Europe’s Strict Emission Standards Drive Palladium Past Gold

Date Posted: January 18, 2019

Read time: 49 min

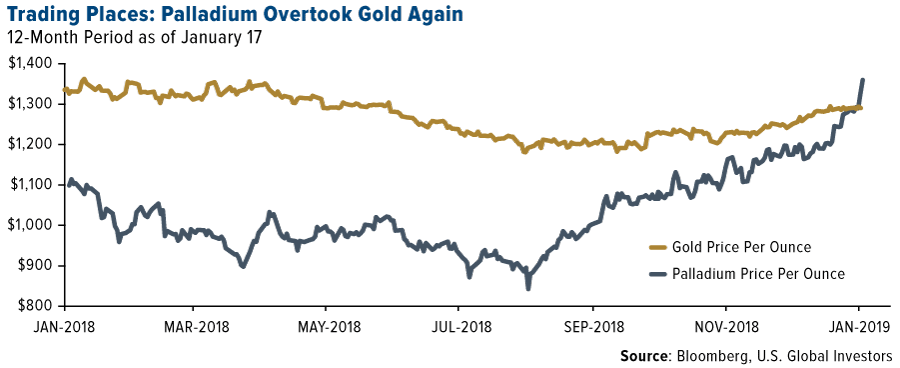

Palladium might not fill headlines the way gold does, but it's been on fire lately. Not only has the precious metal been the best performing commodity for two years straight, but its price also just shot past gold for the first time since 2001.

By Frank Holmes

CEO and Chief Investment Officer

U.S. Global Investors

Palladium might not fill headlines the way gold does, but it’s been on fire lately. Not only has the precious metal been the best performing commodity for two years straight, but its price also just shot past gold for the first time since 2001. For the first time ever, it broke through $1,400 an ounce this week before pulling back somewhat. From its 52-week low set in August, palladium has climbed almost 70 percent. It’s added about 16 percent in the past 30 trading days alone.

Supply is tight, but like many other things, we largely have government policy to thank for the palladium rally. In this case, I’m talking specifically about governments in Europe, which have recently strengthened their vehicle emission standards. The “Euro standard,” as it’s called, classifies vehicles on a scale from one to six, with one being the most polluting and six being the least polluting.

Some European cities have already banned the dirtiest “Euro 1” vehicles from their streets. Old diesel cars and trucks were outlawed in Brussels effective January 2018. In May 2018, Hamburg became the first German city to do the same.

Diesel Engines in the Crosshairs

But now that it’s a new year, some city governments are escalating the ban to include Euro 2 automobiles that run on diesel. Next month, Frankfurt—Germany’s financial hub—will go as far as to ban all Euro 4-and-worse diesel vehicles, and all Euro 1 and 2 gasoline-burning vehicles.

I believe this escalation was prompted in part by a comment made by Elzbieta Bienkowska, a European commissioner whose responsibilities include oversight of industry and entrepreneurship. Speaking to Bloomberg in May, she said that “diesel cars are finished.”

|

|

And then, as if to hasten Bienkowska’s prediction, a damning study on diesel engines was issued in June by the very same group that blew the whistle on Volkswagen’s emissions scandal back in 2015. According to the study, conducted by the International Council on Clean Transportation (ICCT), even the newest, cleanest diesel vehicles failed to meet Europe’s strict emission standards in “real world” driving conditions. Peter Mock, the ICCT’s managing director, defended the report, saying that “pretty much all Euro 6 diesels on the market are not clean.”

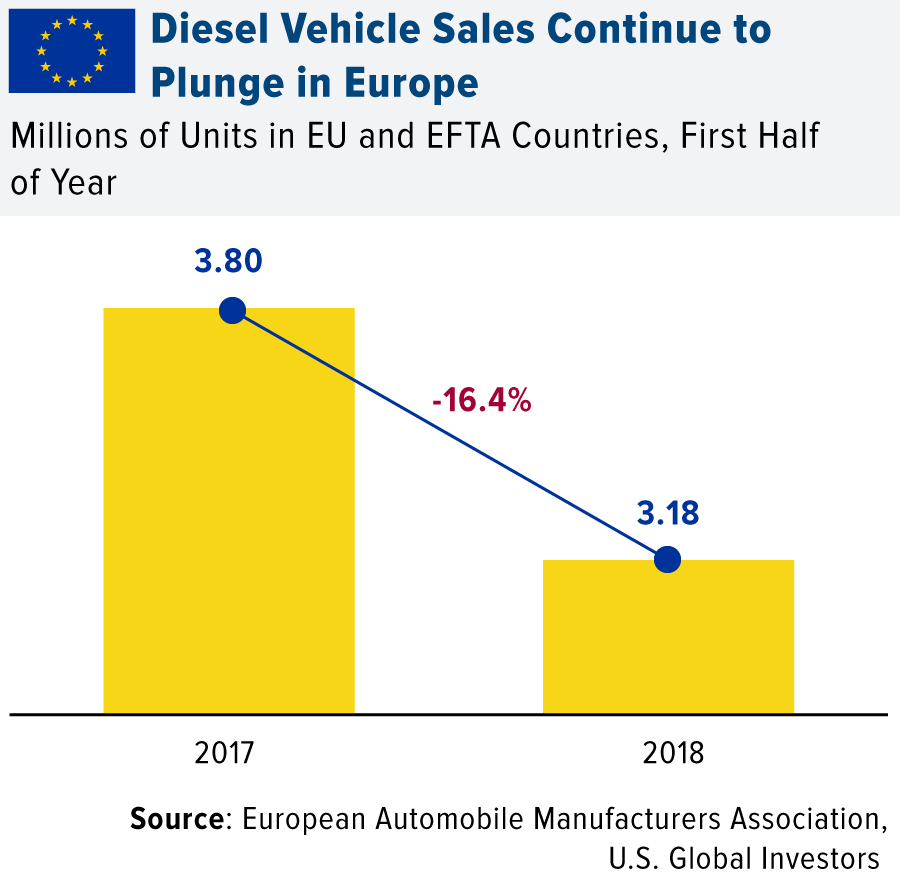

European sentiment of diesel was already in freefall, but momentum is increasing. In the first half of 2018, sales of diesel vehicles within the European Union (EU) and European Free Trade Association (EFTA) fell more than 16 percent compared to the same period in 2017. For all of 2018, British sales of diesels were down nearly 30 percent, according to the Society of Motor Manufacturers and Traders (SMMT). Between 2016 to 2018, diesel’s share of new vehicle sales in the EU plunged dramatically, from nearly half of all sales to just under a third.

Palladium Has Been the Beneficiary

So what does all of this have to do with palladium? The metal, as you probably know, is used in the production of catalytic converters, which “scrub” pollutants from the exhaust of internal combustion engines. And because of Europe’s enforcement of strict new standards, demand for these devices is surging, along with palladium itself.

Demand is so high, in fact, that there are now reports, in the U.K. and U.S., of thieves stealing catalytic converters, sometimes in broad daylight, to extract the precious metal. On Thursday, it traded as high as $1,434.50, according to CNBC.

Supply Worries Have Remained High

There’s more to the story of palladium’s bull run. For the past several years, supply has been in deficit. That’s mostly because around 80 percent of all palladium (and platinum) production is concentrated in two countries—South Africa and Russia. The geopolitical risks are high. When South African laborers went on strike in 2014, all production of the platinum metals, including palladium, grinded to a halt.

Besides supply issues, the biggest risk facing palladium right now is substitution risk. With palladium trading above $1,400 an ounce, how long will it be before auto manufacturers switch to its sister metal, platinum, which is currently trading at around $800 an ounce?

In the meantime, there could be money to be made.

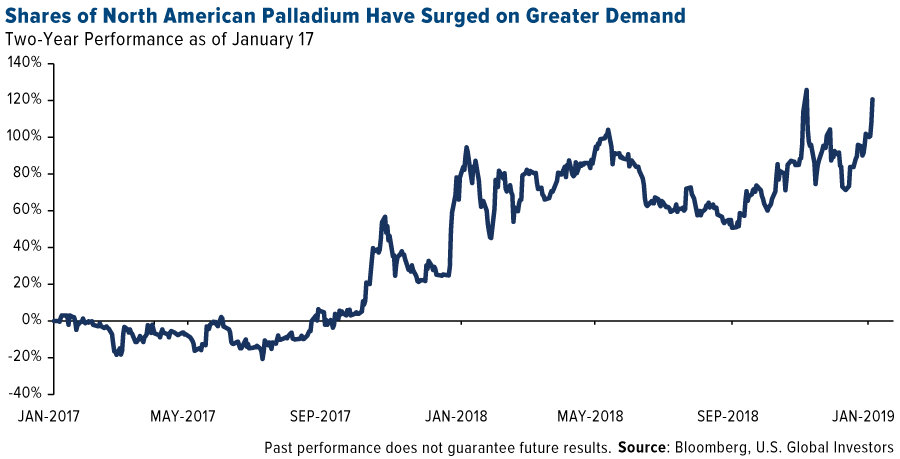

A Palladium Miner With Incredible 87 Percent Income Growth

One of our favorite ways to play the rally is North American Palladium. The company, headquartered in Toronto, mines both palladium and gold (and other metals as a byproduct), and has seen quite a rally itself on higher metal prices. For the 24-month period, its shares are up a remarkable 120 percent.

North American Palladium had a phenomenal third quarter in 2018. According to results, income after taxes and expenses was $22.9 million, up a whopping 87.7 percent from $12.2 million during the same period the previous year. That translated to earnings per share (EPS) of $0.39, up from $0.21 in 2017. I’m eagerly awaiting the company’s results for the fourth quarter!

Gold Market

This week spot gold closed at $1,281.75, down $5.75 per ounce, or 0.45 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 3.24 percent. The S&P/TSX Venture Index came in off 1.04 percent. The U.S. Trade-Weighted Dollar gained 0.72 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Jan-15 | PPI Final Demand YoY | 2.5% | 2.5% | 2.5% |

| Jan-16 | Germany CPI YoY | 1.7% | 1.7% | 1.7% |

| Jan-17 | Eurozone CPI Core YoY | 1.0% | 1.0% | 1.0% |

| Jan-17 | Initial Jobless Claims | 220k | 213k | 216k |

| Jan-20 | China Retail Sales YoY | 8.1% | — | 8.1% |

| Jan-22 | Germany ZEW Survey Current Situation | 43.3 | — | 45.3 |

| Jan-22 | Germany ZEW Survey Expectations | -18.5 | — | -17.5 |

| Jan-23-Feb-1 | New Home Sales | 567k | — | 544k |

| Jan-23-Feb-1 | Durable Goods Orders | 0.8% | — | 0.8% |

| Jan-23-Feb-1 | Housing Starts | 1253k | — | 1256k |

| Jan-24 | ECB Main Refinancing Rate | 0.000% | — | 0.000% |

| Jan-24 | Initial Jobless Claims | 215k | — | 213k |

| Jan-25 | Durable Goods Orders | 1.5% | — | — |

| Jan-25 | New Home Sales | 554k | — | — |

Strengths

- The best performing metal this week was palladium, up 4.36 percent on acute supply tightness. JPMorgan sees additional upside to the price despite weaker auto sales. Gold traders and analysts surveyed by Bloomberg remain bullish on the yellow metal for a 10th straight week even as prices remain near the $1,300 level. ETFs added gold to their holdings for the 15th straight day. So far this year, according to Bloomberg data, ETF net purchases totaled 917,554 ounces. Turkey continues to stock up on gold with its reserves rising $123 million from the previous week. Russia is also boosting its reserves of gold. Central bank data shows that Russia’s gold reserves rose to $468.5 billion in December, up from $462.1 billion in November. This week’s further Brexit turmoil has sparked gold demand in the U.K. as a safe haven asset.

- Bloomberg reports that Waterton Global Resource Management, which owns 12 percent of Hudbay Minerals, is seeking to oust Hudbay’s CEO and most of the board. The company’s shares have fallen more than 40 percent in the past year and Waterton began agitating for changes since last year. Waterton CEO Isser Elishis said that “the company’s board must evolve in order to meaningfully hold management to account.” Shareholder activism such as this is positive for the metals sector and could help spark better performance from companies.

- Just three months after Barrick Gold moved to buy Randgold Resources, another mega gold miner deal was announced this week. Newmont Mining is buying rival Goldcorp in a $10 billion deal that will create the world’s largest gold miner. Newmont will pay 0.3280 of its own shares for each Goldcorp share, representing a premium of 17 percent, reports Bloomberg. Goldcorp shares climbed 11 percent on Monday when the deal was announced.

Weaknesses

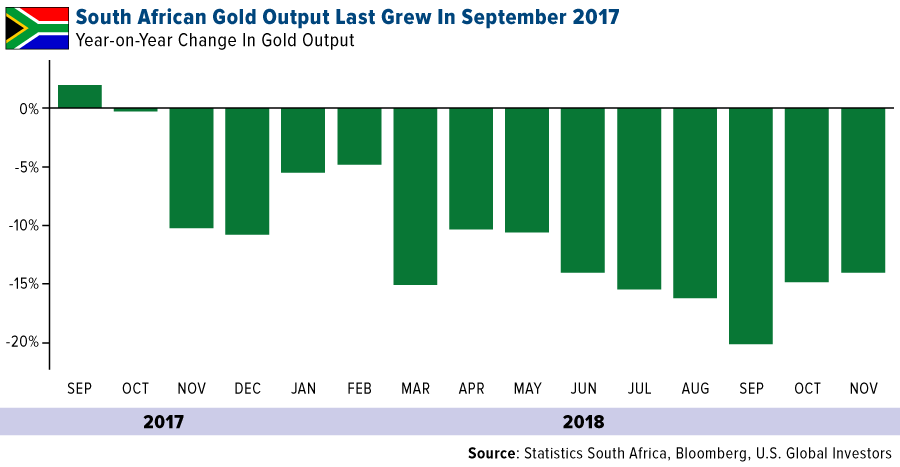

- The worst performing metal this week was silver, down 1.63 percent. Gold is experiencing its slowest start to a year in six years, trading within the narrow range of $1,280 to $1,300 an ounce, despite January historically being a strong month for the yellow metal. South Africa, once the world’s top producer, has seen gold production fall since September 2017 and is down 14 percent from a year earlier. Bloomberg’s Prinesha Naidoo writes that most of South Africa’s gold mines are unprofitable at current gold prices.

- Kirk Woodman, vice president of exploration at Vancouver-based Progress Minerals, was found dead with bullet holes in his body in Burkina Faso yesterday after being reported as abducted earlier in the week. Officials of the West African nation have said that no group has taken responsibility for the murder so far.

- As mentioned above, the Newmont-Goldcorp merger is likely positive for the gold industry, and is even more positive for Goldcorp CEO David Garofalo, who could exit the deal with $6.9 million to $11 million in his pocket. Garofalo has overseen shares of Goldcorp fall more than a quarter in the last 12 months and highlights the fact that some gold executives are overpaid even as the companies they run underperform. The Shareholders’ Gold Council said in a statement that “the merger with Newmont is only a victory for shareholders in as much as it eliminates another gold company with executive incentives that are grossly misaligned with those of shareholders.”

Opportunities

- Billionaire and founder of Equity Group Investments Sam Zell said in a Bloomberg interview this week that he has bought gold for the first time in his life “because it is a good hedge.” Zell continued to say that “supply is shrinking and that is going to have a positive impact on the price.” Another bullish recommendation on gold this week comes from Cornerstone Marco. The investment shop writes that gold could be set up for a breakout above the well-defined annual tops of the last five years. Analysts write that gold is a bona fide investment vehicle because it has “matched the performance of the S&P 500 with dividends reinvested over a 20-year basis” and that gold’s performance is “not too shabby.”

- Jewelers in China, the world’s number one consumer of gold, are struggling to appeal to the younger generation of consumers because they don’t view gold jewelry as an investment, as some of the older generations did. However, to combat these changes, jewelers are opting for more unique designs rather than focusing solely on quality. For example, new gold jewelry player Mene is partnering with world-renowned fashion photographers Inez & Vinoodh to create a special collection of investment-grade jewelry. Some older, more traditional jewelers who have not kept up with changing trends could see shares fall on weaker sales. For example, Signet Jewelers fell 25 percent on Thursday and was downgraded to a sell from neutral after the company reduced financial targets on disappointing holiday results, reports Bloomberg.

- With now two monster gold miner deals—Barrick-Randgold and Newmont-Goldcorp—there could be more smaller acquisitions on the way. Newmont and Goldcorp are both expected to unload some of their unloved assets, which could leave room for other gold companies to make some deals. UBS Group AG analysts, including Daniel Morgan, write that Australian gold producers, such as Evolution Mining and Northern Star Resources, are best placed to acquire assets that could be sold amid the two above-mentioned mergers. Northern Star Resources executive chairman Bill Beament said in an interview this week that deals won’t come cheap. Beament says that the gold sector isn’t under pressure and that “the majors aren’t forced sellers.” Some warn that mega-mergers aren’t necessarily positive for shareholders. Jake Klein, executive chairman of Evolution Mining, told Bloomberg that the thesis of bigger being better “hasn’t proven to be value creating for shareholders” historically in the gold sector. Mid-sized and small producers such as Evolution Mining and Wesdome Gold Mines have actually outperformed larger competitors over the past six years.

Threats

- The Financial Times reported that there was large-scale fraud in elections in the Democratic Republic of Congo. This could be negative for certain companies who own mines in the country. Due to the recent mega gold miner mergers, the S&P TSX Global Gold Index will now become a combined 38.8 percent weighted in just two names, Barrick and Newmont, which makes the index and portfolios tracking the index less diversified. Some investors worry that Canada is losing its status and influence in the global mining industry, as evidenced by the takeovers of Canadian-based Barrick and then Goldcorp. For example, with the Newmont-Goldcorp merger, offices will more than likely be consolidated to Newmont’s in Colorado, removing Goldcorp’s Vancouver presence.

- Russia is discovering that the push to accelerate “de-dollarization” is harder than it initially thought. Bloomberg writes that Russia’s central bank dumped $101 billion in 2018 of U.S. currency amid fears of additional sanctions. Shifting to another currency, such as the ruble or yuan, equals higher costs and difficulties in finding banks to handle business, according to Russian state-owned company executives. Many commodity benchmarks, such as oil, are set in the U.S. dollar, which makes it complicated to move away from.

- Credit Suisse strategists warn investors not to get overly optimistic about the global stock market rally and warn that it’s best to take profit instead of building positions. Bloomberg writes that the strategists say investment-grade spreads, which have been closely correlated with the S&P 500, are at “danger” levels. Wells Fargo wrote this week that it would turn negative on gold if it breaks the $1,350 an ounce level. The bank warned investors to “resist the urge to jump on the gold bandwagon if this rally continues” because they view the gold rally as a sprint, rather than a marathon, and say it won’t last.

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 2.96 percent. The S&P 500 Stock Index rose 2.87 percent, while the Nasdaq Composite climbed 2.66 percent. The Russell 2000 small capitalization index gained 2.43 percent this week.

- The Hang Seng Composite gained 1.59 percent this week; while Taiwan was also up 0.79 percent and the KOSPI rose 2.35 percent.

- The 10-year Treasury bond yield rose 8 basis points to 2.785 percent.

Domestic Equity Market

Strengths

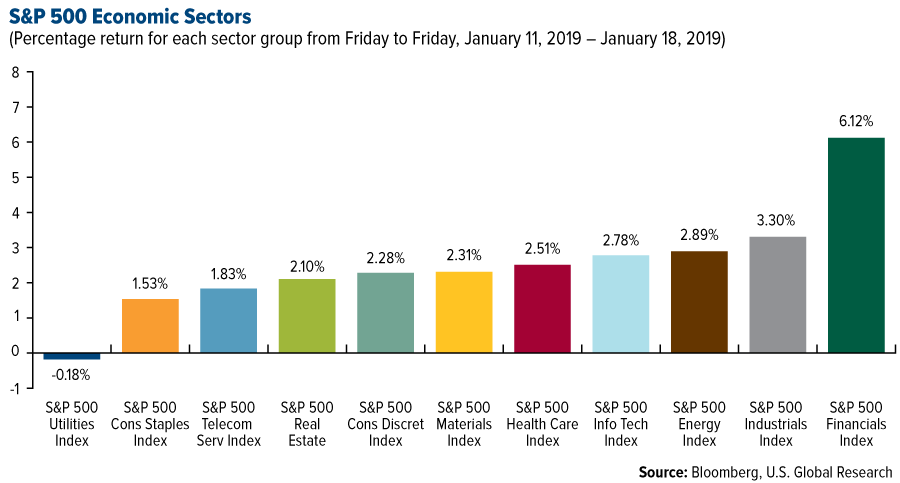

- Financials was the best performing sector of the week, increasing 6.12 percent compared to an overall increase of 2.68 percent for the S&P 500 Index.

- VF Corporation was the best performing stock for the week, increasing 15.14 percent.

- Digital First Media made an offer for Gannett this week. The $1.4 billion bid equates to $12 a share, a 23 percent premium to Friday’s closing price.

Weaknesses

- Utilities was the worst performing sector for the week, decreasing 0.18 percent compared to an overall increase of 2.68 percent for the S&P 500.

- Newmont Mining was the worst performing stock for the week, falling 8.94 percent.

- Geisha Williams stepped down as CEO of Pacific Gas & Electric (PG&E), as the company is reportedly preparing for bankruptcy later this month amid the fallout from the state’s wildfires.

Opportunities

- Workplace chat service Slack is planning to go public through a direct listing rather than an initial public offering (IPO). Spotify made waves when it chose to bypass a traditional offering in pursuit of a direct listing.

- According to JPMorgan, value stocks are set to explode higher as the market recovers from the plunge in December.

- Verizon is quietly testing its own cloud gaming service, according to The Verge. The company has been quietly recruiting gamers to test Verizon Gaming, which will eventually make its way to Android phones.

Threats

- Facebook’s business model is under scrutiny in Germany, where a local regulator will reportedly order the social network to stop collecting certa in user data. German authorities don’t like the way Facebook collects information about people via WhatsApp, Instagram and third-party sites.

- The impact of the U.S.-China trade war on corporate earnings will be in focus now that earnings season has gotten underway. Many companies have been vocal about the trade war impacting their business.

- Snap’s stock plummeted after the company confirmed it was losing its chief financial officer (CFO). In an SEC filing, the company said that Tim Stone was walking away after just eight months on the job.

The Economy and Bond Market

Strengths

- Filings for unemployment benefits fell to an unexpected five-week low, even amid the shutdown. Initial jobless claims declined by 3,000 to 213,000 last week.

- The Philadelphia Fed Business outlook for January surprisingly advanced to 17.0, up from 9.4 in December. The data is an encouraging sign that the recent surge in political uncertainty has weighed less on business sentiment than previously estimated.

- Sentiment among U.S. homebuilders rose for the first time in three months amid a decline in borrowing costs, which is a sign that housing may stabilize in the year ahead even as the industry remains in a broad slowdown. The National Association of Home Builders/Wells Fargo Housing Market Index increased to 58 in January, up from a three-year low of 56 in December.

Weaknesses

- The Empire State manufacturing index fell 7.6 points to 3.9 in January, the lowest reading in more than a year, the New York Federal Reserve said Tuesday. Economists had expected the index to inch up to 12. The index has fallen a cumulative 18 points since November. The new-orders index and shipments gauges show performance in these areas has moved at a slower pace in January. The new-orders index fell 9.9 points to 3.5, and the shipments index fell 2.4 points to 17.9. Unfilled orders and inventory indexes also fell. Firms were less optimistic about the six-month outlook.

- China’s 2018 trade surplus with the world fell to $351.76 billion, the lowest since 2013, according to data released Monday by China’s General Administration of Customs. China’s trade surplus with the U.S., however, swelled to a record $323.32 billion.

- Europe is in an economic slump. Eurostat data released Monday showed that industrial production throughout the eurozone fell 1.7 percent from October to November 2018.

Opportunities

- The Leading Index for December will be released next Thursday. Any indications of positive economic momentum would assuage investor fears about a growth slowdown.

- New home sales data will be released next Friday. The forecast for a pickup to 567k from the previous 544k would be a welcome sign for the weakening housing market.

- According to Evercore ISI, UK Prime Minister May’s Brexit deal defeat in parliament this week means more uncertainty in the near-term. However, the defeat increases the likelihood of a softer Brexit or no Brexit in the long-term, which is positive for markets.

Threats

- Momentum is easing across the world’s major economies, according to a gauge the OECD uses to predict turning points. The Composite Leading Indicator is the latest sign of a synchronized slowdown in global growth, adding to recession warnings sparked by industrial figures in Germany last week and slumping trade figures for China earlier this week. The indicator, which is designed to anticipate turning points six-to-nine months ahead, has been ticking down since the start of 2018 and fell again in November. The OECD singled out the U.S. and Germany, where it said “tentative signs” of easing momentum are now confirmed. Just two weeks into 2019, the OECD economic indicator follows a run of data that mean growth this year could be even slower than currently anticipated. For Bloomberg economists, the data points to a “slowdown, not meltdown,” but they still say the loss of momentum is “striking.”

- The U.S. government shutdown is now the longest on record. Bank of America Merrill Lynch says, "Every two weeks of a shutdown trims 0.1 percentage points from growth; additional drag is likely due to delays in spending and investment."

- The bond market is flashing a scary parallel to the financial crisis. Weakening demand at U.S. Treasury auctions is the latest worry that investors need to pay attention to.

Energy and Natural Resources Market

Strengths

- Lumber was the best performing major commodity this week rising 7.76 percent. The commodity rose to a seven-week high after West Fraser Timber announced production cuts at three British Columbia sawmills.

- The best performing sector this week was the S&P 1500 Oil & Gas Services and Equipment Index. The index rose 5.72 percent after index heavyweight Schlumberger NV said it would lower capital expenditures but still forecasted healthy growth, sending its shares higher.

- The best performing stock for the week was Mercer International Inc. The Canadian pulp and paper producer rose 28.28 percent after the company was added to the S&P Smallcap 600 Index, resulting in large-volume buying action from passive funds tracking the index.

Weaknesses

- Iron ore was the worst performing commodity this week. The commodity dropped 5.67 percent after India announced it is considering raising import duties on iron ore.

- The worst performing sector this week was the NYSE Arca Gold Miners Index. The index dropped 3.31 percent after gold prices declined amid optimism for progress in U.S.-China trade talks that boosted equities.

- The worst performing stock for the week was Newmont Mining Corp. The largest gold mining company in the U.S. dropped 9.02 percent after the company announced a $10 billion share deal to acquire Canadian rival Goldcorp Inc.

Opportunities

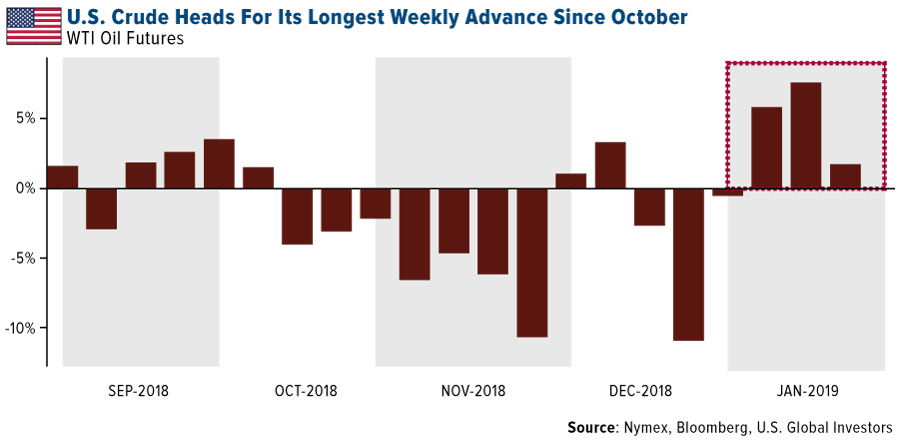

- Oil headed for a third weekly increase on expectations that production cuts by OPEC and resilient fuel demand will keep global markets in balance. In addition, global oil demand remains on course to be stronger this year than in 2018 as a boost from lower fuel prices counters slowing economic activity, according to the International Energy Agency.

- Billionaire Sam Zell said he is buying gold for the first time in a bet on tight supply. “The amount of capital being put into new gold mines is a most nonexistent,” Zell said. “All of the money is being used to buy up rivals.” The combined gold reserves still buried in mines — an indicator of production prospects — shrank by more than 40 percent in 2017.

- Chinese officials pledged tax cuts on a “larger scale.” JPMorgan estimated the impact may be a fiscal boost of around half a percentage point. On the data front, credit growth exceeded expectations last month in a sign efforts to spur lending are having an effect.

Threats

- Latest trade data from China showed imports fell 7.6 percent year-on-year in December when analysts had predicted a 5 percent rise. Exports unexpectedly dropped 4.4 percent, confounding expectations for a 3 percent gain.

- Home sales in the U.S. slumped almost 11 percent in December, the biggest decline for any month since 2016, according to real estate brokerage Redfin. Prices inched up 1.2 percent to a median of $289,800, marking the smallest annual increase since the end of the last housing crash in 2012.

- Economists are becoming more bearish on iron ore. After a series of warnings about potential losses from top banks Morgan Stanley and Goldman Sachs, Capital Economics has chimed in with a forecast for a drop back to $55 per ton by the end of the year.

Emerging Europe

Strengths

- Turkey was the best performing country this week, gaining 7.4 percent. Turkish equites responded positively to improving global conditions and a dovish Fed. Additionally, the central bank’s decision to keep rates unchanged might have offered additional confidence to investors.

- The Turkish lira was the best relative performing currency this week, gaining 2.6 percent against the U.S. dollar. The central bank left its main rate unchanged at 24 percent, while some investors might have speculated the rate would be cut due to declining inflation.

- Consumer staples was the best performing sector among eastern European markets this week.

Weaknesses

- Greece was the worst performing country this week, losing 2.9 percent. Banks were the biggest laggards. The European Central Bank (ECB) may require banks to provision 100 percent of all new and old non-performing loans until 2026. Greek banks still carry a high level of non-performing loan on their books, about 75 percent.

- The Czech koruna was the worst performing currency this week, losing 1 percent against the U.S. dollar. The koruna erased gains from the prior week, but the central bank should continue to hike rates, and such monetary policy should support the currency. This week final third quarter GDP was released and the Czech economy is growing at 2.4 percent annually, which is a much slower rate than neighboring Poland or Hungary.

- Utilities was the worst performing sector among eastern European markets this week.

Opportunities

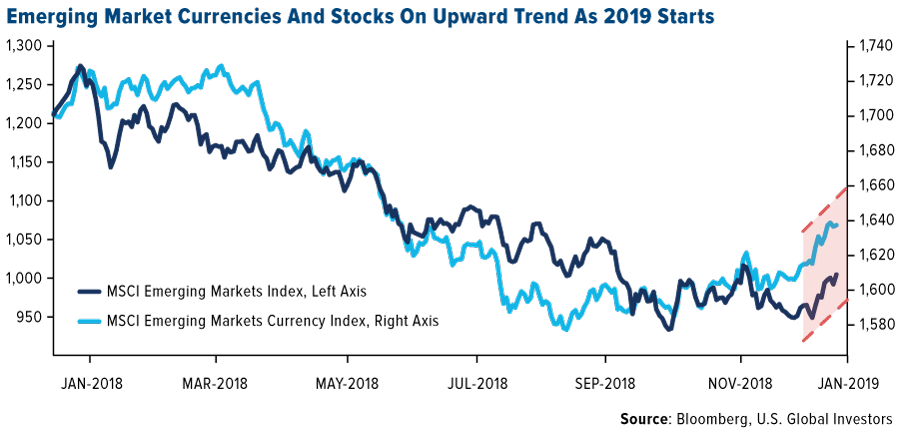

- A rally in emerging market assets should continue until the likely conclusion of a U.S.-China trade deal by the end of February caps the current gains, according to Bank of America Corp. In the short-term, the bank maintains a risk-on stance, except for Mexico and Turkey. Bank of America prefers to invest in Ukraine, Russia, South Africa, Brazil, Argentina and Asian currencies.

- On December 19 of last year, the U.S. Treasury Department announced that sanctions imposed on three companies linked to Russian oligarch Oleg Deripaska would expire within 30 days unless Congress voted against it. The deadline for the end of the sanctions was extended, but if sanctions are lifted, Russian equites may outperform and aluminum prices may fall.

- Reuters reported that Germany and China signed agreements on Friday to strengthen coordination in banking, finance and capital markets, and pledged to further open market access and deepen cooperation to broaden economic ties. The agreements were reached after a two-day visit to Beijing by German Finance Minister Scholz for talks with Vice Premier Liu He. Both sides reaffirmed that they will strengthen macroeconomic policy coordination and pragmatic cooperation in the fiscal and financial fields and expand strategic cooperation.

Threats

- Members of the parliament in the United Kingdom voted against Theresa May’s proposed Brexit deal, but her government survived vote of confidence, suggesting that most party members still have confidence in May’s leadership. For now, the U.K. avoided early elections, but the Brexit crisis remains. The probability of extending the Brexit date or holding a new referendum vote has increased. The British pound and equites will most likely remain volatile.

- Economic growth in Russia may not pick up in 2019. RenCap analysts published a report saying that 2019 looks like a more challenging year for Russia than 2018 was, with just 1.2 percent GDP growth (at $65 per barrel oil prices), cooling consumer and investment activity, higher inflation and rate hikes. Moreover, the threat of potential sanctions on newly issued state debt still exists.

- The mayor of the Polish city of Gdansk died on Monday after being stabbed during a charity event. The attacker, who was recently released from prison, screamed that he was “unfairly” imprisoned and “tortured” by the government. Political tension may rise.

China Region

Strengths

- Korea’s KOSPI jumped 2.35 percent for the week. Hong Kong, Shanghai and the Philippines all gained more than 1.6 percent for the week.

- Consumer goods was the top performing sector in the Hang Seng Composite Index for the week, climbing 3.69 percent. All sectors finished in the green for the week.

- The Thai baht pushed as low as 31.57 this week, leading performers in the region’s currencies.

Weaknesses

- Singapore’s non-oil domestic exports fell by 8.5 percent for the December year-over-year period, far short of an expected growth rate of 2.0 percent, and down from the prior and revised reading of -2.8 percent.

- China’s exports and imports missed, too. Year-over-year exports dropped 4.4 percent, well below the expected growth of 2.0 percent, while imports declined 7.6 percent, missing an anticipated 4.5 percent growth rate.

- Keeping up the theme of the week here, exports also missed in Indonesia, clocking in for the December period at a rate of a 4.62 percent decline year-over-year, short of surveyed expectations for a gain of 1.03 percent. Imports missed as well, showing a gain of 1.16 percent, well shy of expectations for a 7.72 percent gain.

Opportunities

- Late in U.S. trading on Friday, the story emerged among the media that in the early January round of trade talks, Beijing reportedly discussed the idea of a buying spree over the next six years aimed at reducing the trade imbalance with the United States to $0 by the end of 2024. (Hmm. Now, can anyone think of why2024 would be a possible target date?) While at face value a positive, clearly trade negotiations did not wrap up and the trade war is not yet concluded, so obviously the devil will be in the details and perhaps the real story is as much about—likely more about, in fact—what we don’tyet know. But importantly, there are apparently substantive conversations being had with real and significant amounts discussed in concrete timeframes, which is a positive. And it remains official that China’s Vice Premier Liu He will come to Washington for further talks at the end of this month.

- The internationalization of the renminbi and the broadening and opening of Chinese markets continues apace, with Chinese officials indicating that the opening of financial markets will proceed regardless of the outcome of the trade war with the United States. Most recently, China announced that authorities will double the foreign investment limit to $300 billion in the country’s latest move to continue to internationalize its system.

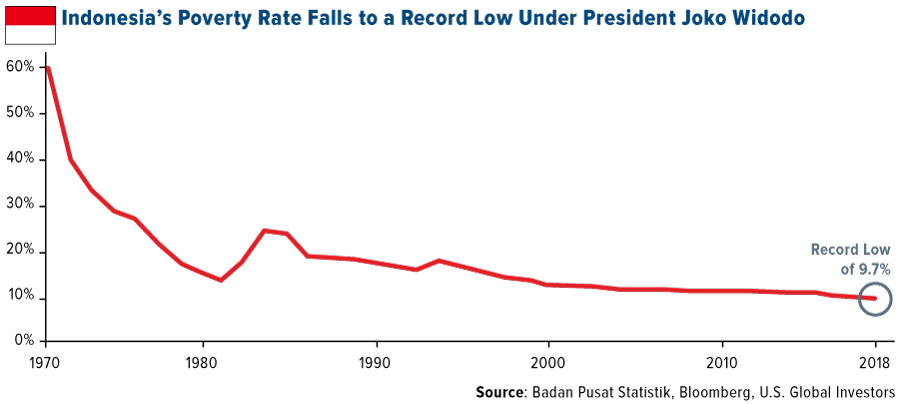

- Sure, it may be a bit of election fodder for debates and talking points in the upcoming Indonesian elections, but nonetheless it remains noteworthy that despite more recent attention to the high levels of dollar-denominated debt and the troubles the rupiah’s had over the last Fed rate hike cycle, the massive and growing Indonesian economy continues to expand as Southeast Asia’s most populous nation keeps chugging along economically. In honor of this fact we award you this humble chart, free of charge, as some food for thought.

Threats

- The trade war between China and the U.S. remains as an obvious headline threat to sentiment toward markets in the region and frankly, for overall global growth. While there may be positive recent developments, as that esteemed philosopher Yogi Berra famously quipped, “It ain’t over till it’s over.”

- It remains a positive that the U.S. continues its talks with North Korea, and while top North Korean aide Kim Yong Chol did arrive in the U.S. for talks late this week, and media reports late on Friday suggest that another Trump-Kim summit has now been penciled into the schedule for some time at the end of February, the stakes may also be rising as more reports indicate North Korea does not appear to be taking any substantial steps forward in the process, and undoubtedly North Korea will have serious demands, and, one suspects, a longer-term game plan and approach as well. (Of course, so will the United States.) But at the end of the day, as more time passes without a lot of demonstrable progress or any concrete plan, statements of “process” may only go so far in stemming disappointment from lack of progress. Talk is good; progress is better; let’s leave it at that. Thus, North Korea remains something of a wildcard as we come closer to a second summit.

- Federal prosecutors this week in the U.S. announced the intent to pursue a criminal probe against Huawei for allegedly stealing trade secrets, which may further exacerbate tensions between China and the U.S. Huawei CFO Meng Wanzhou remains under close watch by Canadian authorities in Vancouver, where she is out on bail, but awaiting a formal U.S. extradition request.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended January 18 was UpToken, up 176.78 percent.

- The world’s largest cryptocurrency exchange by adjusted trading volume, Binance, has launched a fiat currency-to-cryptocurrency exchange on the island of Jersey, a British self-governing dependency, writes CoinDesk. The new exchange targets Europe and will allow traders to trade bitcoin and Ethereum against the British pound and euro, according to Binance.

- Bitwage, a service offering companies the ability to pay workers in digital assets or cryptocurrencies, announced a partnership this week with Simple Efficient HR, a professional employer organization based in Texas. Bitwage CEO Jonathan Chester says that the partnership will help expand its services and allow more U.S. employers fund payroll, payroll taxes and benefits with bitcoin or ether, reports CoinDesk.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week ended January 18 was empowr coin, down 83.82 percent.

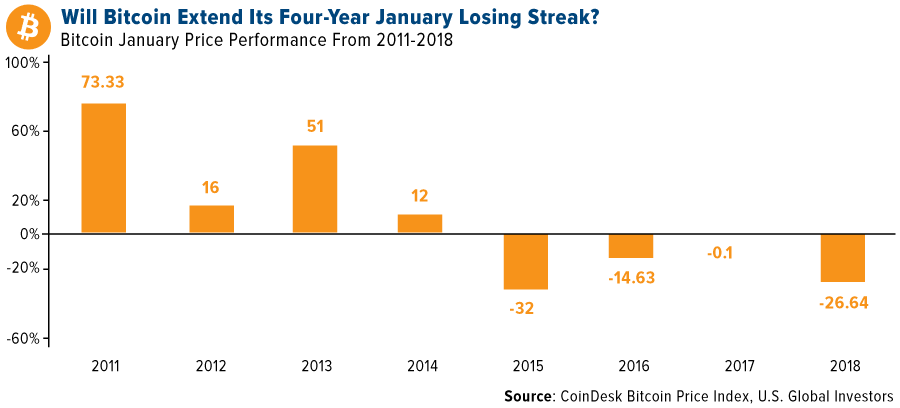

- For the past four years, bitcoin has reported losses for the month of January, and this year might be the fifth straight year. The cryptocurrency fell 13 percent last week and for the month so far it’s down over 2 percent. However, volatility is down significantly from a year ago. The spread between the high and low price stood at $61 as of Wednesday, down 98 percent from the spread of $3,468 from the same January 16 last year, writes CoinDesk.

- CoinTelegraph reports that New Zealand-based digital assets exchange Cryptopia was hacked this week, with the platform reporting via Twitter of “significant losses.” Cryptopia has around 1.4 million registered users and is the largest such exchange in the country. The incident was initially reported as unscheduled maintenance by the company, and then later confirmed as a security breach with key details still lingering about the amount stolen.

Opportunities

- Denmark’s tax agency has gained permission to begin collecting information relating to the trade of digital currencies conducted through three exchanges from 2016 to 2018, Bloomberg writes. Although trading in cryptocurrencies in the country will be exposed to more scrutiny, this could be positive regulation that the industry needs as it develops. The exchanges will need to provide certain user information that “will ensure that citizens who have traded cryptocurrencies have paid the right tax,” the agency said.

- U.S. Representative Tom Emmer is trying to pass a bill, House Resolution 528, which aims “to provide a safe harbor from licensing and registration for certain non-controlling blockchain developers and providers of blockchain services,” writes CoinDesk. The bill hopes to allow companies that use or trade cryptocurrencies, but do not store them, to be exempt from money transmission laws. Emmer introduced an identical bill last year; however, this year the bill has bipartisan support.

- The Financial Times reports that HSBC is using blockchain-based tools to handle processes involved in making foreign exchange trades. The major bank processed more than 3 million forex transactions in the past year. Seeking Alpha writes that this is a positive move and demonstrates that banks are finding useful applications for blockchain technology.

Threats

- Coindesk reports that customers of QuadrigaCX, a cryptocurrency exchange, are complaining that they cannot get their money out even a month after the exchange won a court dispute that tied up $19 million of funds. Additionally, the company announced on Monday that its CEO and founder had died over a month earlier and just reported on it this week. Xitong Zou, a QuadrigaCX customer, told CoinDesk that “there’s a bunch of warning bells going off in most people’s heads right now.”

- A professor at the University of California, Los Angeles (ULCA) predicted this week that 2019 will be even more unkind to cryptocurrencies than 2018 was. In a post listing his predictions for 2019, Scott Galloway wrote that “VR and crypto go from bad to worse.”

- Two researchers from Palo Alto Networks, a cybersecurity firm, published a report this week about a malware called Rocke group that targets public cloud infrastructure. CoinDesk reports that the researchers discovered how Rocke injected code to uninstall five cloud security products from infected Linux servers, including products from Alibaba and Tencent.

Leaders and Laggards

| Index | Close | Weekly Change($) |

Weekly Change(%) |

|---|---|---|---|

| S&P/TSX Global Gold Index | 172.36 | -6.90 | -3.85% |

| Gold Futures | 1,280.30 | -9.20 | -0.71% |

| Natural Gas Futures | 3.43 | +0.33 | +10.71% |

| S&P/TSX VENTURE COMP IDX | 595.51 | -6.26 | -1.04% |

| 10-Yr Treasury Bond | 2.79 | +0.08 | +3.07% |

| Nasdaq | 7,157.23 | +185.75 | +2.66% |

| Oil Futures | 53.79 | +2.20 | +4.26% |

| Hang Seng Composite Index | 3,599.09 | +62.24 | +1.76% |

| S&P 500 | 2,670.71 | +74.45 | +2.87% |

| DJIA | 24,706.35 | +710.40 | +2.96% |

| Korean KOSPI Index | 2,124.28 | +48.71 | +2.35% |

| Russell 2000 | 1,482.50 | +35.12 | +2.43% |

| S&P Energy | 471.53 | +13.25 | +2.89% |

| S&P Basic Materials | 335.00 | +7.56 | +2.31% |

| XAU | 68.38 | -3.33 | -4.64% |

| Index | Close | Monthly Change($) |

Monthly Change(%) |

|---|---|---|---|

| Natural Gas Futures | 3.43 | -0.30 | -7.92% |

| S&P/TSX Global Gold Index | 172.36 | -0.18 | -0.10% |

| 10-Yr Treasury Bond | 2.79 | +0.03 | +1.05% |

| Oil Futures | 53.79 | +6.59 | +13.96% |

| Gold Futures | 1,280.30 | +23.90 | +1.90% |

| S&P 500 | 2,670.71 | +163.75 | +6.53% |

| S&P Energy | 471.53 | +40.03 | +9.28% |

| Hang Seng Composite Index | 3,599.09 | +140.05 | +4.05% |

| DJIA | 24,706.35 | +1,382.69 | +5.93% |

| Korean KOSPI Index | 2,124.28 | +45.44 | +2.19% |

| Nasdaq | 7,157.23 | +520.40 | +7.84% |

| S&P Basic Materials | 335.00 | +23.43 | +7.52% |

| Russell 2000 | 1,482.50 | +133.27 | +9.88% |

| S&P/TSX VENTURE COMP IDX | 595.51 | +53.64 | +9.90% |

| XAU | 68.38 | +1.77 | +2.66% |

| Index | Close | Quarterly Change($) |

Quarterly Change(%) |

|---|---|---|---|

| Natural Gas Futures | 3.43 | +0.23 | +7.29% |

| 10-Yr Treasury Bond | 2.79 | -0.40 | -12.42% |

| DJIA | 24,706.35 | -673.10 | -2.65% |

| Oil Futures | 53.79 | -14.86 | -21.65% |

| S&P 500 | 2,670.71 | -98.07 | -3.54% |

| Gold Futures | 1,280.30 | +44.20 | +3.58% |

| S&P Energy | 471.53 | -62.88 | -11.77% |

| Nasdaq | 7,157.23 | -327.91 | -4.38% |

| Korean KOSPI Index | 2,124.28 | -24.03 | -1.12% |

| S&P Basic Materials | 335.00 | -0.23 | -0.07% |

| Russell 2000 | 1,482.50 | -78.25 | -5.01% |

| Hang Seng Composite Index | 3,599.09 | +197.05 | +5.79% |

| S&P/TSX Global Gold Index | 172.36 | +1.35 | +0.79% |

| S&P/TSX VENTURE COMP IDX | 595.51 | -94.95 | -13.75% |

| XAU | 68.38 | -1.67 | -2.38% |

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission ("SEC"). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (12/31/2018):

Newmont Mining Corp.

North American Palladium Ltd.

Barrick Gold Corp

Hudbay Minerals Inc

Mene Inc

Evolution Mining Ltd

Wesdome Gold Mines Ltd

Northern Star Resources Ltd

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies.

The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks.

The Russell 2000 Index is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months.

The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange.

The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver.

The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar.

The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500.

The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500.

The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period.

The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500.

The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500.

The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500.

The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500.

The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500.

The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500.

The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns.

The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment.

The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The Organization for Economic Co-operation and Development’s (OCED) composite leading indicator (CLI) is designed to provide early signals of turning points in business cycles showing fluctuation of the economic activity around its long term potential level. CLIs show short-term economic movements in qualitative rather than quantitative terms.

The Empire State Manufacturing Index (ESMI) is a survey given out by the Federal Reserve Bank of New York to manufacturing companies within the state of New York. It measures how the people who run these companies feel towards the economy.

The Housing Market Index is based on a monthly survey of National Association of Home Builders (NAHB) members designed to take the pulse of the single-family housing market. The survey asks respondents to rate market conditions for the sale of new homes at the present time and in the next six months as well as the traffic of prospective buyers of new homes.

The S&P 500 Oil & Gas Equipment & Services Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period.

The S&P SmallCap 600 Index is a market capitalization-weighted index consisting of 600 small-capitalization common stocks that is used as a benchmark to measure the performance of small cap stocks.

The S&P/TSX Global Gold Index is designed to provide an investable index of global gold securities. It includes producers of gold and related products, including companies that mine or process gold and the South African finance houses which primarily invest in, but do not operate, gold mines.