday – with over 170 arrests made worldwide, including over 500 kilograms of drugs seized worldwide along with $6.5 million in both cash and crypto.

- At the start of the week, bitcoin fell by 4.5 percent, writes CoinDesk, registering its biggest single-day decline since September 4. It appears that the biggest cryptocurrency is again taking cues from the stock markets with analysts warning that prices may fall below $10,000 if equities see a further sell-off.

- The Ethereum price remains at risk, according to NewsBTC, with a strengthening case for a correction below $300. The digital currency broke below key support of $330, and then $320. “If Ethereum fails to recover above the $330 and $335 resistance levels, there is a risk of more losses in the near term,” writes senior analyst Aayush Jindal.

Leaders and Laggards

| Index | Close | Weekly Change($) |

Weekly Change(%) |

|---|---|---|---|

| 10-Yr Treasury Bond | 0.66 | -0.03 | -4.93% |

| Oil Futures | 40.12 | -0.85 | -2.07% |

| Hang Seng Composite Index | 3,635.17 | -177.04 | -4.64% |

| S&P Basic Materials | 392.92 | -26.26 | -6.26% |

| Korean KOSPI Index | 2,278.79 | -127.38 | -5.29% |

| S&P Energy | 229.09 | -24.49 | -9.66% |

| Nasdaq | 10,913.56 | +3.28 | +0.03% |

| DJIA | 27,173.96 | -728.02 | -2.61% |

| Russell 2000 | 1,474.91 | -67.69 | -4.39% |

| S&P 500 | 3,298.46 | -58.55 | -1.74% |

| Gold Futures | 1,864.80 | -85.10 | -4.36% |

| XAU | 139.96 | -14.10 | -9.15% |

| S&P/TSX VENTURE COMP IDX | 695.26 | -47.96 | -6.45% |

| S&P/TSX Global Gold Index | 358.62 | -24.64 | -6.43% |

| Natural Gas Futures | 2.13 | +0.09 | +4.16% |

| Index | Close | Monthly Change($) |

Monthly Change(%) |

|---|---|---|---|

| Korean KOSPI Index | 2,278.79 | -90.53 | -3.82% |

| 10-Yr Treasury Bond | 0.66 | -0.03 | -4.79% |

| Gold Futures | 1,864.80 | -87.70 | -4.49% |

| S&P Basic Materials | 392.92 | -5.31 | -1.33% |

| S&P 500 | 3,298.46 | -180.27 | -5.18% |

| DJIA | 27,173.96 | -1,157.96 | -4.09% |

| Nasdaq | 10,913.56 | -751.50 | -6.44% |

| Oil Futures | 40.12 | -3.27 | -7.54% |

| Hang Seng Composite Index | 3,635.17 | -289.34 | -7.37% |

| S&P/TSX Global Gold Index | 358.62 | -21.45 | -5.64% |

| XAU | 139.96 | -10.54 | -7.00% |

| Russell 2000 | 1,474.91 | -85.29 | -5.47% |

| S&P Energy | 229.09 | -37.76 | -14.15% |

| S&P/TSX VENTURE COMP IDX | 695.26 | -34.61 | -4.74% |

| Natural Gas Futures | 2.13 | -0.33 | -13.57% |

| Index | Close | Quarterly Change($) |

Quarterly Change(%) |

|---|---|---|---|

| XAU | 139.96 | +17.69 | +14.47% |

| S&P/TSX Global Gold Index | 358.62 | +27.14 | +8.19% |

| Gold Futures | 1,864.80 | +76.40 | +4.27% |

| DJIA | 27,173.96 | +1,428.36 | +5.55% |

| S&P 500 | 3,298.46 | +214.70 | +6.96% |

| Nasdaq | 10,913.56 | +896.56 | +8.95% |

| Korean KOSPI Index | 2,278.79 | +166.42 | +7.88% |

| Natural Gas Futures | 2.13 | +0.65 | +43.52% |

| S&P Basic Materials | 392.92 | +44.82 | +12.88% |

| Russell 2000 | 1,474.91 | +61.59 | +4.36% |

| Oil Futures | 40.12 | +1.40 | +3.62% |

| Hang Seng Composite Index | 3,635.17 | +11.94 | +0.33% |

| S&P/TSX VENTURE COMP IDX | 695.26 | +99.30 | +16.66% |

| S&P Energy | 229.09 | -58.30 | -20.29% |

| 10-Yr Treasury Bond | 0.66 | -0.03 | -4.37% |

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission ("SEC"). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (06/30/2020):

OTP Bank

Tesla Inc.

Wheaton Precious Metals Corp.

Maverix Metals Inc.

OceanaGold Corp.

Barrick Gold Corp.

Newmont Corp

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment. The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index. The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges. The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

There is no guarantee that the issuers of any securities will declare dividends in the future or that, if declared, will remain at current levels or increase over time. Bloomberg Galaxy Crypto Index (BGCI) is designed to measure the performance of the largest cryptocurrencies traded in USD. The Bloomberg Barclays Global Aggregate Index is a flagship measure of global investment grade debt from twenty-four local currency markets. This multi-currency benchmark includes treasury, government-related, corporate and securitized fixed-rate bonds from both developed and emerging markets issuers. The MSCI ACWI Index is a free-float weighted equity index. It includes both emerging and developed world markets. Bloomberg Commodity Index (BCOM) is calculated on an excess return basis and reflects commodity futures price movements. The index rebalances annually weighted 2/3 by trading volume and 1/3 by world production and weight-caps are applied at the commodity, sector and group level for diversification. The Bloomberg Dollar Spot Index (BBDXY) tracks the performance of a basket of 10 leading global currencies versus the U.S. Dollar. The MSCI Indonesia Index is designed to measure the performance of the large and mid-cap segments of the Indonesian market. The NIFTY 50 is a benchmark Indian stock market index that represents the weighted average of 50 of the largest Indian companies listed on the National Stock Exchange. The relative strength index (RSI) is a momentum indicator used in technical analysis that measures the magnitude of recent price changes to evaluate overbought or oversold conditions in the price of a stock or other asset. Standard deviation is a measure of the dispersion of a set of data from its mean. The more spread apart the data, the higher the deviation. Standard deviation is also known as historical volatility. The cash flow growth rate for a stock is a measure of how the stock’s cash flow per share (CFPS) has grown over the last three to five years. Gross margin is a company’s net sales revenue minus its cost of goods sold (COGS). In other words, it is the sales revenue a company retains after incurring the direct costs associated with producing the goods it sells, and the services it provides.