Hunting for Yield? Consider Emerging Europe

Date Posted: July 12, 2019

Read time: 7 min

Lately it hasn't been easy out there for yield-seeking investors. Government bonds have continued to rally around the world, pushing yields to record or near-record lows. More than a few have even fallen into negative territory.

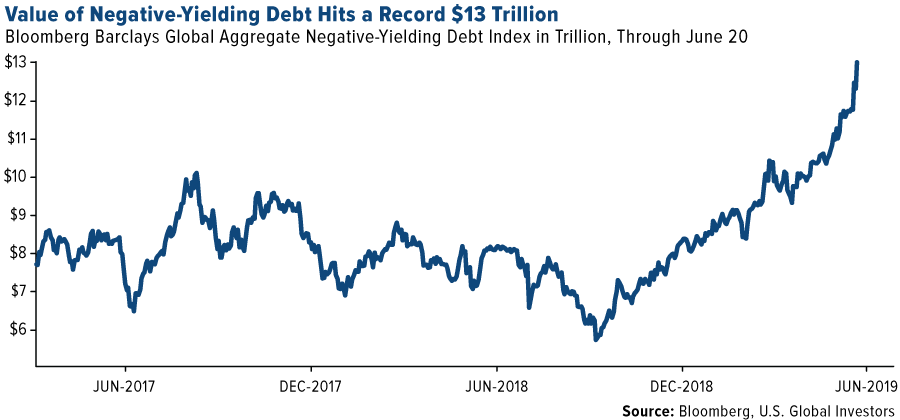

Lately it hasn’t been easy out there for yield-seeking investors. Government bonds have continued to rally around the world, pushing yields to record or near-record lows. More than a few have even fallen into negative territory. In the middle of June, the amount of negative-yielding debt globally reached a record $13 trillion, with more than half of all government debt in Western Europe below zero.

Until now this trend hasn’t been seen in emerging Central and Eastern Europe (CEE) economies, but that’s beginning to change. According to Bloomberg, all of the Czech Republic’s bonds were trading at negative real (inflation-adjusted) yields as of July 8, while the yield on Poland’s 10-year note was just slightly above zero.

So where can investors turn?

Emerging Europe Equities Offer Some of the Best Yields Right Now

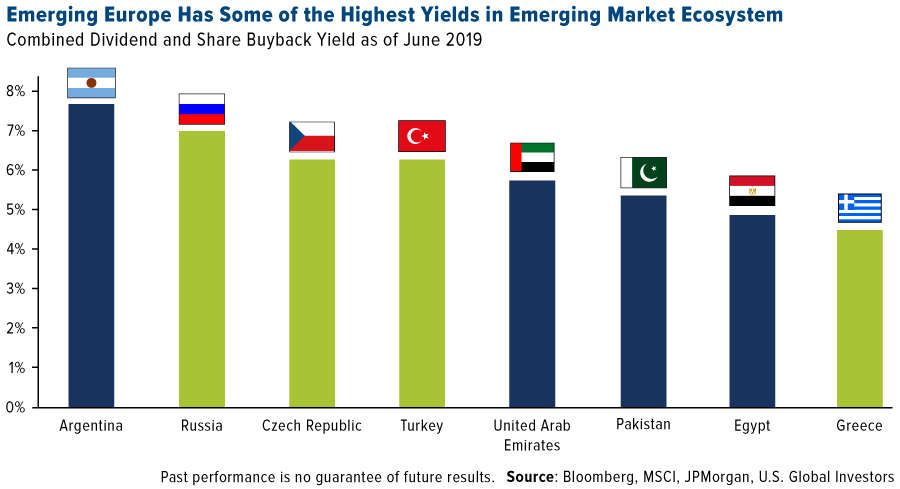

I believe one of the best places in the world to find yield right now is emerging European equities, many of which feature generous dividends and stock buyback programs. Take a look at the chart below. Russia, the Czech Republic, Turkey and Greece all offer some of the highest combined dividend and buyback yields in the entire emerging market (EM) ecosystem. At around 7 percent, Russian stocks had the best yields among emerging European countries as of June, and were second only to Argentinian stocks, according to JPMorgan.

Our Emerging Europe Fund (EUROX) provides access to all four countries’ generous dividends and then some, with Russia the number one country at 52.13 percent of the fund as of the June quarter, Turkey at 11.70 percent, the Czech Republic at 0.88 percent and Greece at 4.37 percent. Hungary, Poland and Romania, which also offer attractive yields, were held in EUROX at the time as well.

You can see the fund’s complete regional breakdown by clicking here.

One of the most generous dividend policies, I believe, is offered by Sberbank, Russia’s largest bank as well as the second largest holding in EUROX as of June 30. The bank is paying out 43.5 percent of its net profit for 2018, which comes out to $5.62 billion, or around $0.25 per share. In a June 12 note to investors, analysts at Renaissance Capital made Sberbank one of their top equity picks for the remainder of 2019. They also recommended natural gas producer Gazprom, gold mining company Polyus and Globaltrans Investment, all of which could also be found in EUROX as of June 30.

Russia Has Led Global Equity Rally So Far in 2019

There are other reasons why I find emerging Europe so compelling, and Russia in particular. Russian stocks have had a good run so far in 2019, surging 30 percent year-to-date through July 5 on a number of factors. For comparison’s sake, the S&P 500 Index rose 19 percent over the same period.

Chief among the contributing factors has been the huge price rally in crude oil, responsible for approximately 60 percent of Russia’s exports and some 30 percent of its gross domestic product (GDP). Renaissance Capital reports that the country’s budget is “comfortably in surplus… with budget parameters calculated using $40 a barrel real oil prices.” Crude is currently trading above $65 per barrel.

In addition, geopolitical conditions have improved. Russian stocks sold off last year, prompted by additional U.S.-imposed sanctions. However, in January, the Treasury Department lifted a number of these sanctions, and the State Department declined to impose any new ones involving the March 2018 poisoning of a former Russian intelligence agent. Investors seem confident that the U.S. won’t take any further actions—in the near term, at least—that might hurt the Russian economy.

For these reasons and more, Russia’s credit rating has recently been raised to investment grade by the three major rating agencies—Standard & Poor’s, Moody’s and Fitch.

Finally, Russian stocks are trading at very attractive multiples right now. According to Renaissance Capital, Russia is trading on a 12-month forward price-to-earnings of 5.9x, the second lowest among EMs.

Discover the Emerging Europe Fund (EUROX) by clicking the link below today!

Please consider carefully a fund’s investment objectives, risks, charges and expenses. For this and other important information, obtain a fund prospectus by visiting www.usfunds.com or by calling 1-800-US-FUNDS (1-800-873-8637). Read it carefully before investing. Foreside Fund Services, LLC, Distributor. U.S. Global Investors is the investment adviser.

Foreign and emerging market investing involves special risks such as currency fluctuation and less public disclosure, as well as economic and political risk. By investing in a specific geographic region, a regional fund’s returns and share price may be more volatile than those of a less concentrated portfolio. The Emerging Europe Fund invests more than 25% of its investments in companies principally engaged in the oil & gas or banking industries. The risk of concentrating investments in this group of industries will make the fund more susceptible to risk in these industries than funds which do not concentrate their investments in an industry and may make the fund’s performance more volatile.

There is no guarantee that the issuers of any securities will declare dividends in the future or that, if declared, will remain at current levels or increase over time. A fund’s yield may differ from the average yield of dividend-paying stocks held by the fund.

The Bloomberg Barclays Global Aggregate Negative Yielding Debt Market Value Index measures the stock of debt with yields below zero issued by governments, companies and mortgage providers around the world which are members of the Bloomberg Barclays Global Aggregate Bond Index.

The MSCI Russia Index is designed to measure the performance of the large and mid-cap segments of the Russian market. With 23 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in Russia. The MSCI Emerging Markets Europe Index captures large and mid-cap representation across 6 Emerging Markets (EM) countries in Europe. With 72 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in each country. The S&P 500 Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies.

A bond’s credit quality is determined by private independent rating agencies such as Standard & Poor’s, Moody’s and Fitch. Credit quality designations range from high (AAA to AA) to medium (A to BBB) to low (BB, B, CCC, CC to C).

The forward price-to-earnings ratio (forward P/E) is a valuation method used to compare a company’s current share price to its expected per-share earnings.

Fund portfolios are actively managed, and holdings may change daily. Holdings are reported as of the most recent quarter-end. Holdings in the Emerging Europe Fund as a percentage of net assets as of 6/30/2019: Sberbank of Russia PJSC 8.34%, Gazprom PJSC 7.64%, Polyus PJSC 0.63%, Globaltrans Investment PLC 0.60%.

All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.